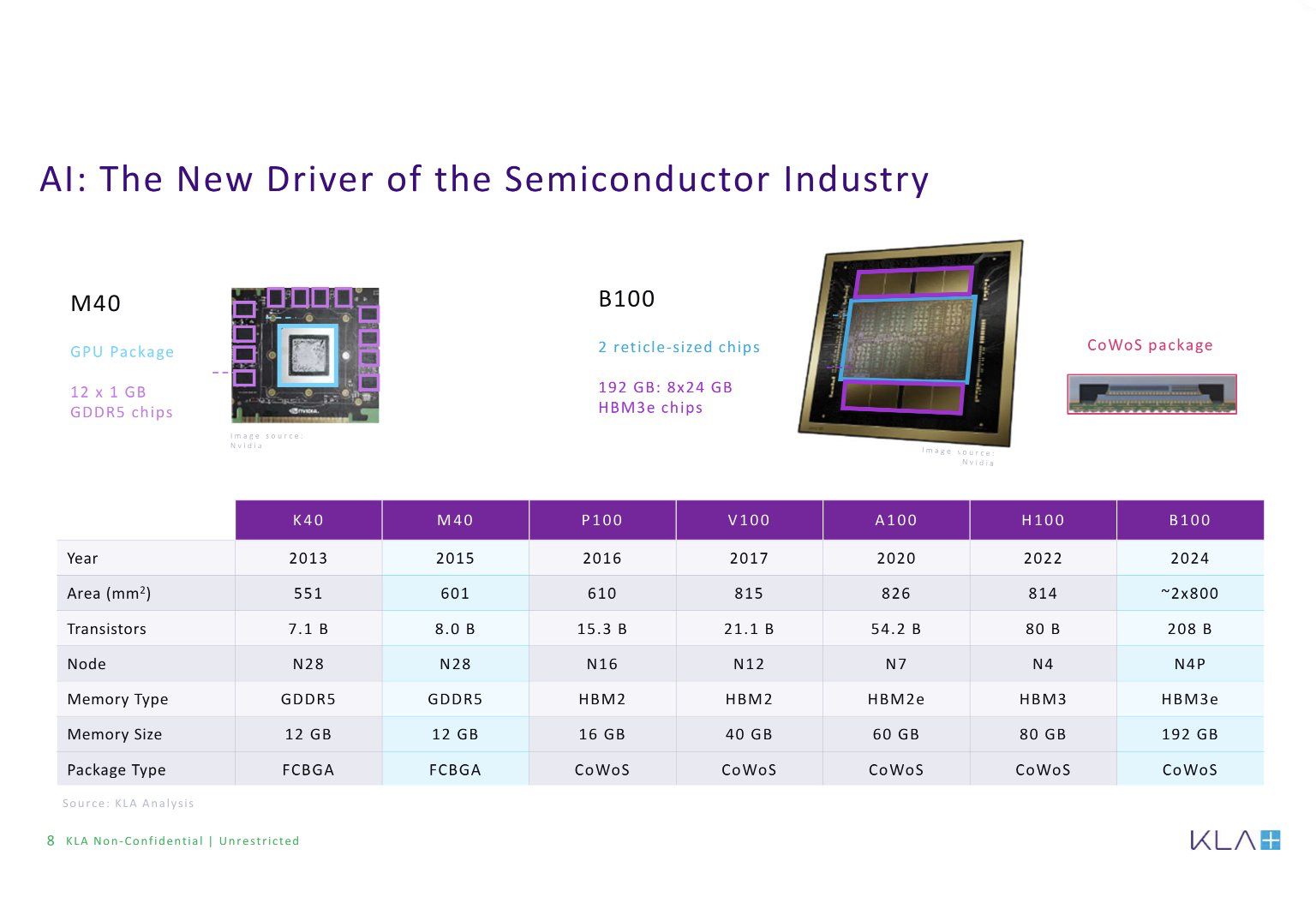

“So I tried just to put together this chart to show how different the GPU package is between 2015 & 2024. So of course, the B100 chip, the GPU introduced a few months ago, and this is not enough because Jensen has already introduced the next generation of GPU last week” (h/t The Transcript).

