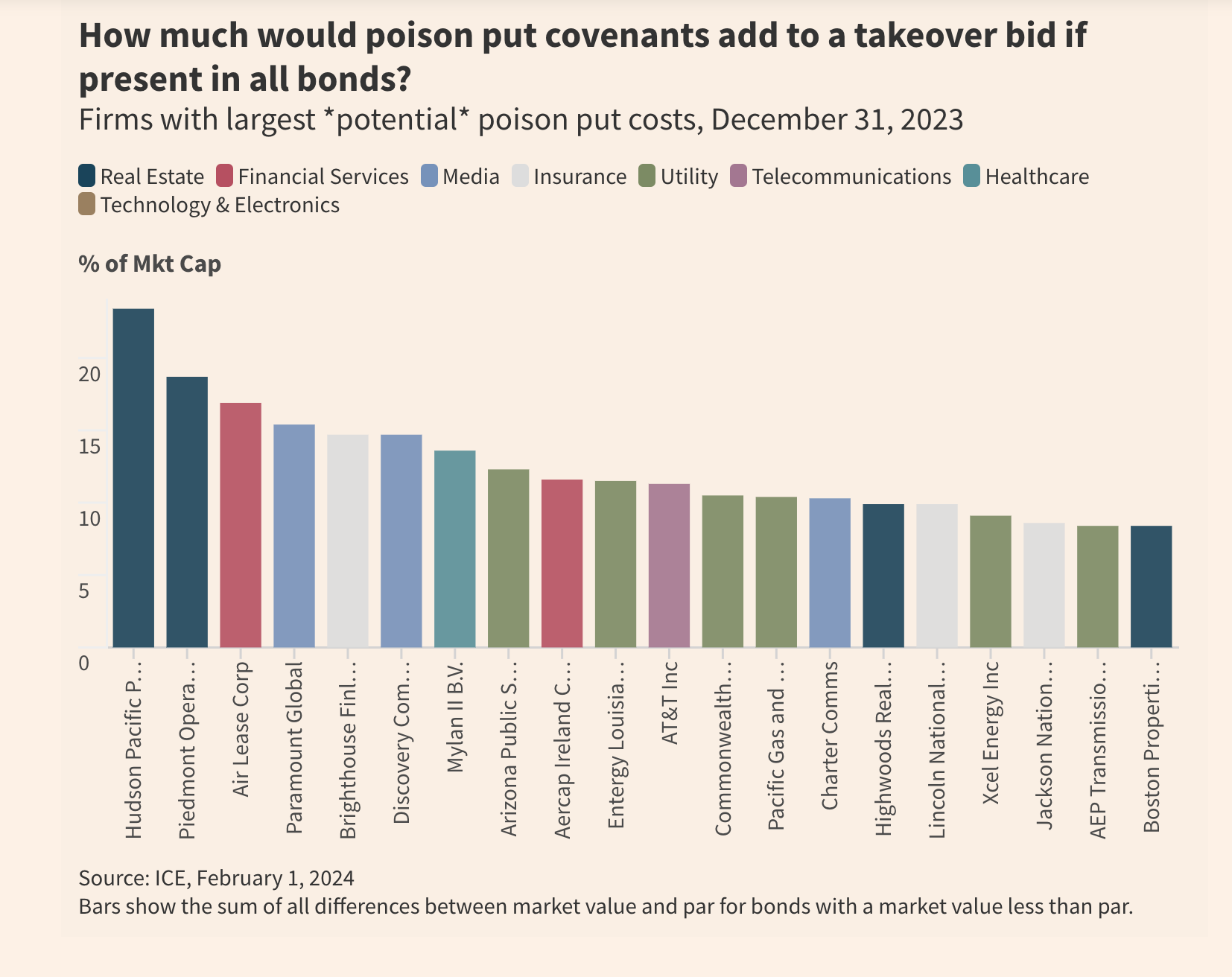

“Senior secured bonds have always been a constituent of the high yield market. However, over the past few years, their share of the overall index has increased dramatically and is now at a record level of the market. While the coupon structure is different, senior secured bonds are “secured” by the assets of the borrower, much like leveraged loans. This recent development — the growth of senior secured bonds as an overall percentage of the high yield market — blurs the lines between these markets and may lead to increasingly similar behavior between the markets.”

