Did you know that one team of funders supported all but one of the 18 scientists who received the Nobel Prize in genetic molecular biology research, funding this revolution.

This was the Natural Science Division of the Rockefeller Foundation which operated during the 1930s – 1950s, under the leadership of Warren Weaver.

A must read history full of lessons for today’s science funders.

“Weaver saw himself, instead, as a “manager of science.” He led his small team of program officers in a highly opinionated grantmaking process that focused on the organizational and social environments of research institutions over the specifics of any individual project. And once his team selected a field to focus on, it funded people over specific ideas.“

“The future of semis will be designing ever more specific chips for ever more specific uses. This change will take many years to play out, but the transition has already begun. This is going to upend the semis industry to the same degree that consolidation over the past 20 years has.“

“at the end of Jane Street internships: interns get a stack of 100 poker chips and spend half a day getting asked brainteasers and then betting on their confidence in the answers … This would actually be a pretty fun way for a math-minded person to spend a few hours, if it weren’t so high-stakes: the winners get a job from which people routinely retire rich in their 30s, and the losers… don’t.“

Intriguing transcript call from a former director suggesting Aladdin could be spun-off from Blackrock [To read follow this link and get a free two week trial of Stream].

Alladin is big (2021 the Technology Services Business at BLK, which is mostly Aladdin, delivered $1.3bn of revenue) and appears to be a winner takes all business (more data means it is better at doing its job).

This was a brilliant (paywalled) history of Alladin for those interested.

Few contrarian buyers out there, and for many startups there is plenty of cash in the bank.

“In 2021, there were more than 3,000 M&A deals globally involving a VC-backed company getting bought, according to Crunchbase. Halfway through the third quarter of this year, just under 1,600 startups have found a mate in the market.“

“I couldn’t help reflecting that there was a fine balance between the stringent requirements of the regulator and what our potential investors would like to see. For the PRA [Prudential Regulation Authority] we needed to be people who had done it all before, who knew how the committees and governance processes worked, and who were fully aware of our responsibilities to look after our customers’ money. On the other hand, for the private equity (PE) world we needed to appear as hard-headed business people who were going to sweat the assets and run a traditional high-return banking business. Meanwhile, any potential venture-capital investors would be on the lookout for a bunch of smart people who wanted to change the world.We just needed to fulfil each and every role somehow! Or rather, some people on the team would have to be all three people on the same day, while others picked a side and stuck with it.“

Brilliant condensation of the tensions of a startup bank by Boden, the founder of Starling (h/t Net Interest)

