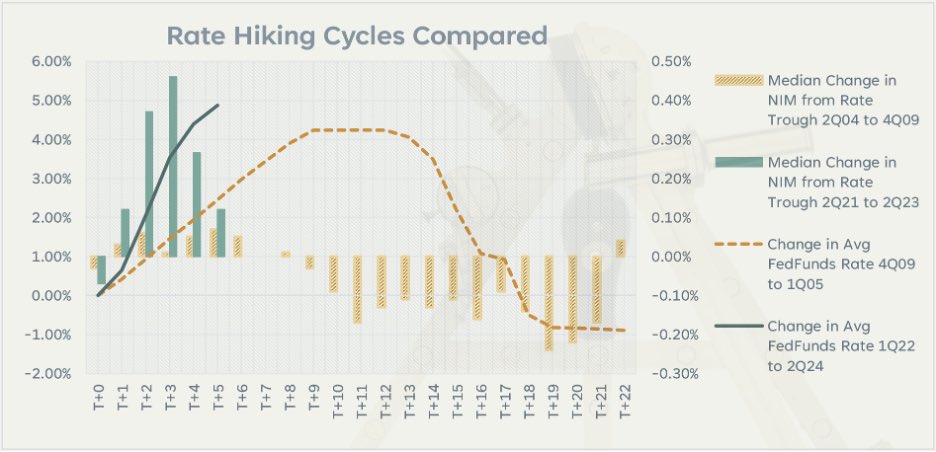

Excellent analysis of how banks got themselves in a bad position this rate-rising cycle.

So much to learn – capitulation led banks into buying MBS that suffer from negative convexity “trapping” (by rising rates extending weighted average lives) banks into low-yielding assets, not enough capital to take losses, held-to-maturity accounting choice requiring marking everything to market (“tainting the book”), the head fake from a higher portion of floating assets pulling forward net interest margin gains.

The result – a worrying state of affairs with funding rates having a long way to go hurting earnings for a long time. This isn’t good for the credit outlook either.

In case you missed it – Loeb’s latest missive from Q1.

His purchase of UBS is interesting – though CS will undoubtedly have more skeletons (see here) and lose more AuM (as clients diversify), the uplift to UBS book value (74% accretive, putting UBS post deal on 0.74x P/TBV), state loss guarantees (CHF 9bn post first 5bn), and liquidity provision (CHF 100bn) are all positives.

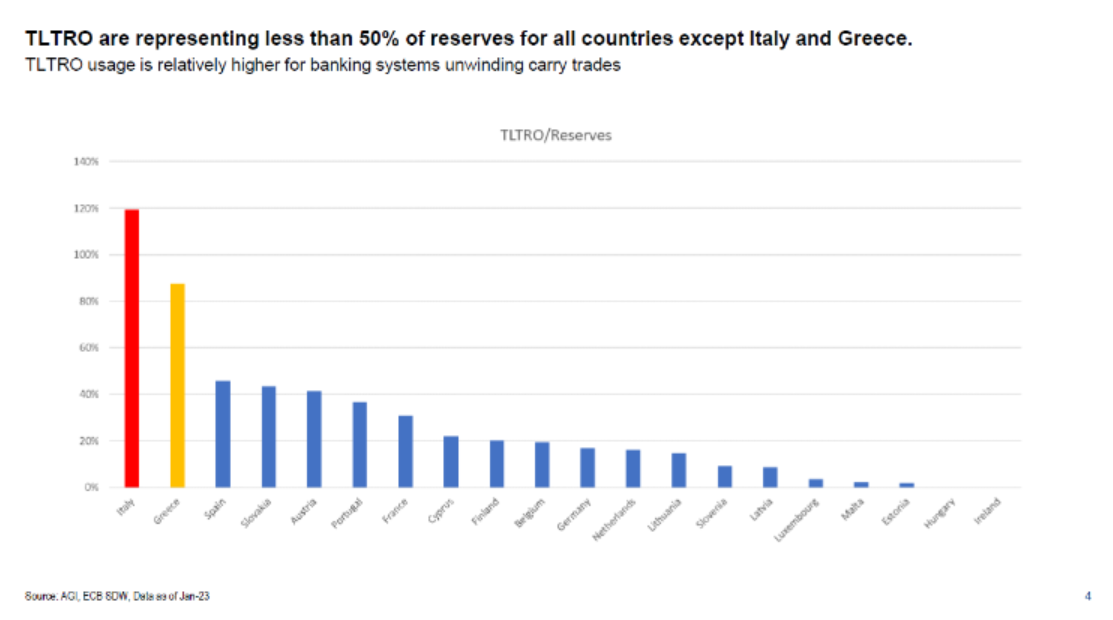

Italy and Greece stand out as still holding huge TLTRO balances relative to reserves.