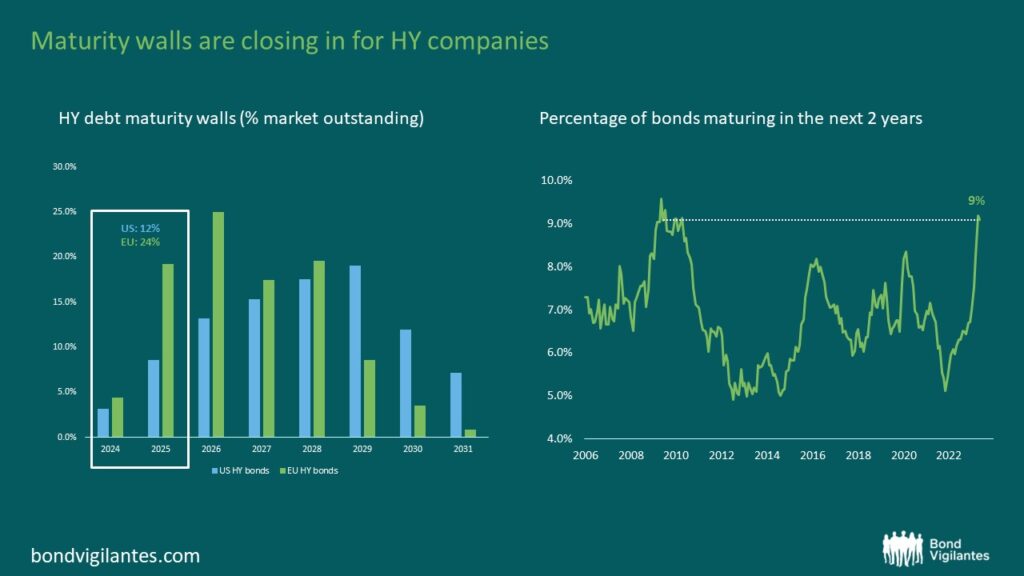

“The chart below shows the substantial amount of debt to roll over in the next 2 years with $127bn, or circa 12% of the market’s outstanding debt, being due for US HY companies. In Europe, maturity walls are even steeper, with €97bn of debt (23% of the index) maturing in 2024/2025. Add in 2026 maturities, and the refinancing wall shoots up to just to under 50% of the market. Historically speaking, this is likely to become the largest refinancing effort for HY issuers since the GFC (2008), and while some companies have already begun doing their homework, we expect it to become a key theme in 2024, particularly if base rates and borrowing costs remain elevated.”

Unlike GFC, as M&G points out, the situation is better – (1) new issuance is open (2) rates are lower despite the spike (3) quality is better.

