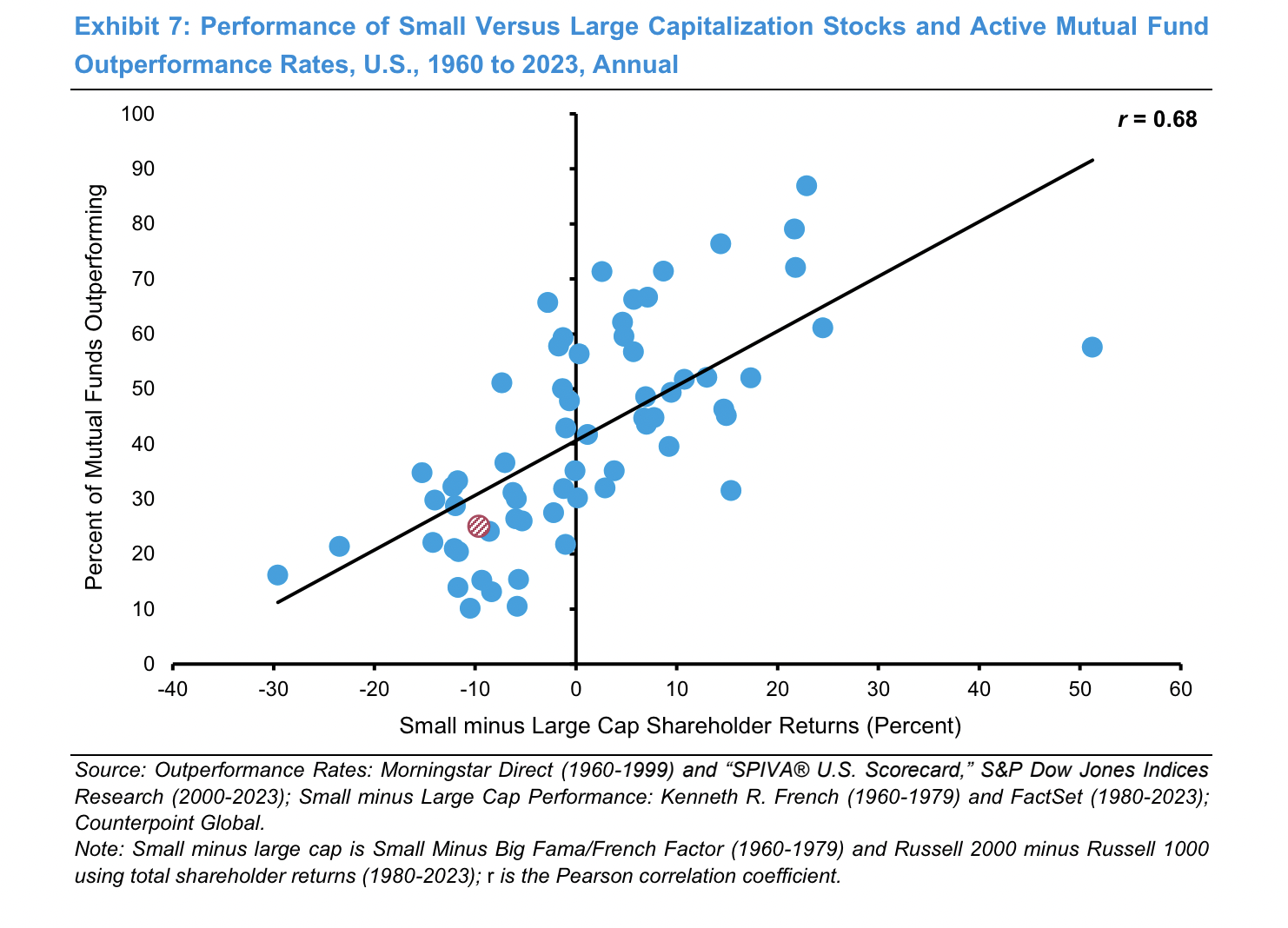

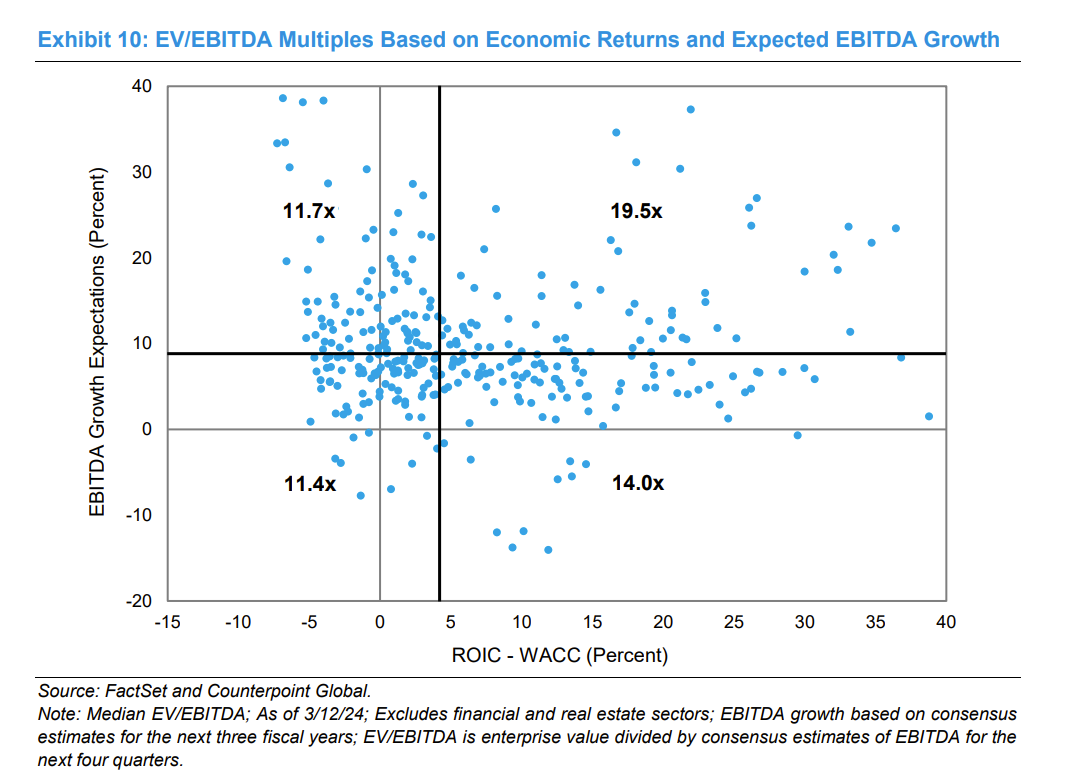

“Rising stock market concentration is challenging for active managers because on average they own stocks with smaller market capitalizations than those in their benchmarks. That means when large-cap stocks do well relative to small-cap stocks, the percentage of mutual funds that outperform the benchmark tends to go down. When small caps outperform large caps, active managers outperform at a higher rate. Exhibit 7 shows this relationship from 1960 to 2023. The striped red dot shows the outcome for 2023.“

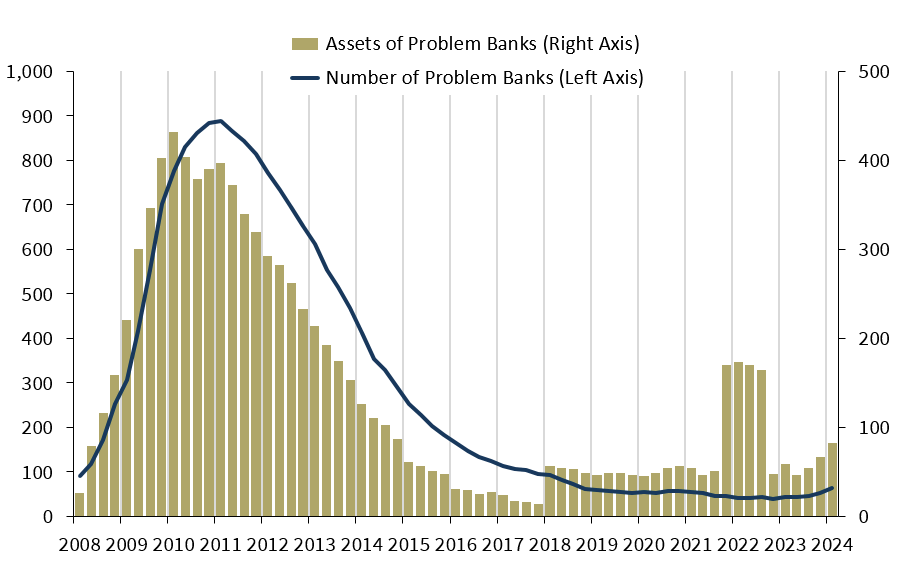

“The number of banks on the FDIC’s “Problem Bank List” increased from 52 to 63. Total assets held by problem banks rose $15.8 billion to $82.1 billion. Problem banks represent 1.4 percent of total banks, which is within the normal range for non-crisis periods of 1 to 2 percent of all banks.“

CRE looks to be causing some problems – “The noncurrent rate for non-owner occupied CRE loans of 1.59 percent is now at its highest level since fourth quarter 2013, driven by office portfolios at the largest banks.“

Some stats tracking the state of the CTA industry, which appears to be in poor health.

