New home sales is a great variable to watch for recessions.

“When the YoY change in New Home Sales falls about 20%, usually a recession will follow.”

Any Fed tightening cycles that cause recessions show up here first.

There are exceptions to this rule – usually due to strong spending on defence or non-residential investment holding the economy up. The pandemic also distorted the series.

Useful resource assessing the state of the logistics industry.

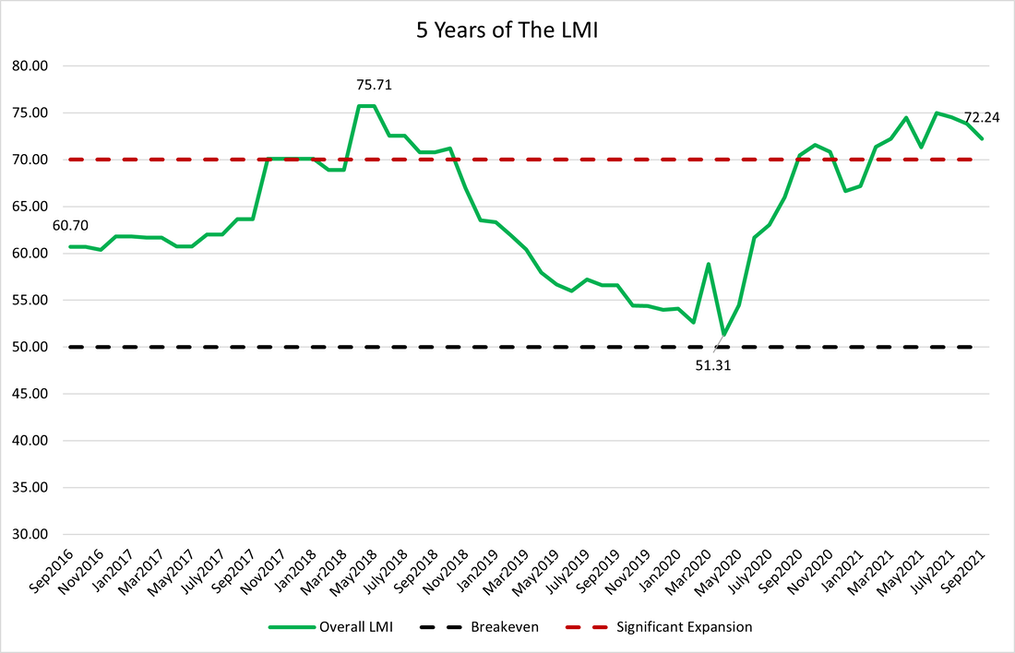

The index has been going for 5 years, consists of eight components and is calculated using a diffusion index i.e. readings above 50 indicate expansion.

The current stretch above 70 – meaning significant growth – is the longest on record.

Will be interesting to watch if the situation improves and along which components.

“It is not just Asia which is seeing renewed weakness of manufacturing performance, however, with output in Russia coming close to stagnation again in June as rising virus numbers disrupted the economy, and a further steep fall in output was recorded in Mexico.

As a result, while developed world production continued to grow at a rate close to decade-highs in June, emerging market output growth came close to stalling, its lowest since June 2020.“