“Two things on remote jobs is really fascinating right now. So pre-pandemic, there’s — at any given time, there’s 15 million, 20 million jobs that are posted on LinkedIn actively. And pre-pandemic, it was roughly 2% of all jobs on the platform were remote jobs. If you go back 2.5 years ago, it peaked. 20%, 21% of all jobs on LinkedIn were remote jobs, which is pretty insane to see that jump from 2% to 21%. And now that number is back to 8%, so it kind of peaked up and now it’s starting to come back down again. So we pay a lot of attention to kind of how the labor market is shifting through remote work, and it seems like that trend is coming down” Linkedin CEO.

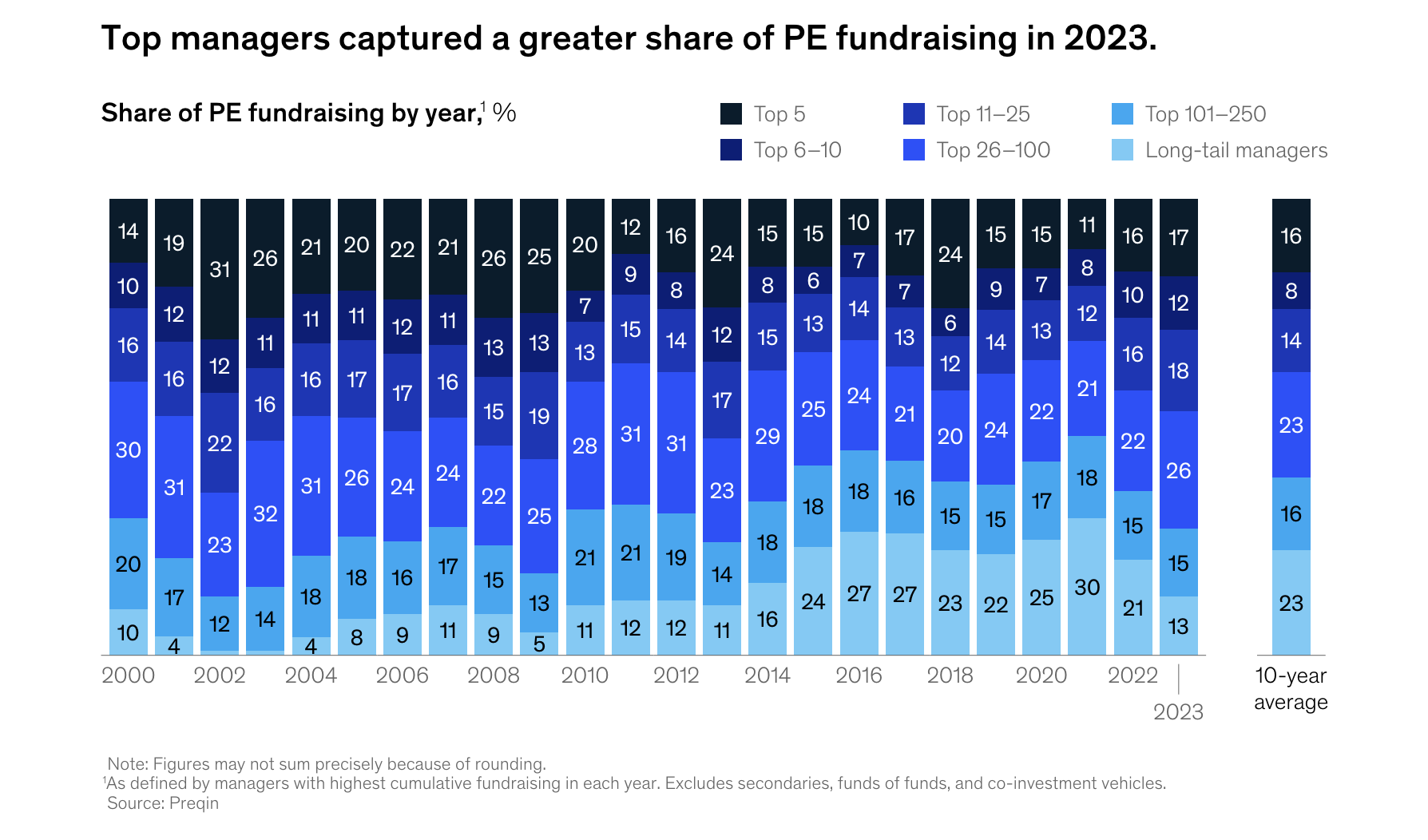

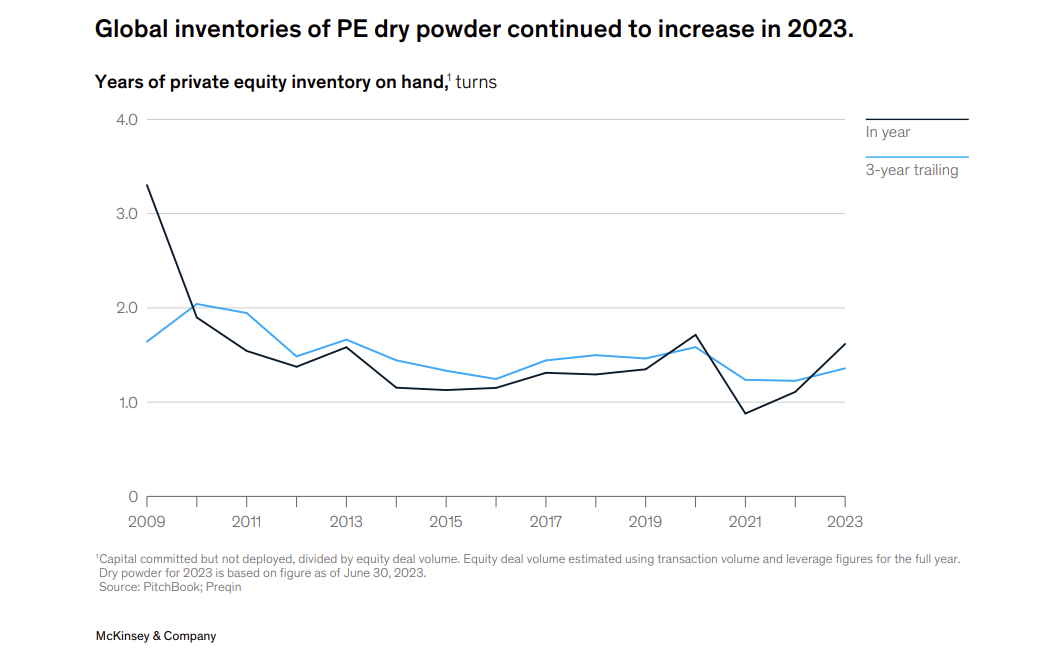

Many people talk about the absolute value of PE dry powder. Indeed this hit a record last year of $2.2 trillion – fundraising continued (at a slower pace) against a dramatic slowdown in dealmaking.

However “Dry-powder inventory (the amount of capital available to GPs expressed as a multiple of annual deployment) increased from 1.1 years in 2022 to 1.6 years in 2023 but remains within the metric’s normal historical range“.

“Decisions made in the next decade are more highly levered to shape the future of humanity than at any point in human history.“

“Technological transitions are packaged deals, e.g. free markets and the industrial revolution went hand-in-hand with the rise of “big government” (see Tyler Cowen on The Paradox of Libertarianism).“

“Natural constraints are often better than man-made ones because there’s no one to hold responsible.“

