RISC-V, the royalty-free open-source instruction set architecture, is worth keeping an eye on especially as Arm convulses its way back to the stock market.

The December 2022 summit (and this great write-up) offered a deep feel of the status of RISC-V.

Bold statements abounded – “It’s really important that you get this. RISC-V is inevitable. RISC-V is going to have the best processors. And RISC-V is going to have the best ecosystem.”

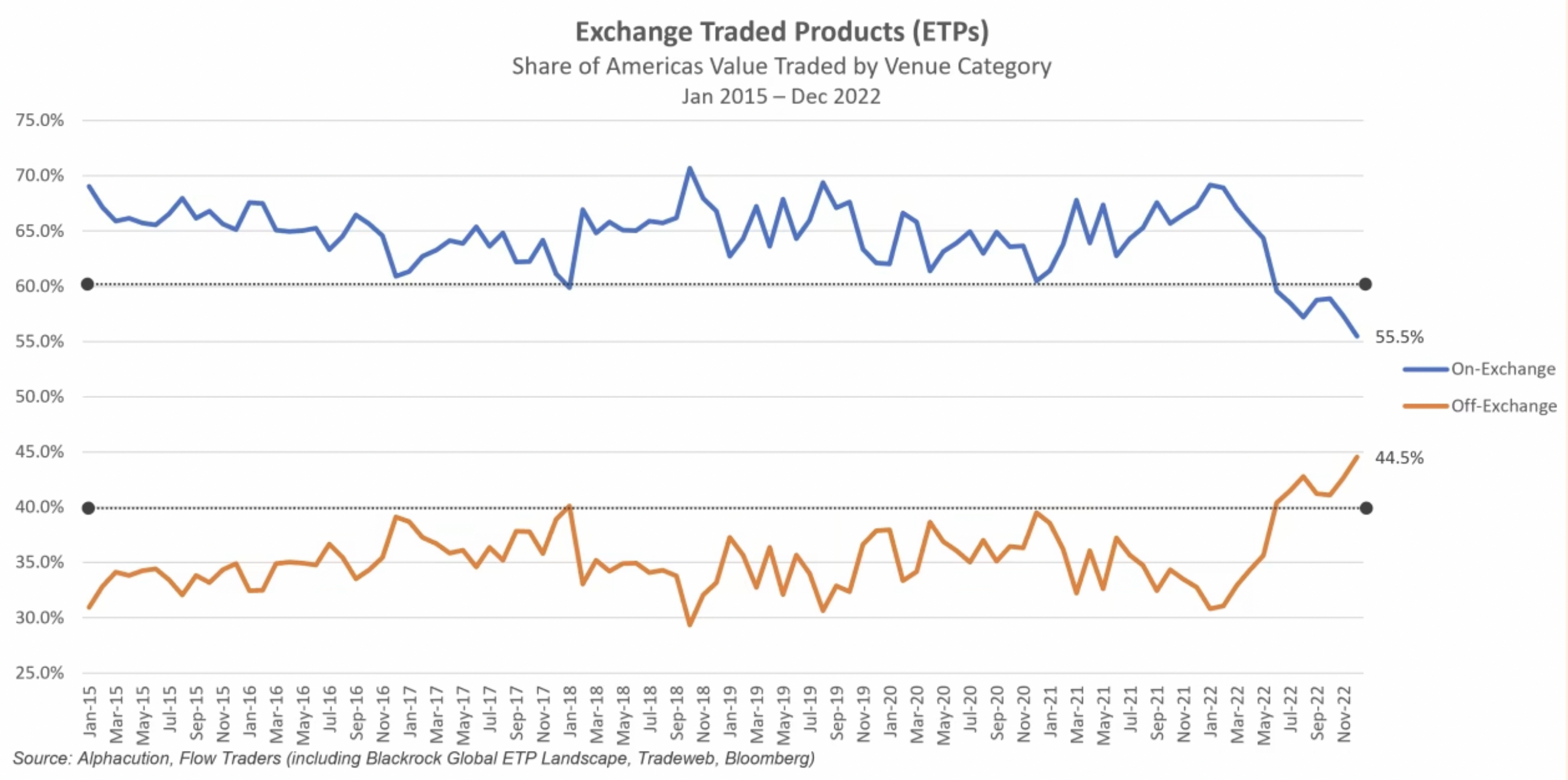

2022 saw a new record in off-exchange trading of US ETFs.

Part of a broader trend where trading off-exchange in US equities went from 35% in 2015 to 43% last year.

Yet, as the FT Alphaville article notes, “ETF shift from lit to off-exchange trading has actually been even starker than it has for equities as a whole“.