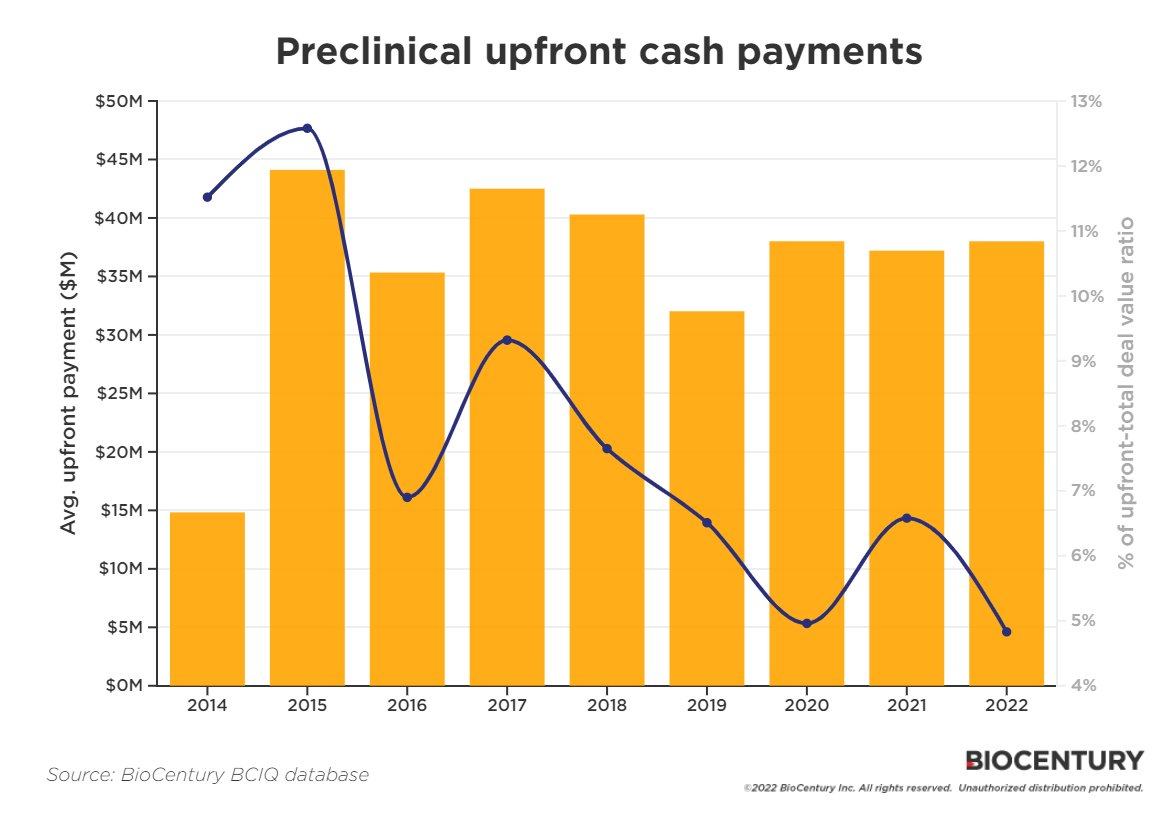

Interesting dataset showing that, despite a fairly constant $ amount of upfront payments, its % of a total biotech licensing deal’s value has fallen to a low for pre-clinical assets.

Derivatives and shorting have made their way into the private market.

Selling interest increased to 80% of open order interest at Caplight, while the buy side has dropped to 20%, according to Javier Avalos, CEO of the private-market derivatives marketplace. It was previously fairly even or a 60/40 split, he said. “We basically saw the demand side of the Caplight marketplace go away for the past few months,” he said.

One interesting aspect of tech is how circular it is, making it prone to downside leverage – “Tech, unlike other sectors, disproportionately sells to itself.”

“The circularity goes beyond VC investments,” he added. “Today major tech companies incubate their own customers at a pace and scale not seen in any other industry.”