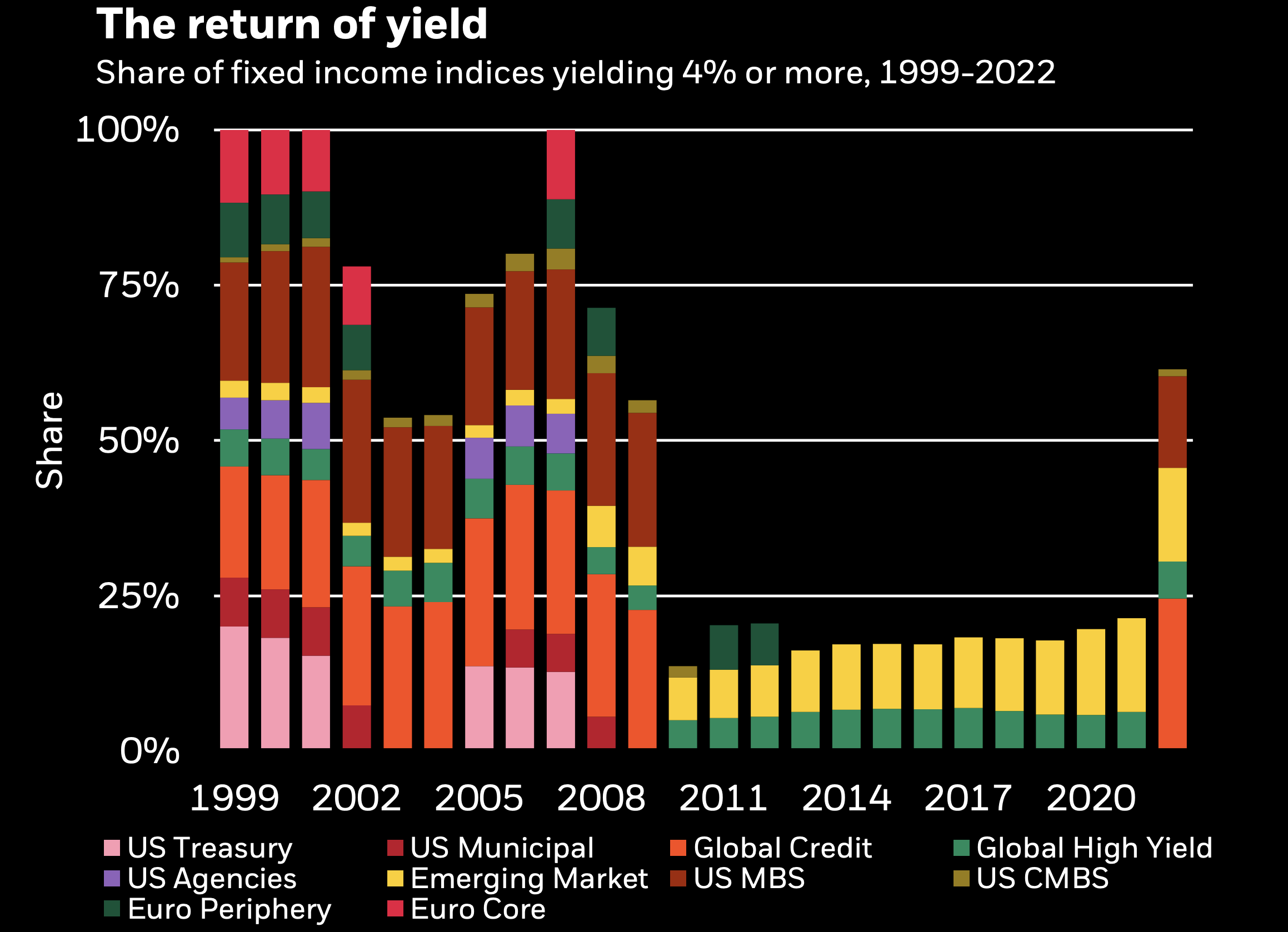

For the first time in a decade, the majority of fixed income assets yield 4% or above.

NB “The bars show market capitalization weights of assets with an average annual yield over 4% in a select universe that represents about 70% of the Bloomberg Mulitiverse Bond Index.”