This could be a painful unwind as these obligations are very cheap and backed by illiquid (as defined by current standards) assets, hurting liquidity coverage ratios.

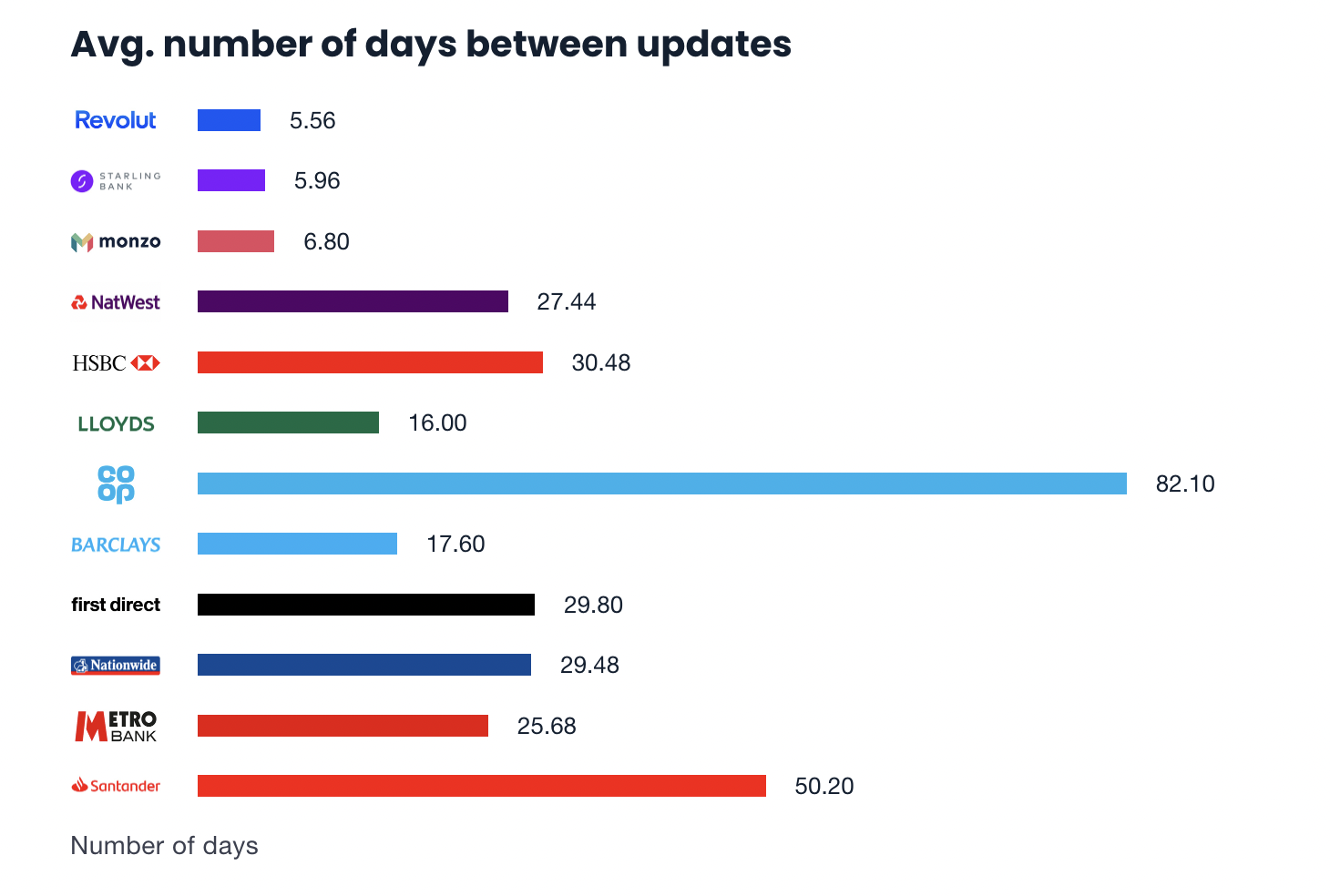

900 days ago this site ran a series of article comparing challenger banks and incumbents in the UK on how good their user experience was (we covered it here).

Today, there is an update, and the picture hasn’t changed.

This chart for example shows the time between app updates – a measure of how quickly improvements are coming to customers.

“On average, the challenger banks deploy updates 4.6x more frequently than the incumbents“.

