A really beautiful must read piece written by a self-professed supply chain nerd.

Weaving in analogies that bounce in time – from the internet age to husbandry – supply chains are brought to life.

“Supply chains are a new class of engineered-emergent artifact, one that includes a few other globe-spanning things like the internet, the air travel system, and low earth orbit, that exist at a level of Gaian phenomenology, terraforming, and planet-scale husbandry.We only ever catch local glimpses of these things.”

“We have to understand these beasts, in all their evolving, learning glory, while living within their bellies.“

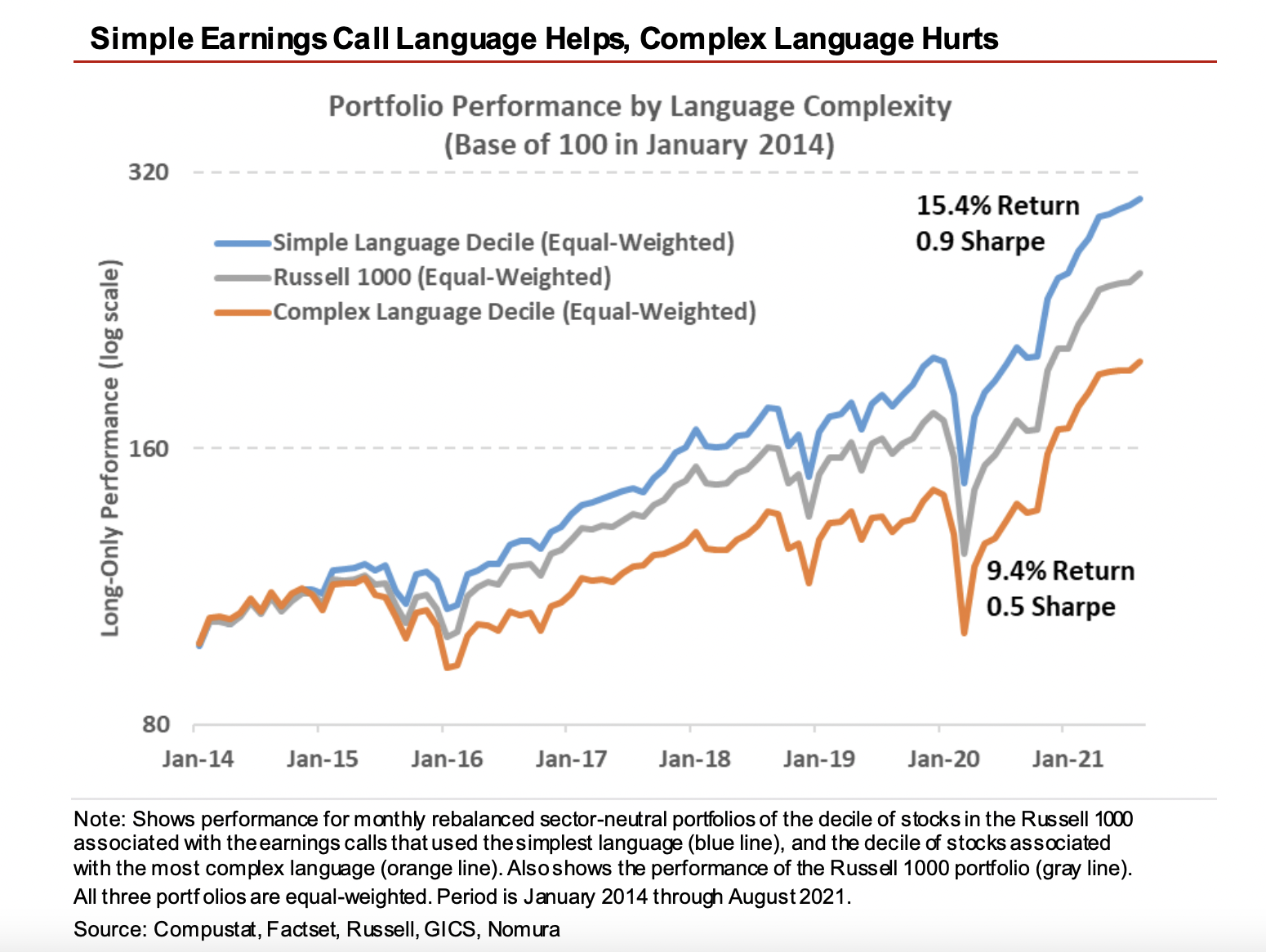

The type of language used in earnings calls has a significant impact on stock returns.