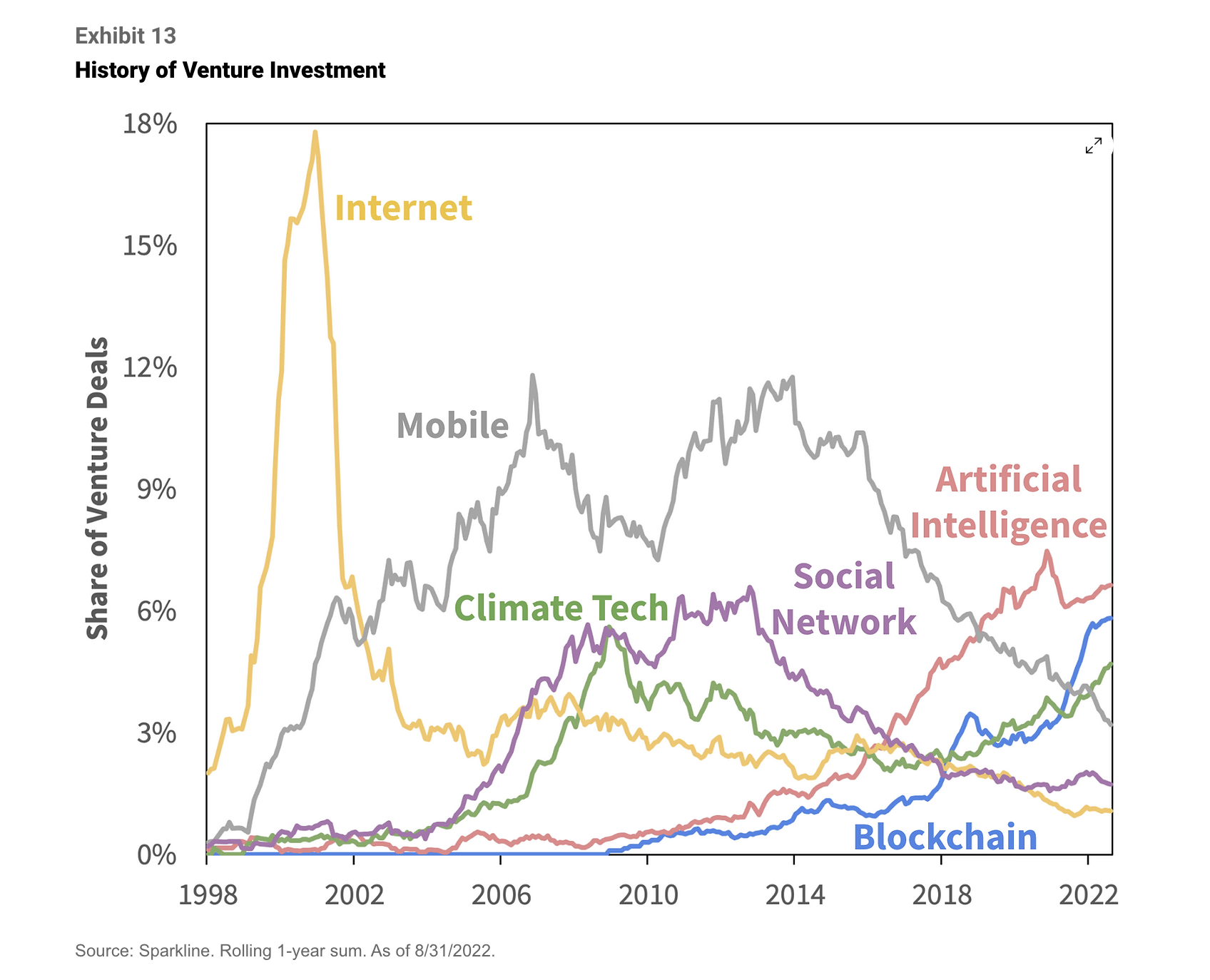

Using a machine learning model Sparkline Capital were able to cluster firms in similar technologies and then look at how venture investment in these tech clusters evolved over time.

This leads to the following chart of cycles.

“In the dot-com bubble, venture capital firms threw money at internet companies. Next, Blackberry and iPhone ushered in the mobile age. Then, Facebook’s success sparked a wave of investment into social networks. Artificial intelligence grew steadily over the past decade, while blockchain burst on the scene a few years ago. Climate tech investment faded after an initial burst but is now seeing a resurgence.“

A large alternative asset class you probably haven’t heard of is litigation financing – “transactions in which a third party provides capital (debt, equity, or a hybrid) to one of the parties to a legal claim (a plaintiff or law firm) in exchange for a financial interest derived in part from the outcome of the claim.“

This is an excellent comprehensive up to date paper on this sector. The full paper is here and a great summary is here.

The asset class is estimated to boast 20%+ returns and has grown to a dedicated AuM of $12bn.

Outsourcing in the biotech and pharma industry continues unabated, boosting contract research organisations (CRO) like IQIVIA, Labcorp etc.

Interestingly, consolidation has been a big feature of the industry, and this Stream expert call (sign up for free two weeks to access) suggests more is to come.

Interesting first hand account of how Monzo grew from nothing to 1 million users in three short years.

Tom credits – a great product (compared to competition) that was a delight to use, a brightly coloured card, and network effects – “if you had 3+ friends on Monzo when you joined, you had a 70% chance of being a WAU [weekly active user] by day 90, versus only a 50% chance if you didn’t have any friends on the platform.“

Strikes me as a very important move by the US towards “open access” academic research.

By 2026 all US federal agency funded research must be free to read immediately on publication.

This has been talked about for a very long time.

In a recent transcript from Stream by AlphaSense (sign up for two free weeks here), a former Elsevier Director, argued the effect on RELX business will be a “small negative” as they will find ways to charge for ancillary parts of research (reviews, data etc). The hit to smaller publishers will be worse.