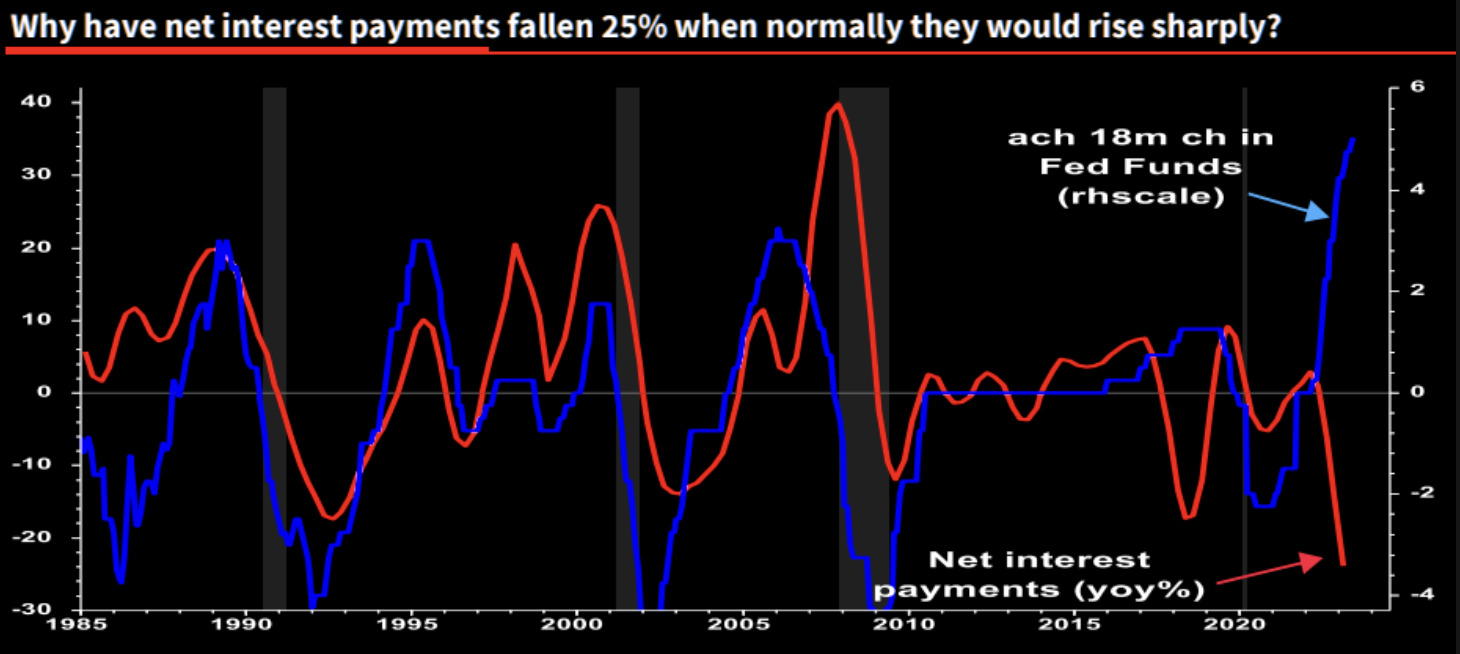

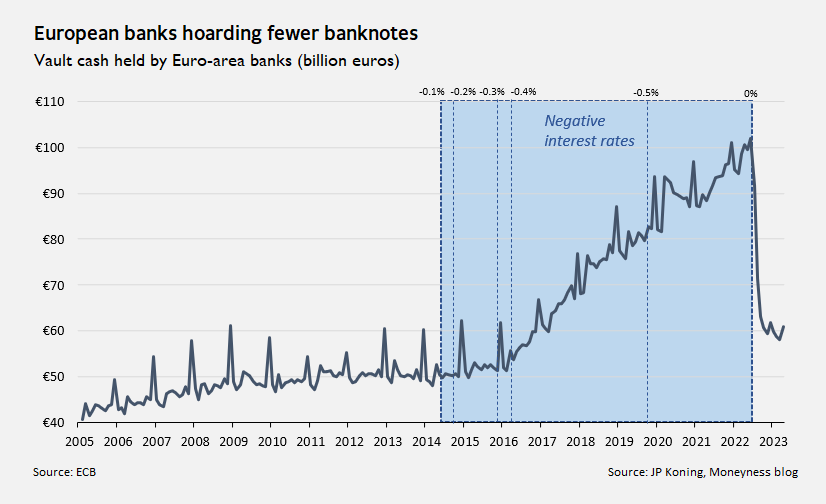

Despite the sharp rise in Fed Funds rate, company net interest payments have actually fallen.

“We have concluded that a sizeable proportion of huge, fixed-rate borrowings during 2020/21 still survives on company balance sheets in variable rate deposits. Companies have effectively played the yield curve in reverse and become net beneficiaries of higher rates, adding 5% to profits over the last year instead of deducting 10%+ from profits as usual.”