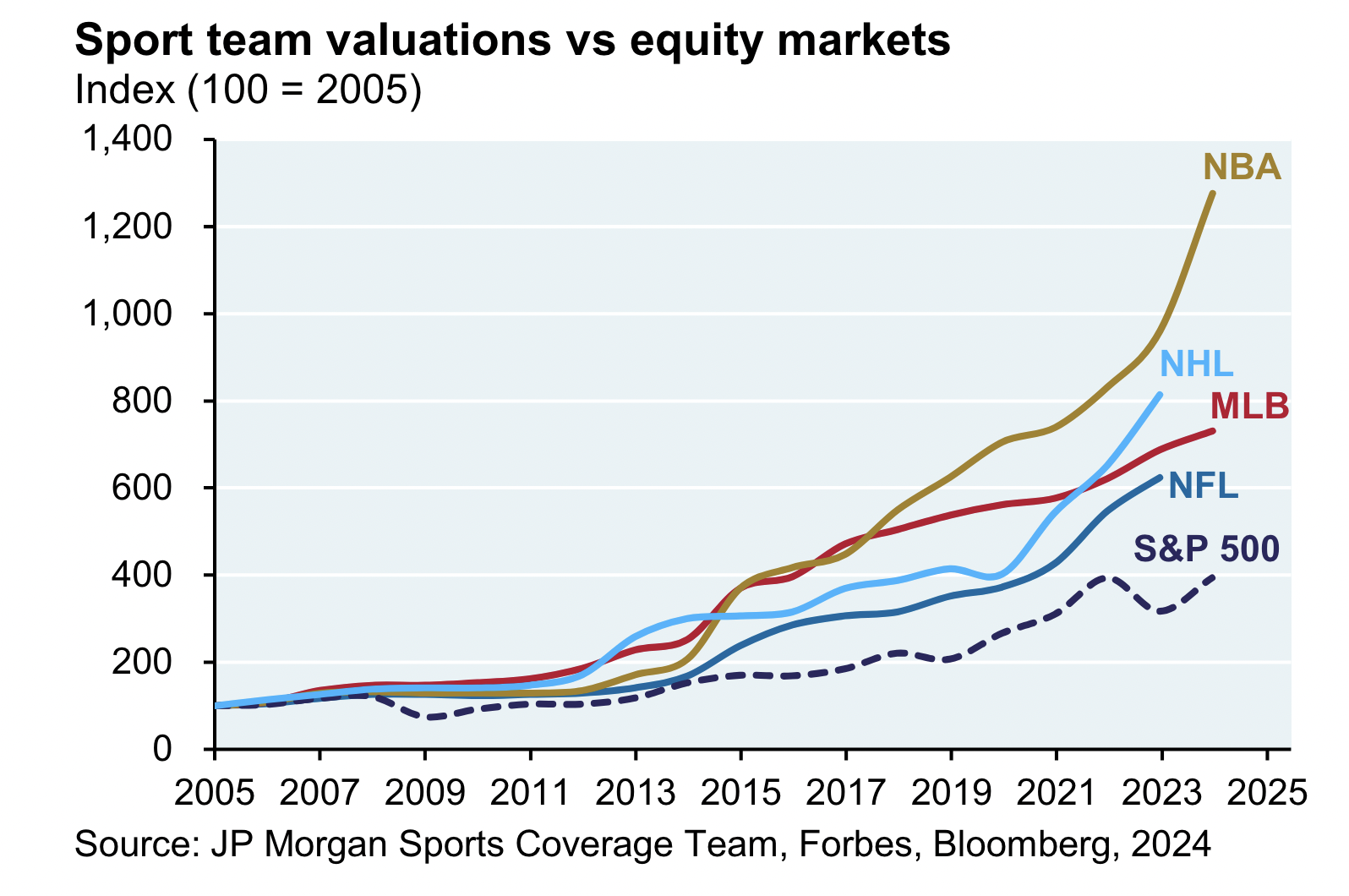

A nice report on investing in sports teams, leagues, and related businesses from JPMAM.

Why now? Historically ownership of sports teams in the US was for the ultra-wealthy, but this is about to change.

“Forbes also constructs a valuation index for each league. As shown below on the left, these indexes have substantially eclipsed the S&P 500 since 2005. To be clear, sports teams are much more expensive than equities: most teams are now valued at 5x-12x sales compared to ~3x sales for the S&P 500.”

