“Engineers at Tesla Inc. have developed a new process that they claim will reduce EV production costs by 50 percent, while reducing factory space by 40 percent.“

The so-called “unboxed” system – “focuses on eliminating linear assembly lines and producing more subassemblies out of large castings“.

One such effect comes from the drugs themselves – anecdotally they seem to suppress addictive behaviours.

Another is a boon for minimally-invasive skin tightening devices (if you want to read full transcript two-week free trial here).

This interview with the scientists that originally investigated GLP-1 is also interesting to read – especially the point that repulsion to food might reduce these drugs’ long-term use.

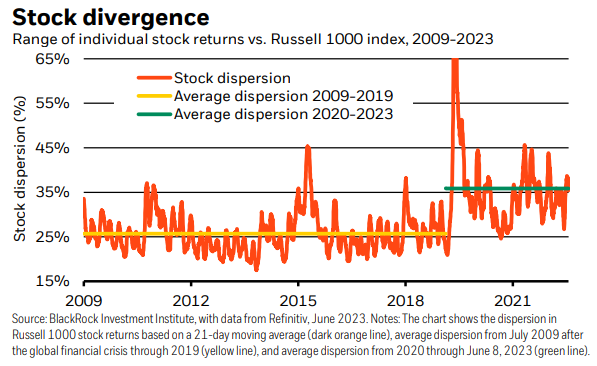

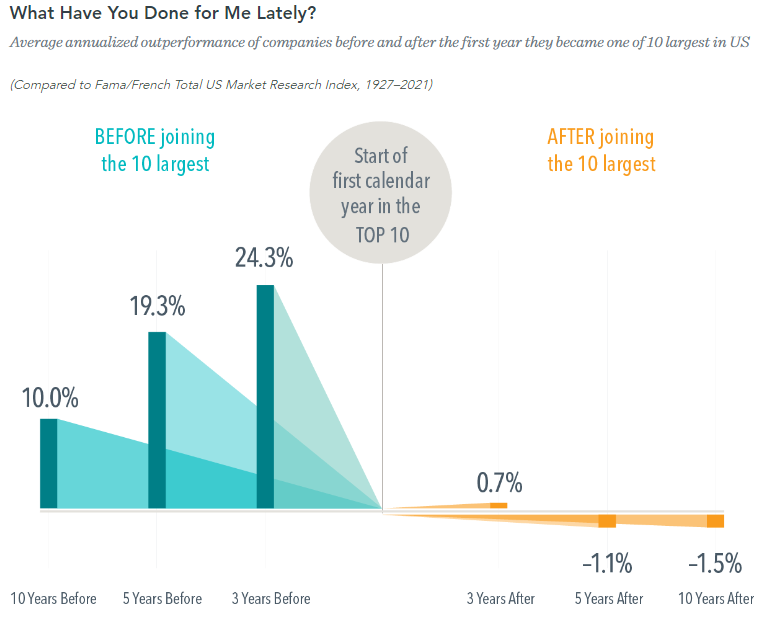

High active share – where portfolios differ markedly from the benchmark – does well (+2% pa outperformance) but only if holding periods are over two years.

So having high active share isn’t enough if the fund trades a lot.

Being patient isn’t enough – as those with low active share do worse.

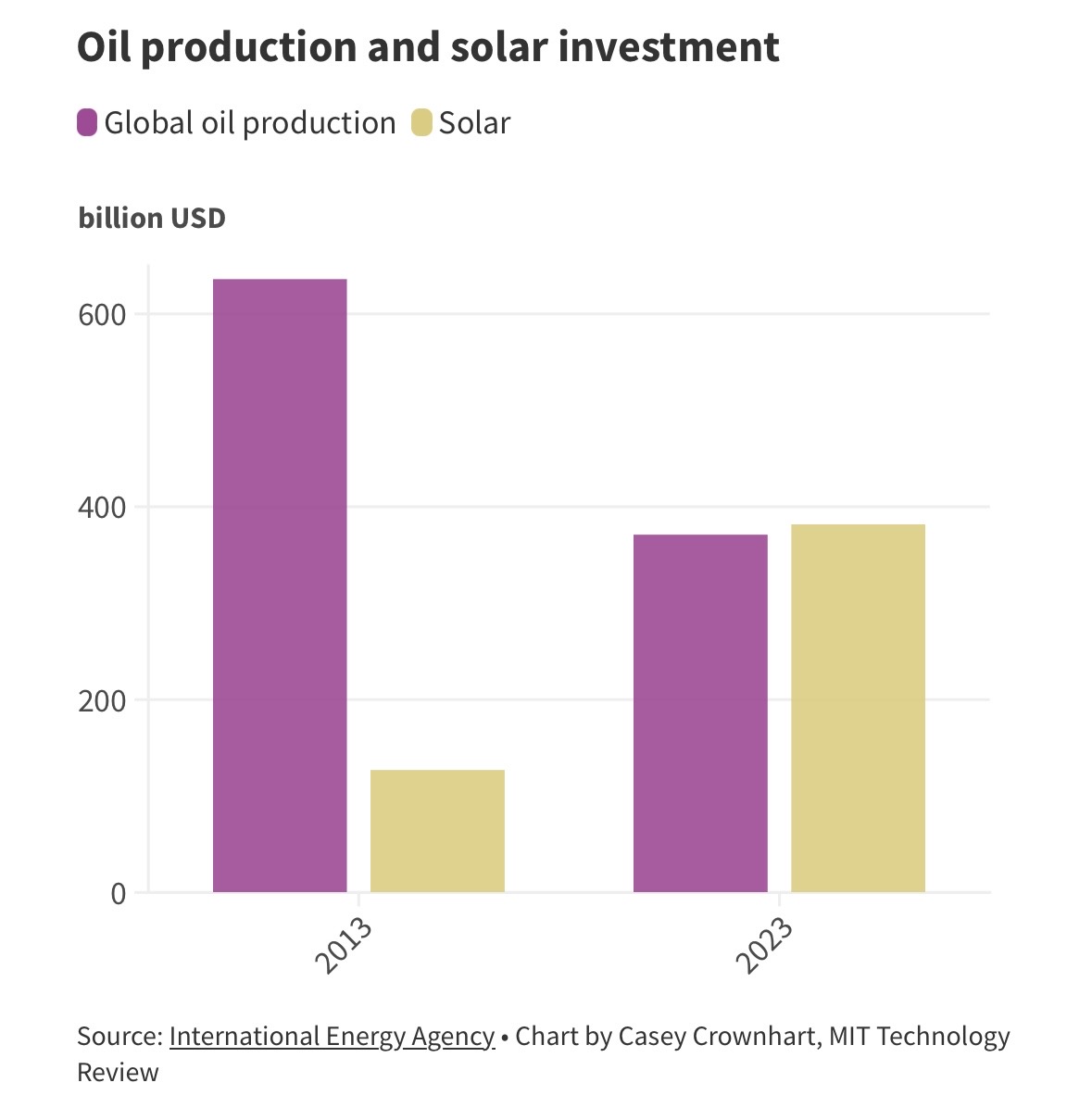

“In 2023, for the first time, investment in solar energy is expected to beat out investment in oil production. It’s a stark difference from what the picture looked like a decade ago, when oil spending outpaced solar spending by nearly six to one.”