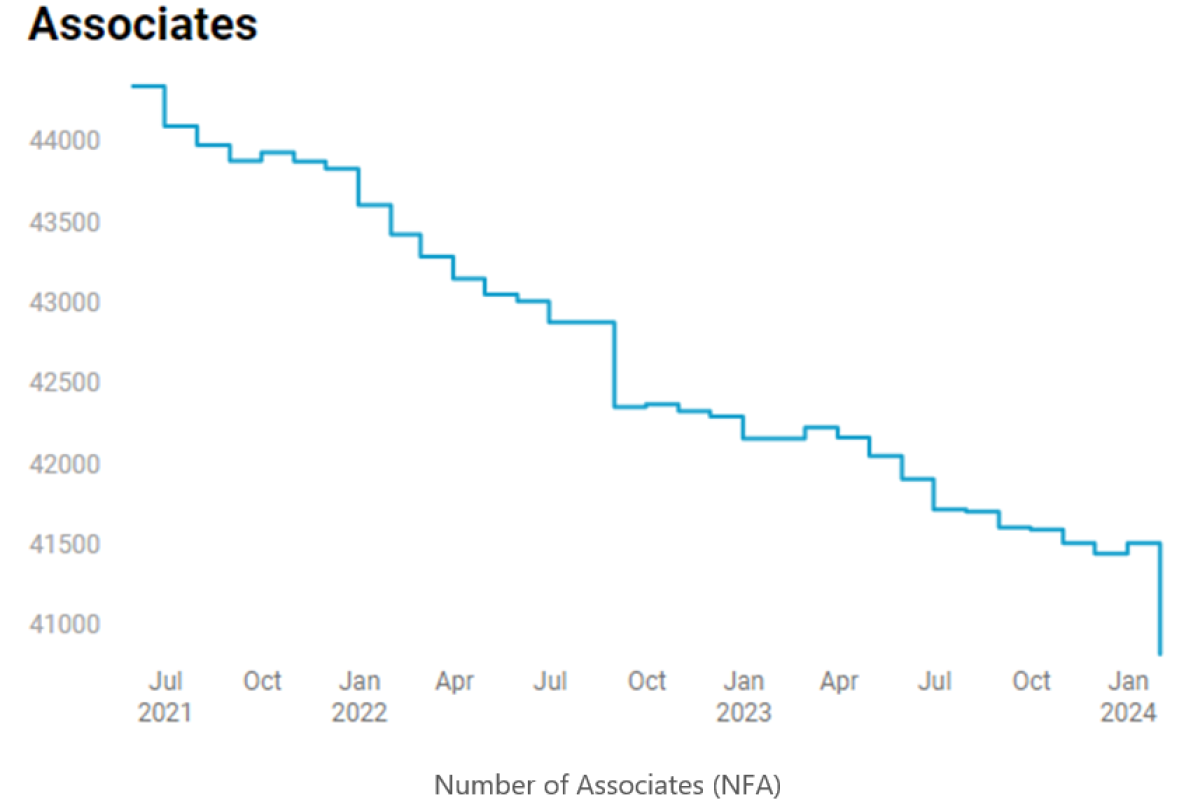

“In January we saw the largest decline in the number of Associates, i.e. individuals working in the Futures Industry. We recorded a decline of 687 individuals no longer seeking to do business.“

“A weak-link problem is where success depends upon the quality of the worst component, whereas a strong-link problem is where it depends upon the quality of the best.“

Understanding which is which is a useful thinking tool.

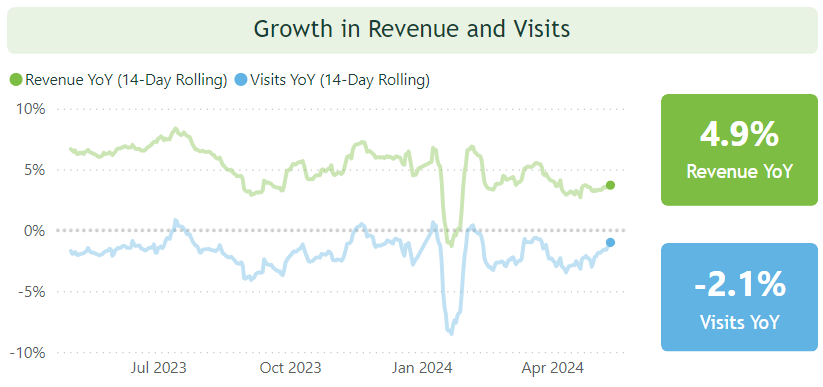

Those interested in the sector this is a good Atlantic piece on the rising cost of vet care in the US (spoiler alert: private equity and corporate ownership).

AVMA actually has a handy tracker of vet visits and revenues.

Admitting that “I don’t know” at least once a day will make you a better person.

Changing your mind about important things is not a consequence of stupidity, but a sign of intelligence.

Where you live—what city, what country—has more impact on your well being than any other factor. Where you live is one of the few things in your life you can choose and change.