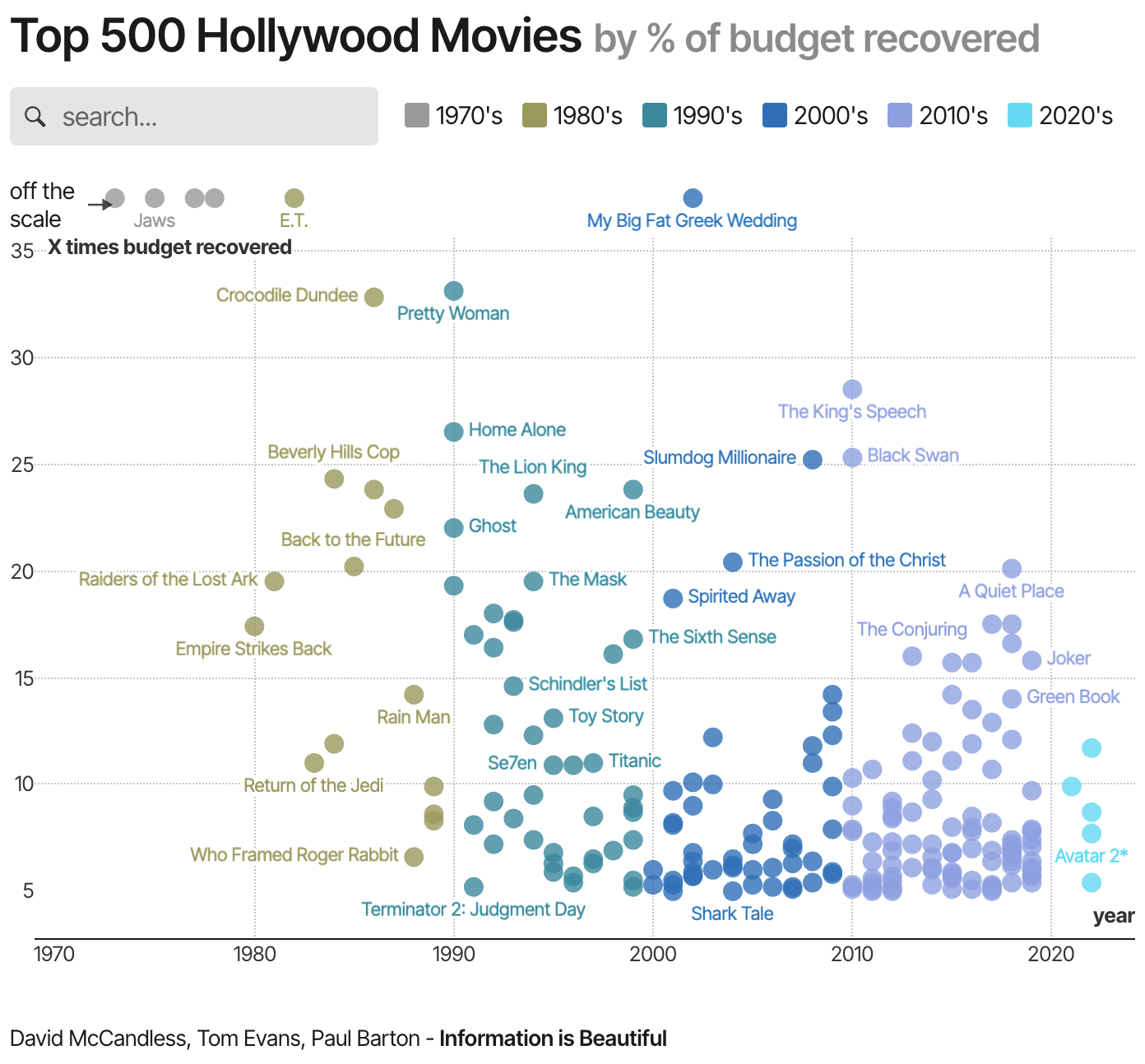

Films often get measured by gross box office, with Avatar (both of them) reigning supreme on this measure.

However, using a measure of return on investment (percentage of budget recovered) throws up an alternative perspective.

Winners on this measure are E.T. (7,552%) but also films like “The King’s Speech (2,849%), Home Alone (2,648%), and breakout sleepers like Crocodile Dundee (3,282%), Slumdog Millionaire (2,523%) and … er, Black Swan?“

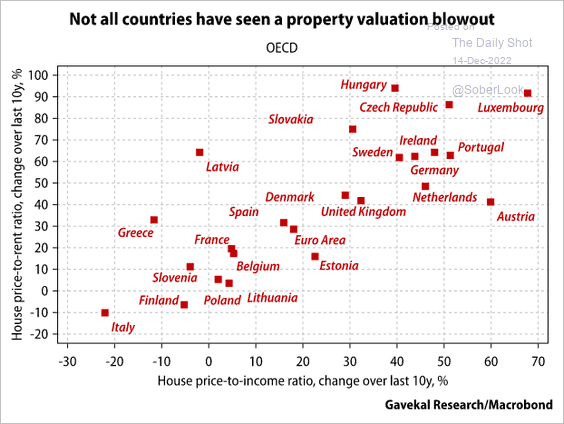

IRF’s The Cut is a fortnightly publication highlighting the latest original and thought-provoking research from a selection of high-quality and differentiated Research Providers.