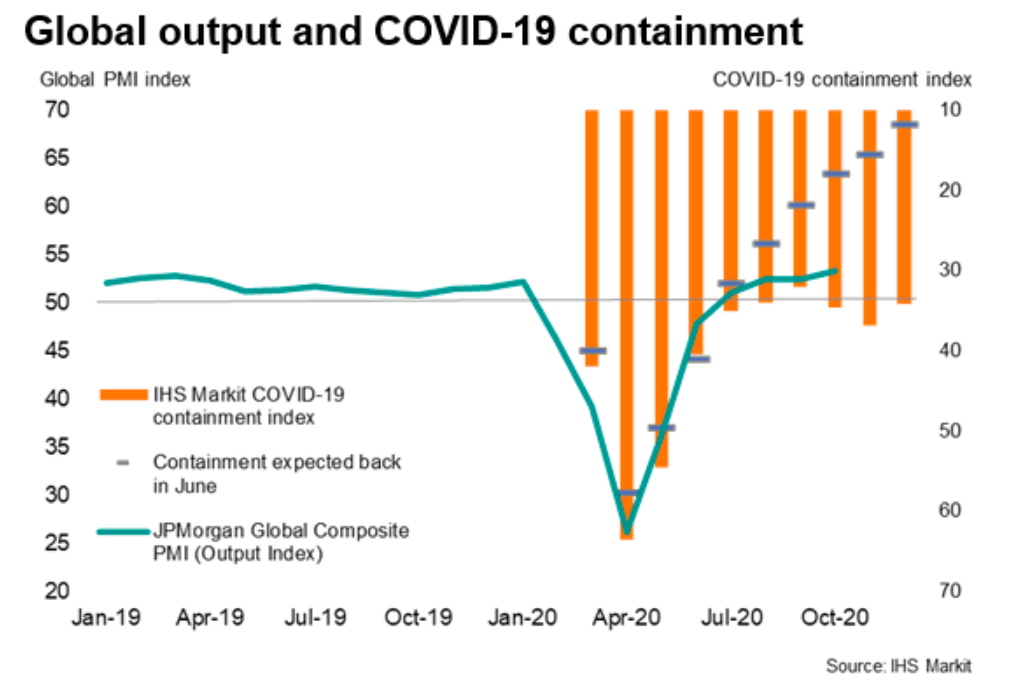

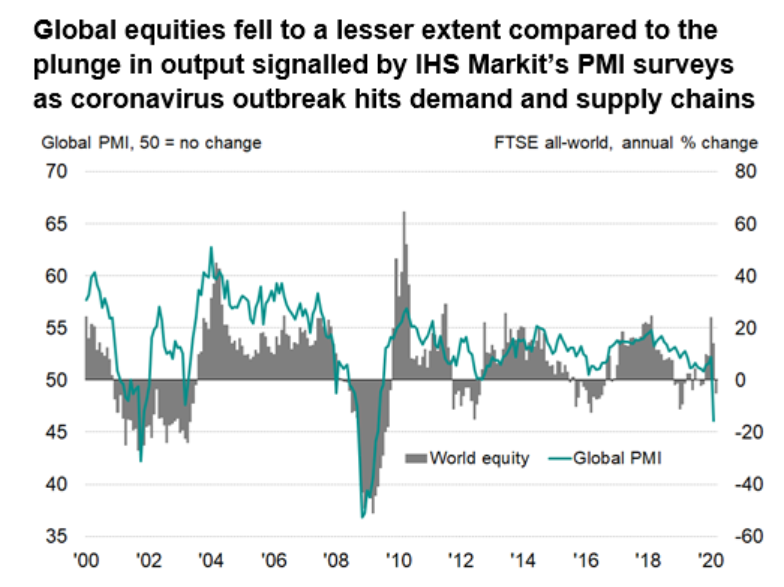

Interesting chart plotting global PMI (green line) against an index of containment (orange line, degree to which economies are locked up).

This index eased from a peak of 64 in April to 32 in September, helping PMIs rise.

In October it has started to rise to 35, and throughout has remained higher than what was expected a few months ago (dashes) – it should have been 18 by now.

The UK is looking very weak on the eve of Brexit, inventory re-stocking boost has run out

IHS Markit/CIPS UK Manufacturing PMI Release hit 47.4 in August – the lowest level since 2012 (https://tinyurl.com/y5qrhe75)

“The high levels of economic and political uncertainty pervasive across domestic and global markets continued to weigh heavily on the performance of UK manufacturing during August. Output volumes fell as intakes of new work contracted at the fastest pace for over seven years, while business optimism dropped to a series-record low.“