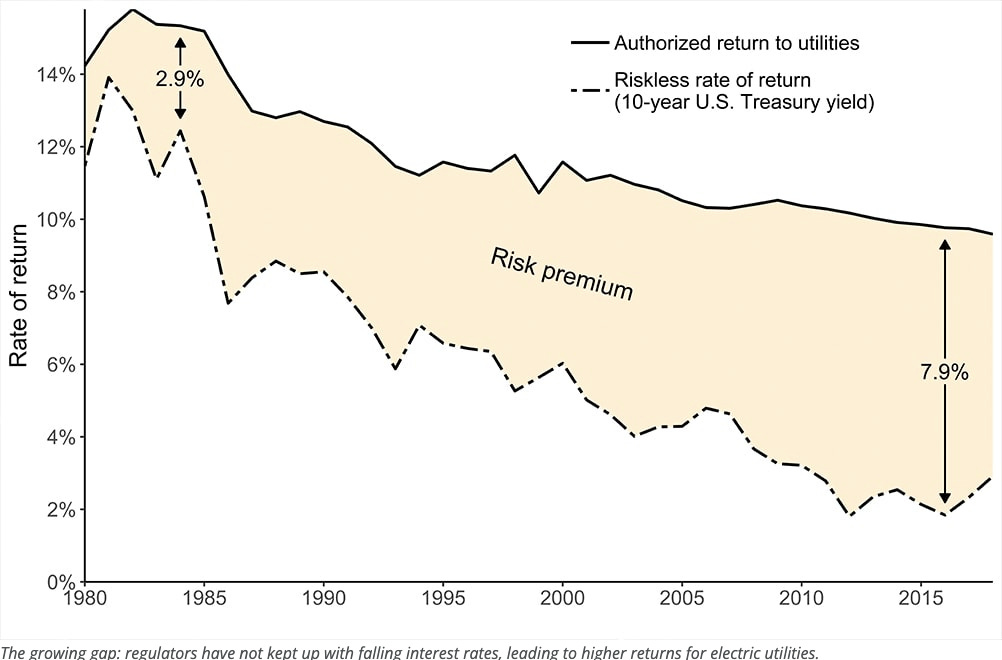

Just four companies serve 90% of the technical testimony utilities use to calculate the rate of return in the US.

“In 2019, two experts at Carnegie Mellon, Paul Fischbeck and David Rode, analyzed 1,600 rate cases over 40 years, and noted the “balance between utility companies and their customers has been shifting over time, in favor of the utilities.” What investors were being paid to take risk in putting money into a utility in 1980 was about 3%, today it is nearly 7%.”

DE Shaw write rarely and this piece is about what an optimizer, both used systematically and in conjunction with discretionary decision making, can teach investors.

Key lesson – focus on the portfolio as a whole not single trades.

National Institutes of Health (NIH) is currently facing chaotic cuts – this article does a decent job laying out how things like a capping indrect spending can only be done via Congress and generally the state of the NIH.

Stripe did $1.4 trillion payments volume in 2024 – it is worth reading their annual letter.

Topics include AI Economy (their data shows top 100 AI firms reach $5m ARR in 24 months vs. 37 months for their top SaaS firms in 2018), vertical SaaS, stablecoins, Europe.

“Consumers of all age groups are using around four different fragrances regularly, which is a significant change from a decade ago when they had one signature scent.“

“Some people talk about the ‘Deep Seek Syndrome,’ saying, ‘You’re overspending, you’re spending $500 billion, you’re overspending! You can save so much more by spending less.’ But I think they are looking at it the wrong way. How much percent of GDP will be replaced by a billion-dollar smart system? I would say at least 5% within 10 years. That 5% is $9 trillion—or if it’s 10%, it’s $18 trillion. So, somewhere between 5% to 10% of today’s GDP will be replaced by this superintelligence. Well, if that’s the amount of return, you shouldn’t be scared of spending a few trillion dollars. If the return is $9 to $18 trillion per year, why should you save? Why should you try to be efficient? For what? I don’t get it. Just a little difference makes a huge return on your market share.” – Softbank CEO Masayoshi Son

Source: A good smorgasbord of quotes from recent transcripts.