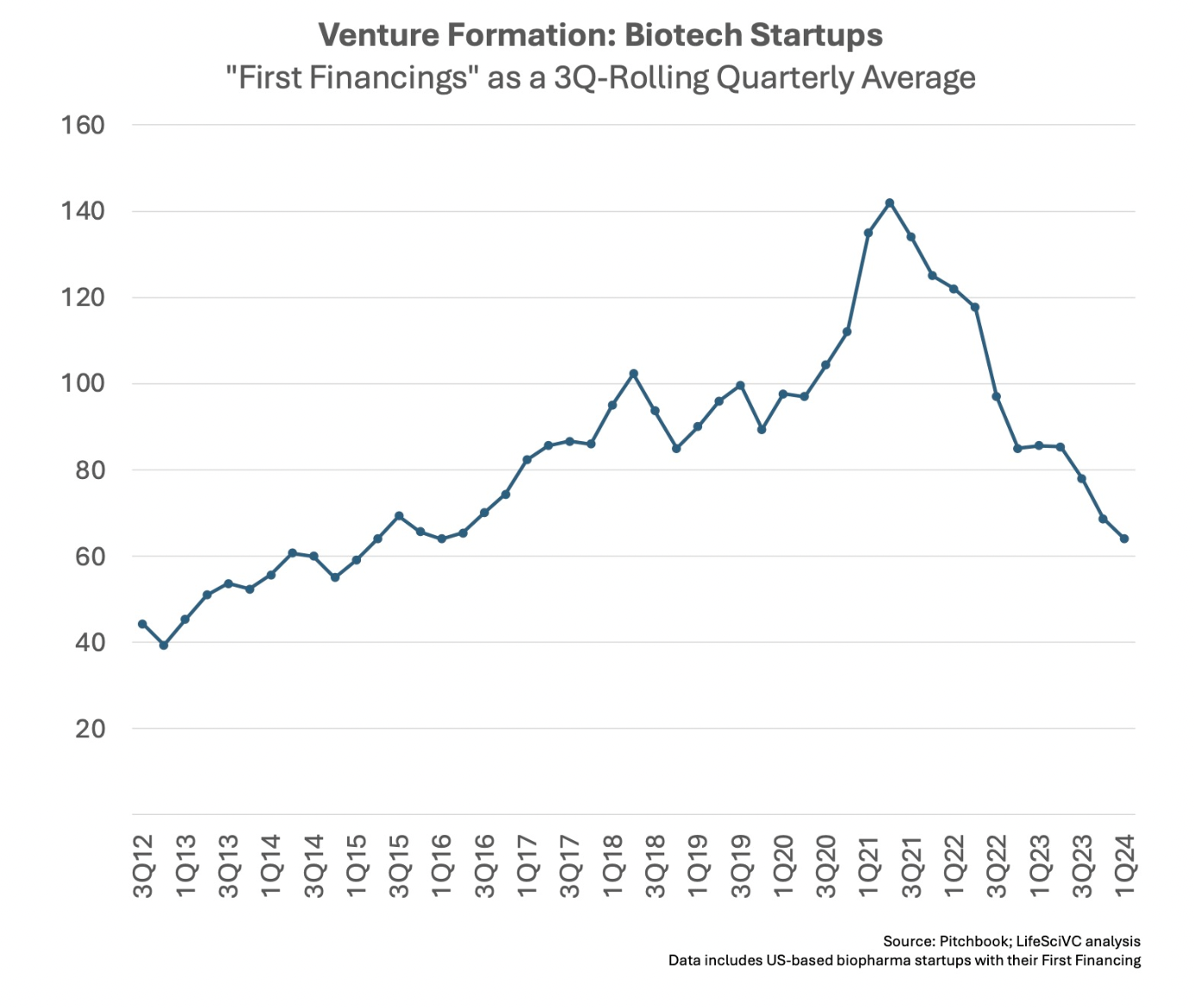

“According to the latest Pitchbook data, venture creation in biotech hit its slowest quarterly pace in eight years during 1Q 2024. With just over 60 new biotechs raising their first round of financing, the sector’s company formation activity has slowed 50-60% from its historic peak in 2021.“

The piece argues why this is a positive for the health of the sector.