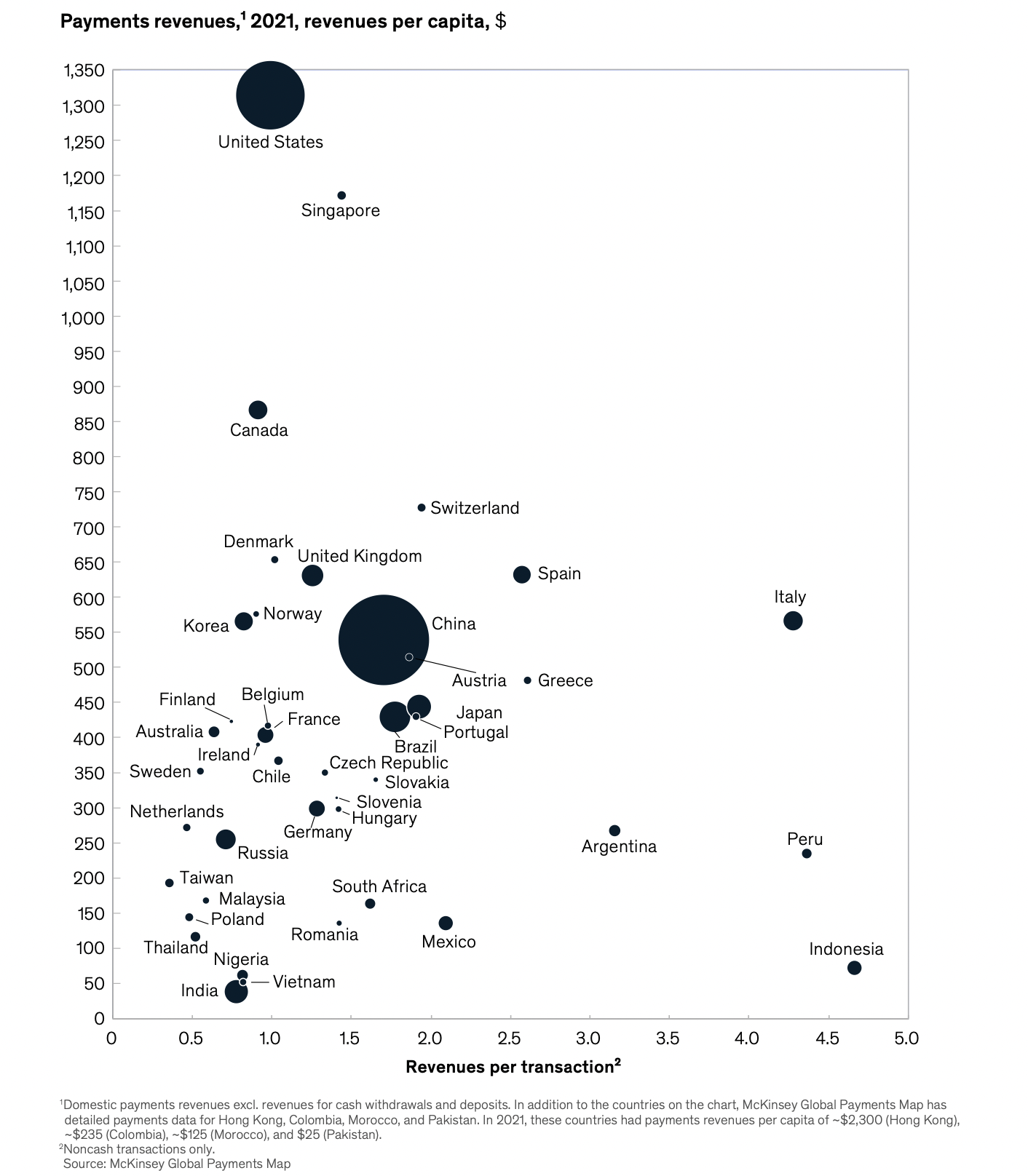

“There remains significant country-level dispersion in revenue per transaction, driven by a variety of factors, including transaction pricing dynamics and payment instrument mix“

FedNow, a faster payments network designed by the Federal Reserve, is nearing launch in 2023 and this is a great explainer/history post.