According to Nomura, simple language (as measured using Gunning Fog Index) leads to higher returns and a considerably better Sharpe ratio when compared to complex language.

This is distinct from earnings call length – which doesn’t correlate to complexity.

For those interested we previously posted further interesting stats on language in company publications.

Orwell offers a lot of advice on writing well, a vital skill for any investor, in his essay “Politics and the English Language”

This postpulls out some of the main “bad habits” to be avoided.

It matters because writing clearly reveals understanding.

“You can shirk it by simply throwing your mind open and letting the ready made phrases come crowding in. They will construct your sentences for you — even think your thoughts for you, to certain extent — and at need they will perform the important service of partially concealing your meaning even yourself.”

“A scrupulous writer, in every sentence that he writes, will ask himself at least four questions, thus: What am I trying to say? What words will express it? What image or idiom will make it clearer? Is this image fresh enough to have an effect? And he will probably ask himself two more: Could I put it more shortly? Have I said anything that is avoidably ugly?“

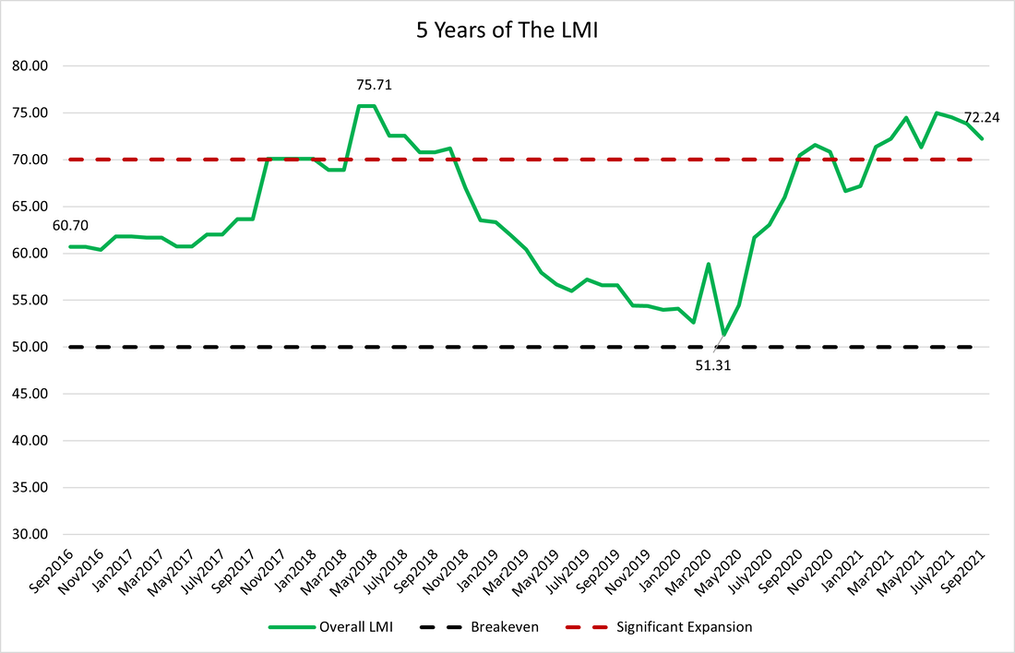

Useful resource assessing the state of the logistics industry.

The index has been going for 5 years, consists of eight components and is calculated using a diffusion index i.e. readings above 50 indicate expansion.

The current stretch above 70 – meaning significant growth – is the longest on record.

Will be interesting to watch if the situation improves and along which components.