“I know that the legal profession does a great job of identifying competence and rewarding it financially. Cheap lawyers are expensive.“

“I know that environmental influence is the most effective form of behavioral control. Accordingly, if you want radical change, radically change your environment. Being in the wrong city will cancel out years of self-improvement.“

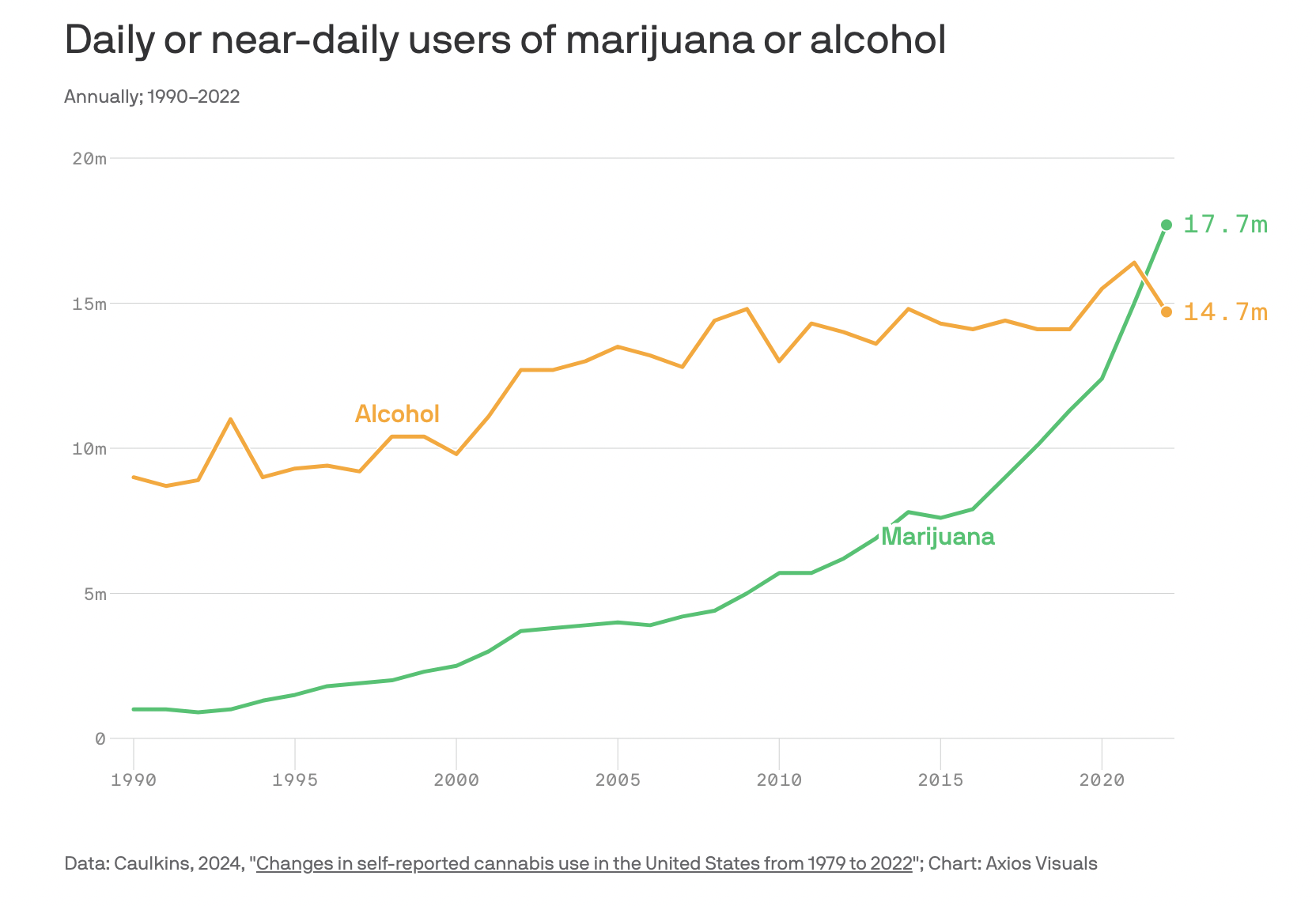

“Daily or near daily marijuana use grew by 269% from 2008 to 2022, according to an analysis conducted by Jonathan Caulkins, a Carnegie Mellon University professor.“

“Meanwhile, the prevalence of daily or near daily alcohol use fell by 7%.“

There is probably enough evidence now to suggest GLP-1s, like Ozempic, work to treat all kinds of addiction.

Why does this matter? “Addiction kills more Americans than cancer or heart disease but only 4% of people with substance use disorders currently receive medication.“