There has been a “seismic shift” in global financial markets – “the use of collateral, notably in the form of government securities” becoming “ubiquitous” at the cost of directly assessing borrower cash flow.

Pushed along by policy this switch from relationship to transactions banking has resulted in an unprecedented broadening and deepening of financial markets, especially derivatives.

Yet, this has also created huge vulnerabilities in financial markets, according to a new BIS article.

Podcast advertising leads to pretty good returns for brands.

“After conducting a study with 250 advertisers and marketers, it says two-thirds (67%) of podcast ad buyers say that every $1 spent on podcasts returns between $4 and $6 for their brands.“

Yet SPOT is struggling to capture this – why?

This blog post covers a lot of reasons. For example:

“[What’s] most misunderstood about Spotify is Spotify doesn’t get to monetize all the podcast content that they have. So in the most recent quarterly earnings report, they say that they had 5 million podcasts on their platform, but 99.9% of those podcasts, Spotify does not get to monetize.“

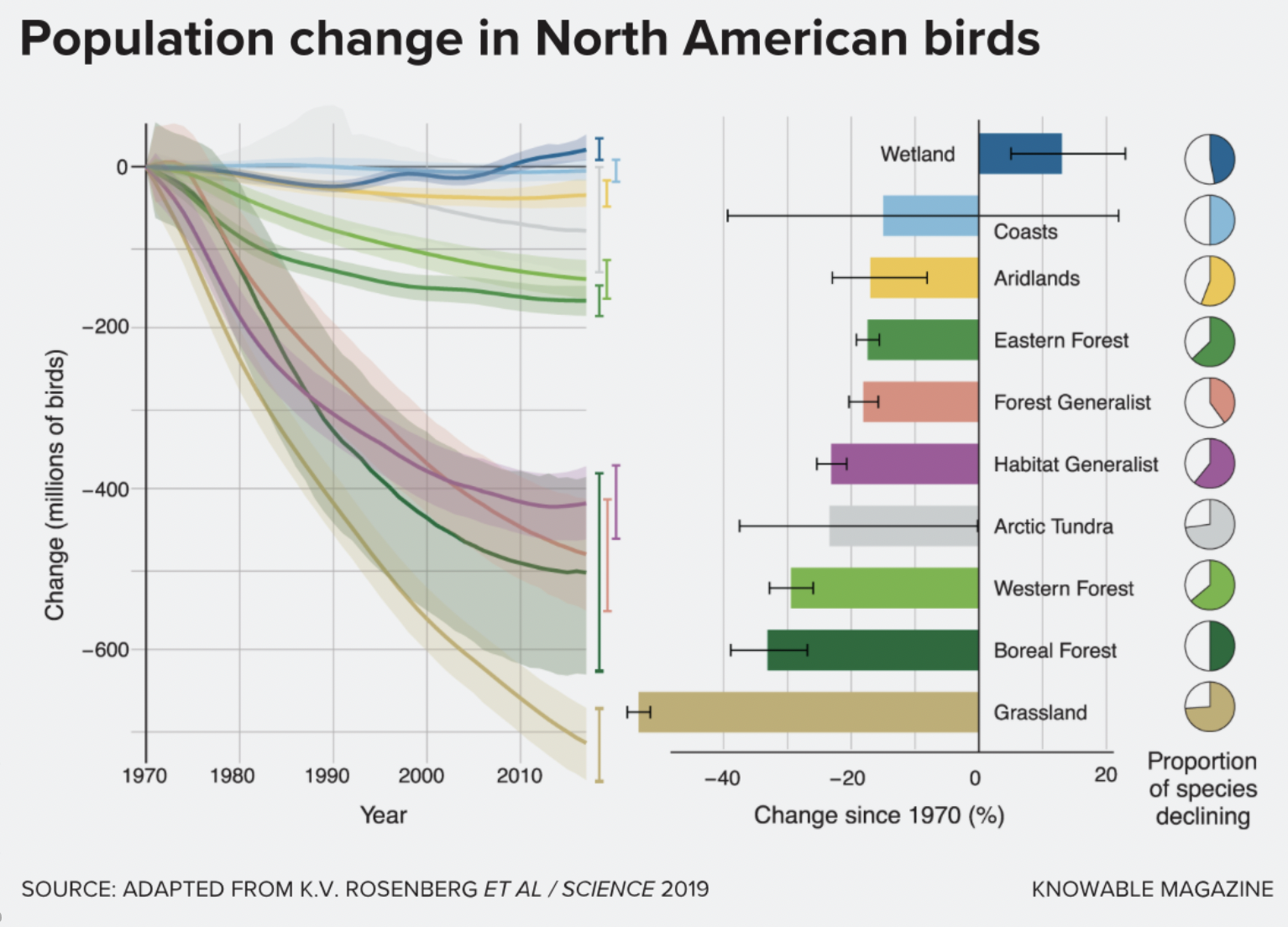

“Since 1970, the team reported in Science in 2019, the number of birds in North America has declined by nearly 3 billion: a 29 percent loss of abundance.“