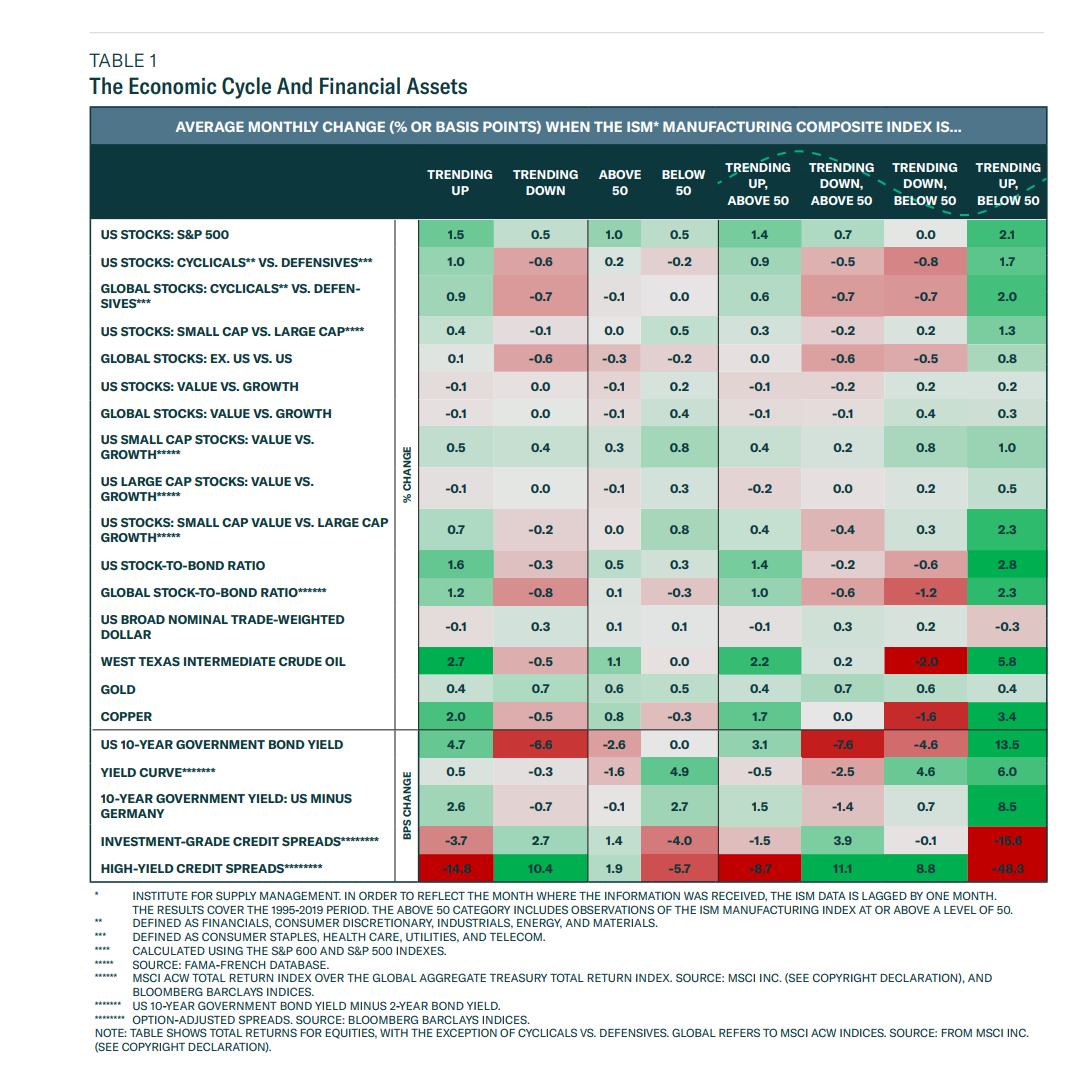

It shows how various financial assets (down the rows) react to the changing economic cycle (columns) as measured by the ISM Manufacturing Composite Index.

It covers the period 1995 – 2019.

Right now we are above 50 on the ISM index (59.9) but trending down.