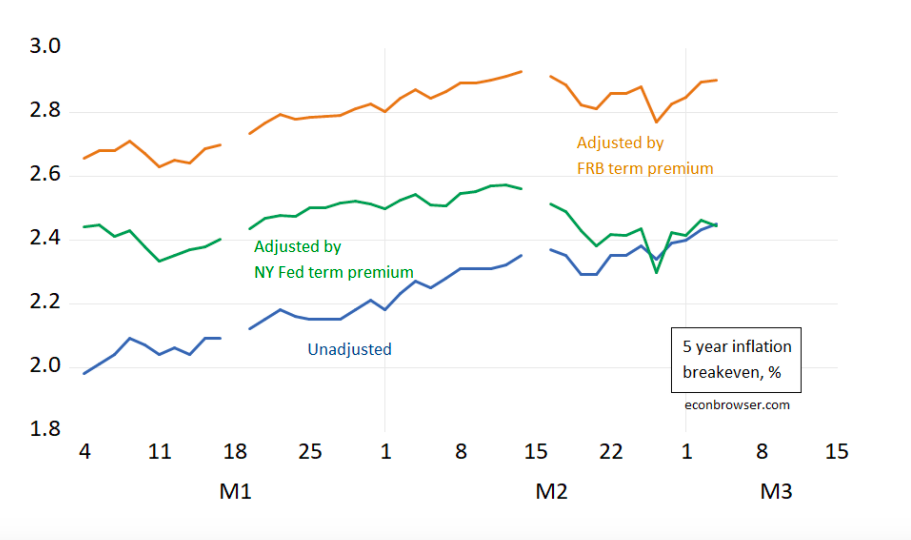

“The five year constant maturity Treasury yield has risen; but after accounting for the estimated term premium, the increase is much more modest, if not negative. Moreover, expected 5 year inflation has not on net moved much over 2021.“

Correction: One needs to also adjust for the liquidity premium.

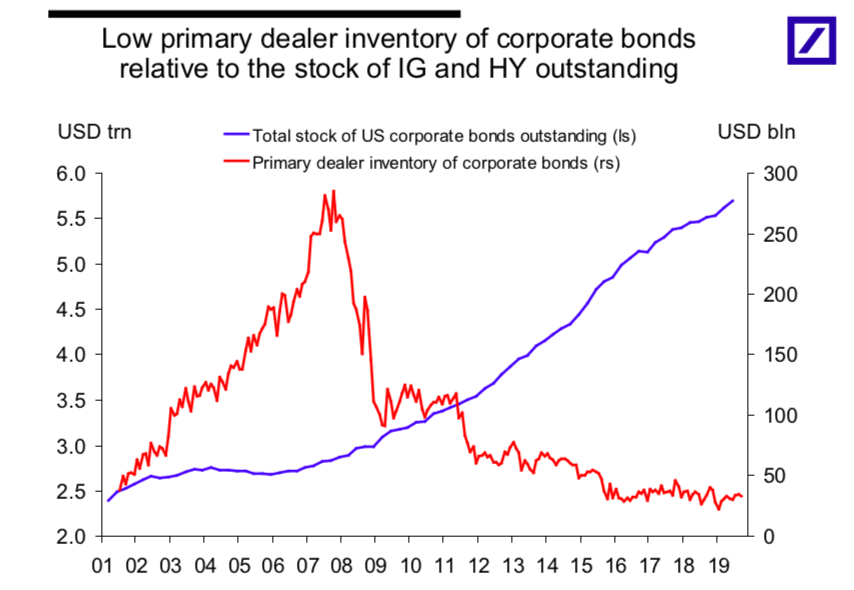

“With fewer opportunities to profit from connecting buyers and sellers, and a much greater risk of losing money in the meantime, HFT-style market makers pulled back abruptly and in some cases likely shut down entirely. Thus the liquidity they provided dropped to a tiny fraction of its previous peak over the first couple weeks of March“

Blaming ratings agencies doesn’t exactly fill anyone with confidence.

Softbank put out this statement asking for Moody’s to withdraw rating due to “excessively pessimistic assumptions regarding the market environment and misunderstanding and speculation that SBG will quickly liquidate assets without any thorough consideration and without making improvements to its financial condition“

We have previously written about the risks building form the rising popularity of bond ETFs.

This article argues the opposite – more ETFs = more trading in bonds = liquidity.

We take issue with these arguments. An inspection of two bond etf prices shows you that they have mostly marched upwards (e.g. LQD, VCIT).

As ETFs go up they create more units and are willing buyers in bond markets. This of course creates liquidity.

The main issue will be on the downside – if something goes wrong, ETFs, en masse as they follow pre-set rules, will sell and there won’t be anyone on the other side.