Interesting analysis of Tesla’s purported business model compared to other automotive manufacturers – make cars that don’t break vs. the razor/razor blade (i.e. zero margin cars with high margin service and parts) typically adopted by others.

“Tesla does not have an existing fleet and that the auto industry, the reason incumbents succeed and newcomers fail, the biggest reason is that the incumbents have a large fleet, and they’re able to sell new cars at close to 0 margin and then sell spare parts at a very high margin, sort of razors and blades type thing.“

NB to access all the transcripts you can try Stream for free for two weeks.

In case you missed it – Loeb’s latest missive from Q1.

His purchase of UBS is interesting – though CS will undoubtedly have more skeletons (see here) and lose more AuM (as clients diversify), the uplift to UBS book value (74% accretive, putting UBS post deal on 0.74x P/TBV), state loss guarantees (CHF 9bn post first 5bn), and liquidity provision (CHF 100bn) are all positives.

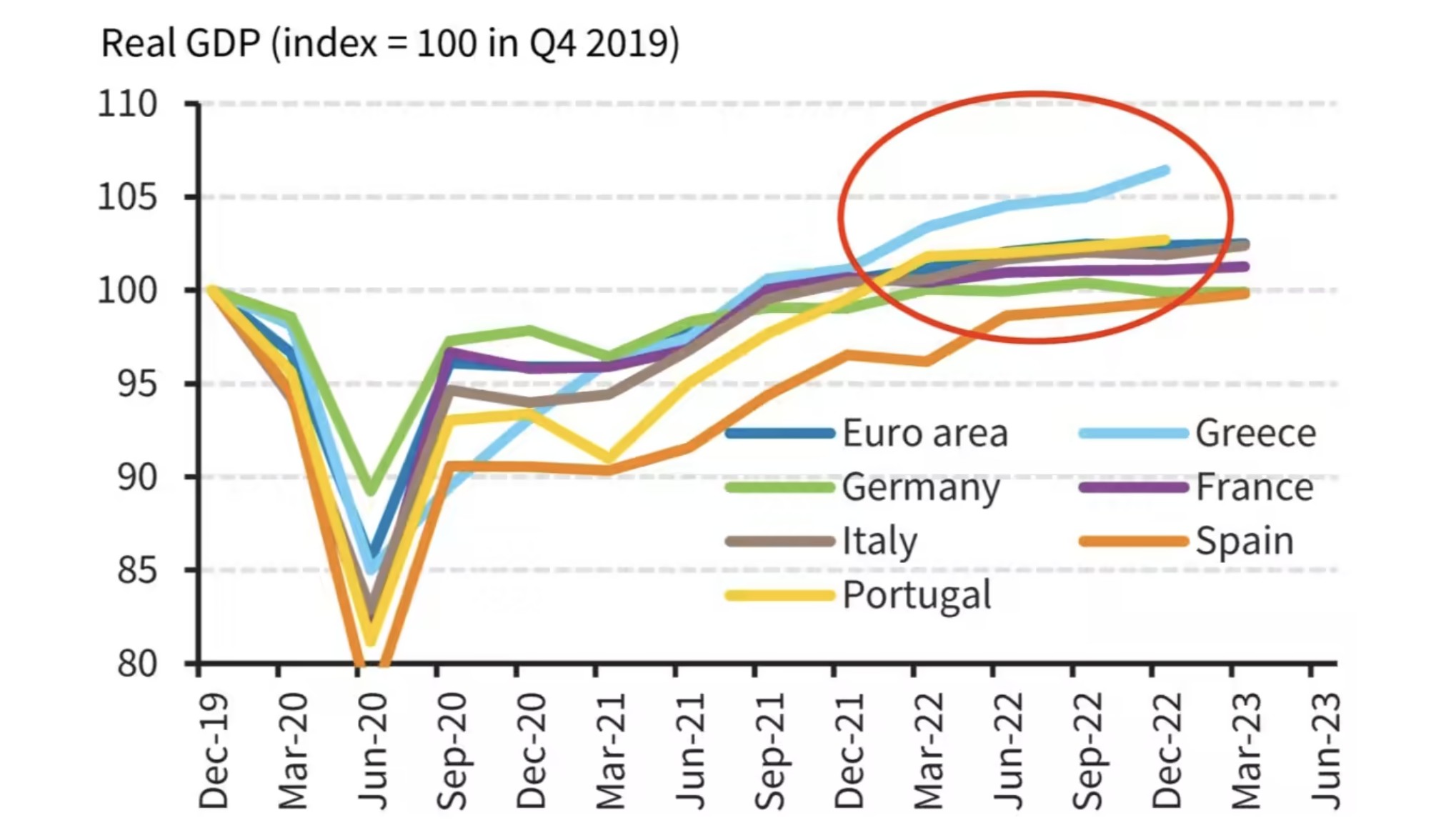

The Greek economy is doing rather well, and starting to peel away in terms of growth.