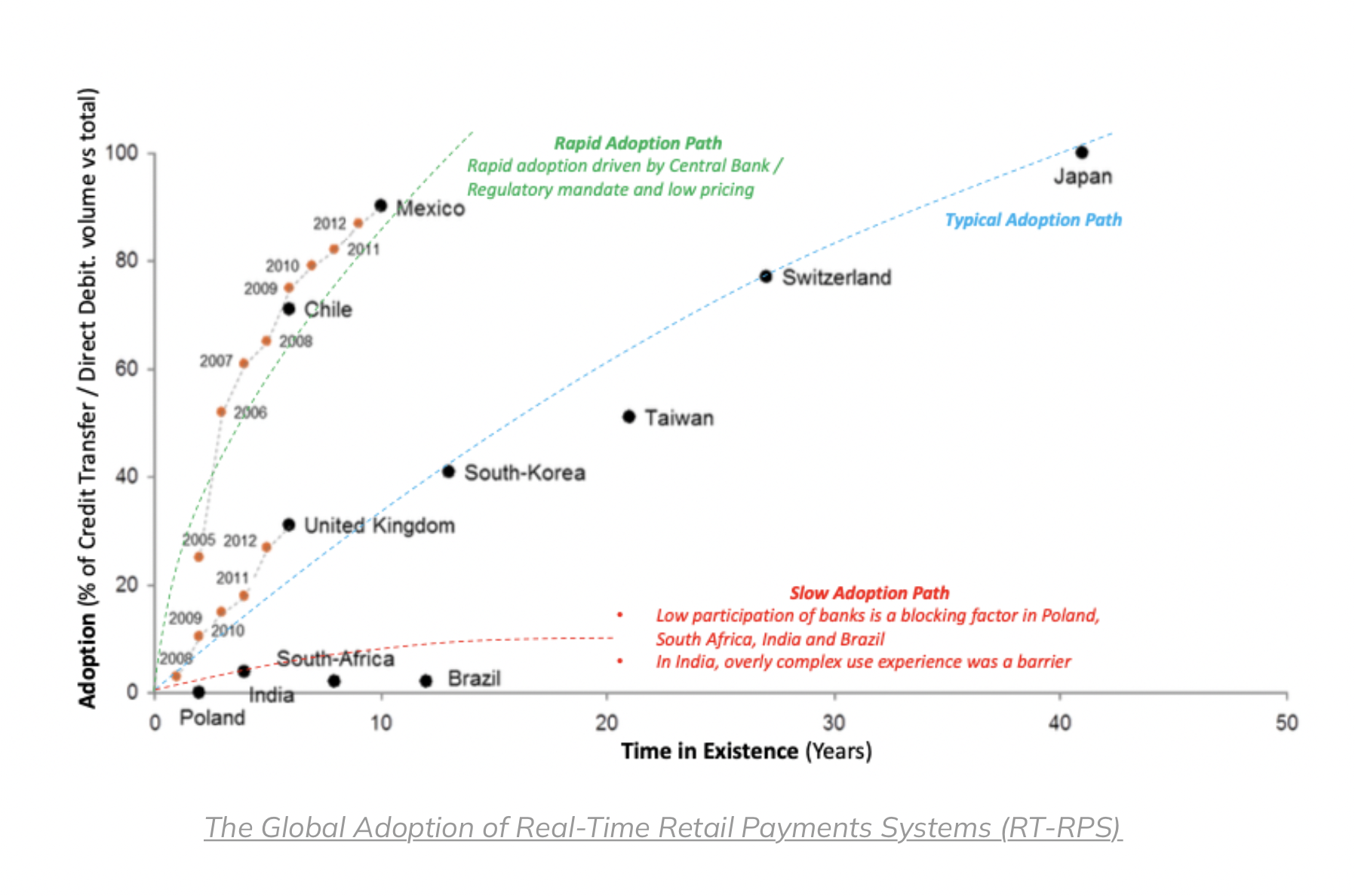

The US lags far behind the rest of the world in faster payments.

FedNow could change that (or not) – it for one is cheaper than existing competitors.

There is also this chart, showing adoption rates of faster payment systems around the world – those that launched recently had faster adoption (especially if helped along by regulators).

Interesting first hand account of how Monzo grew from nothing to 1 million users in three short years.

Tom credits – a great product (compared to competition) that was a delight to use, a brightly coloured card, and network effects – “if you had 3+ friends on Monzo when you joined, you had a 70% chance of being a WAU [weekly active user] by day 90, versus only a 50% chance if you didn’t have any friends on the platform.“