Interesting use case of GPT3 – to model economic agents – as was done in this paper.

“These models can be used the same way economists use homo economicus: they can be given endowments, put in scenarios and then their behavior can be explored—though in the case of homo silicus, through computational simulation, not a mathematical deduction“

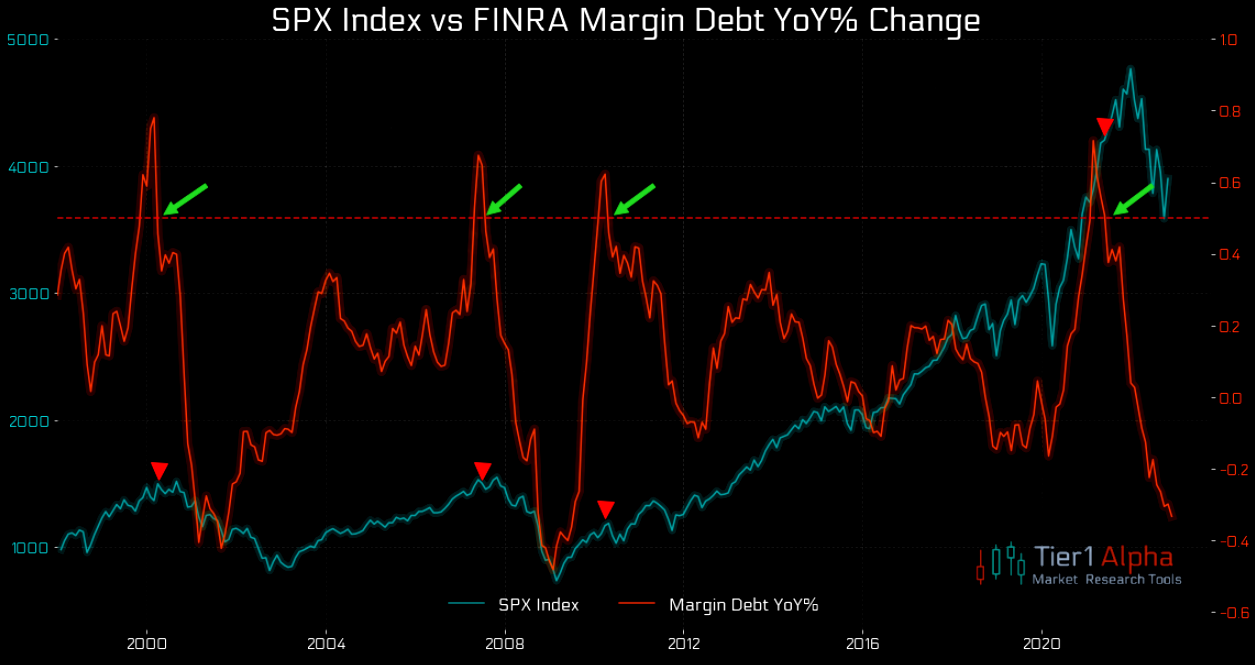

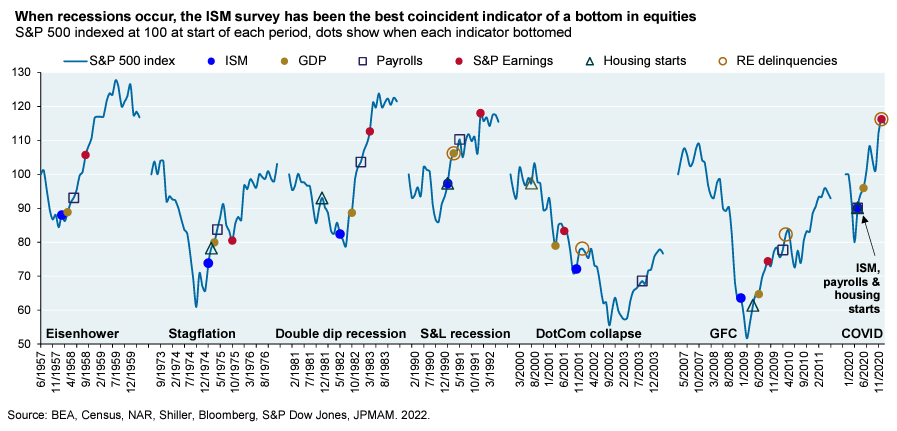

“As shown below, in the history of US recessions (with the exception of the dot-com collapse of 2001), equity markets bottomed well before the bottom in GDP, payrolls, S&P 500 earnings and housing starts and the peak in household/corporate delinquencies. The ISM survey has been the most reliable coincident indicator of a bottom in equities“.