Barclays, via FT Alphaville, argue it might be entering a third positive “megacycle”.

This analysis agrees – “Greece is growing, investment is booming, employment prospects are improving, the number of businesses is moving up, salaries are increasing, and the country is becoming less poor, not more“.

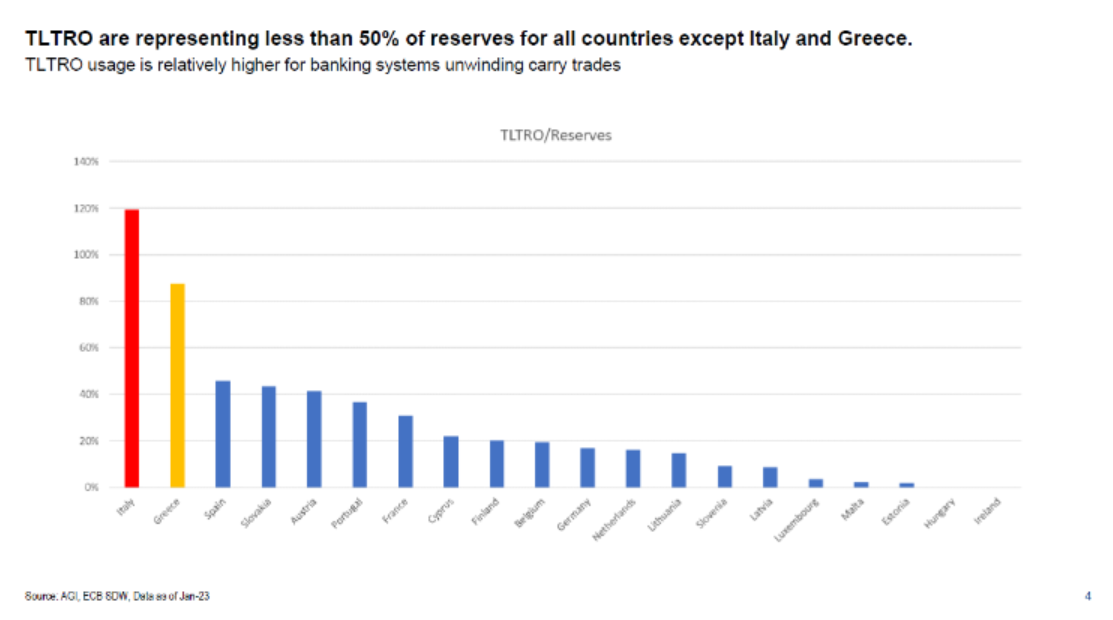

Italy and Greece stand out as still holding huge TLTRO balances relative to reserves.

This could be a painful unwind as these obligations are very cheap and backed by illiquid (as defined by current standards) assets, hurting liquidity coverage ratios.

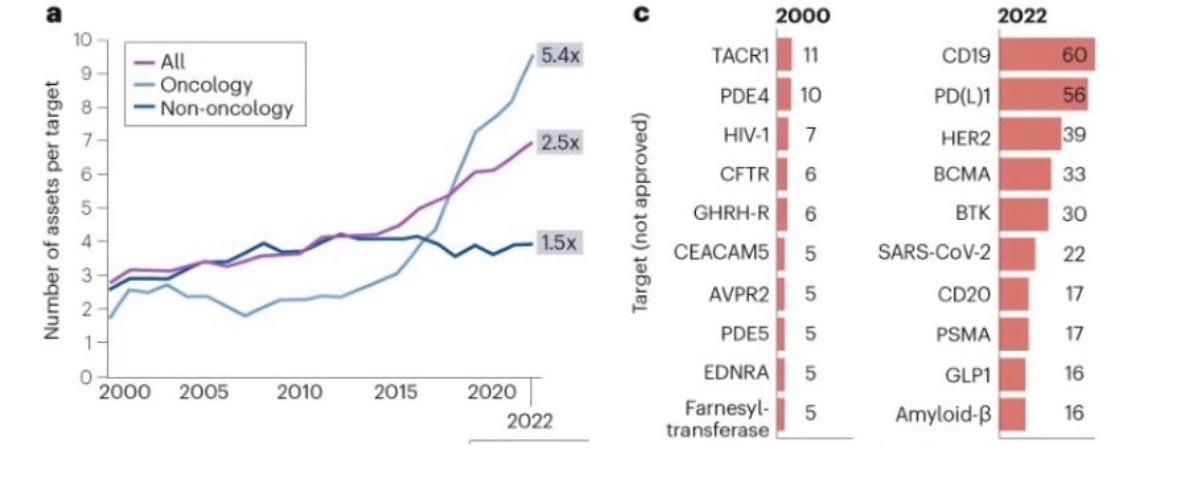

“An analysis of biopharma pipelines shows that the average number of assets per target investigated has more than doubled: 3 assets/target in 2000 to 7/target today. The number of assets in clinical development is outpacing the number of biological approaches, particularly in oncology.”