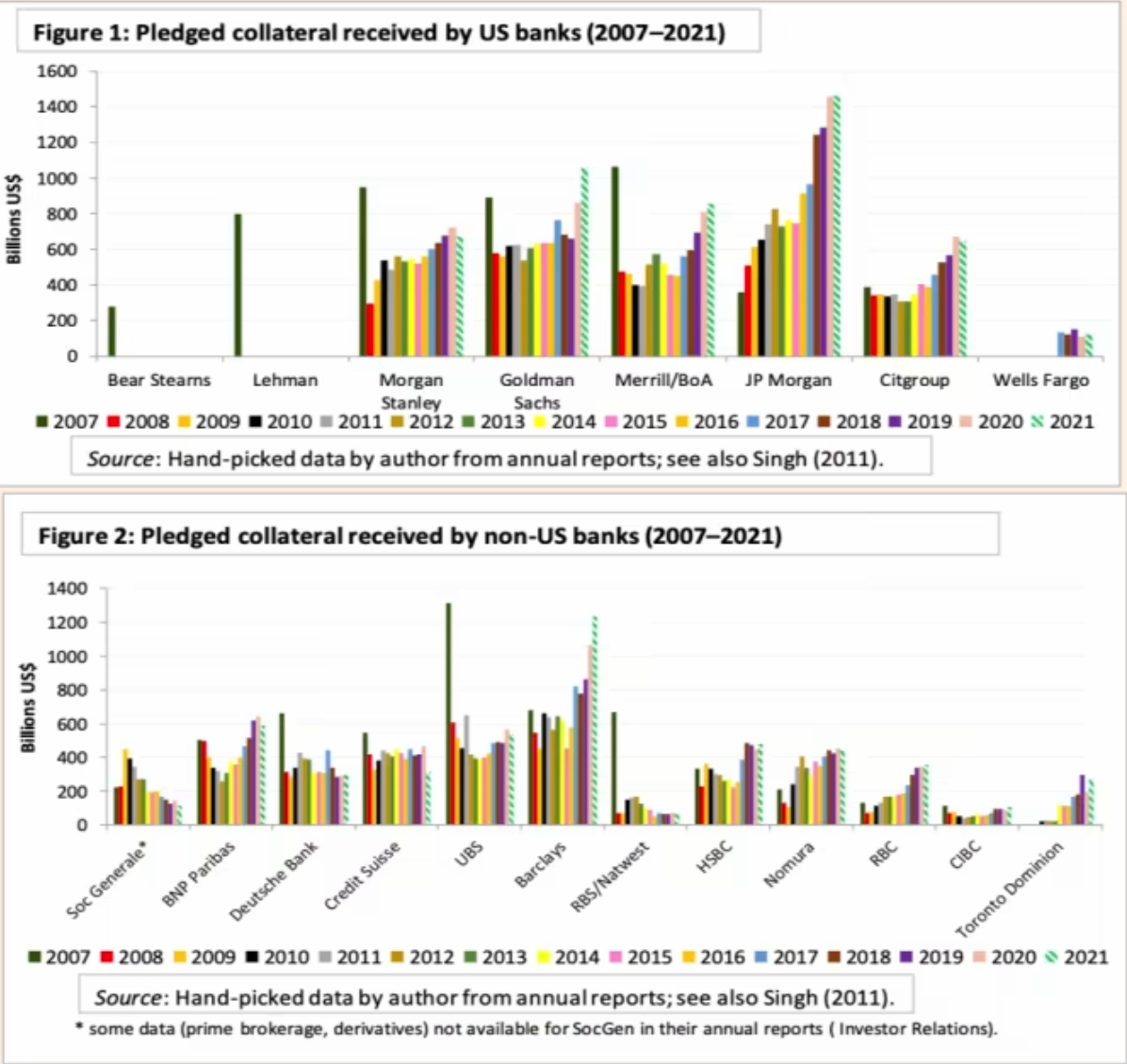

The Global Financial crisis 14 years ago ushered in a new era of attempting to understand the pipes of the global financial system – especially incorporating the shadow banking world.

One big node point is pledged collateral and so called collateral velocity. The world expert on this is IMF senior economist Manmohan Singh.

This latest post on FT AV by Singh is absolutely worth a read to understand what is going on now.

These charts are one part of the picture – showing how pledge collateral has grown but also moved around.

“As you might expect, a lot has changed since 2007, with the disappearance of Lehman Brothers and Bear Stearns, the reshuffling of business models by UBS, Credit Suisse and Deutsche Bank, and the rise of JPMorgan and Barclays.“

Credit Suisse, who suffered $5.5bn in losses in the Archegos debacle earlier in 2021, have published a full report of what happened by an external firm.

Nice read for those interested in the inner workings of the Prime Brokerage business.

If you aren’t familiar with it, this is a brilliant introduction and history (paywalled).

COBOL is the programming language that underpins the entire financial system.

“Over 80% of in-person transactions at U.S. financial institutions use COBOL. Fully 95% of the time you swipe your bank card, there’s COBOL running somewhere in the background.“

“The second most valuable asset in the United States — after oil — is the 240 billion lines of COBOL”

The language is old (from the 1960s) and runs on huge machines (mainframes), yet it is extremely suited to the task of processing billions of transactions very fast.