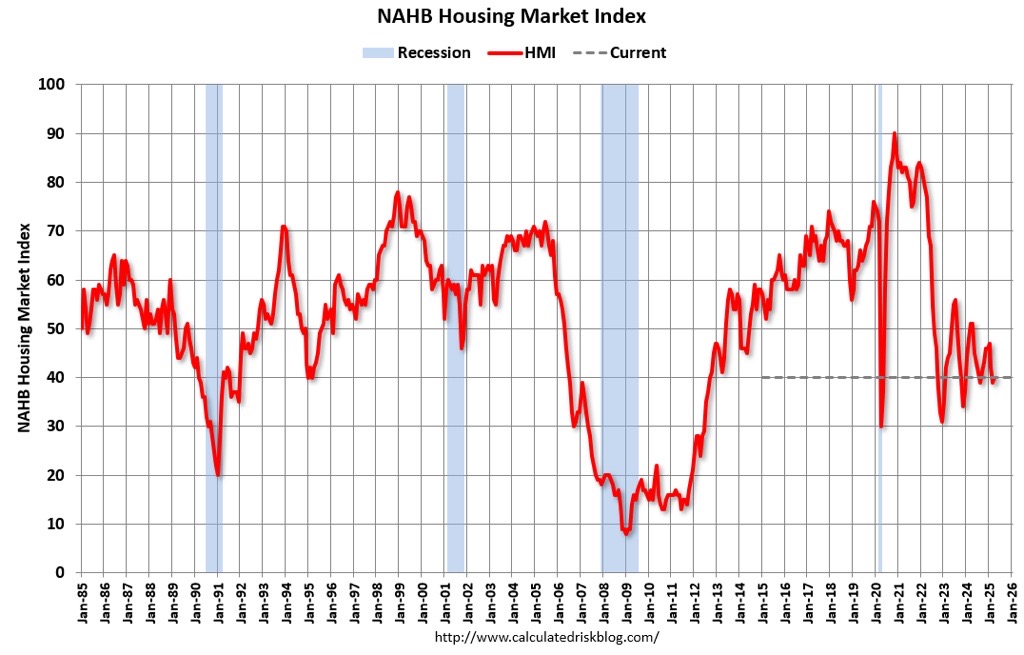

“Policy uncertainty is having a negative impact on home builders, making it difficult for them to accurately price homes and make critical business decisions,” said NAHB Chief Economist Robert Dietz. “The April HMI data indicates that the tariff cost effect is already taking hold, with the majority of builders reporting cost increases on building materials due to tariffs.”

When asked about the impact of tariffs on their business, 60% of builders reported their suppliers have already increased or announced increases of material prices due to tariffs. On average, suppliers have increased their prices by 6.3% in response to announced, enacted, or expected tariffs. This means builders estimate a typical cost effect from recent tariff actions at $10,900 per home.

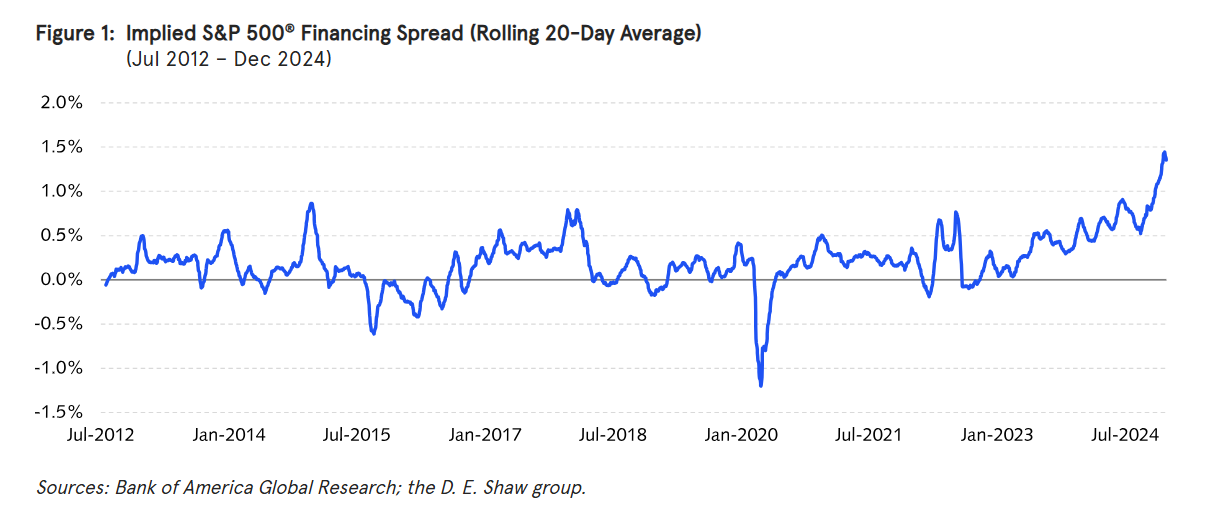

The financing rate for equity exposure via futures has been very high.

The S&P 500® financing spread can’t be directly observed, but it can be estimated by comparing the actual price of futures to the fair value implied by dividend forecasts, interest rates, and spot prices. Figure 1 plots one such estimate since 2012.