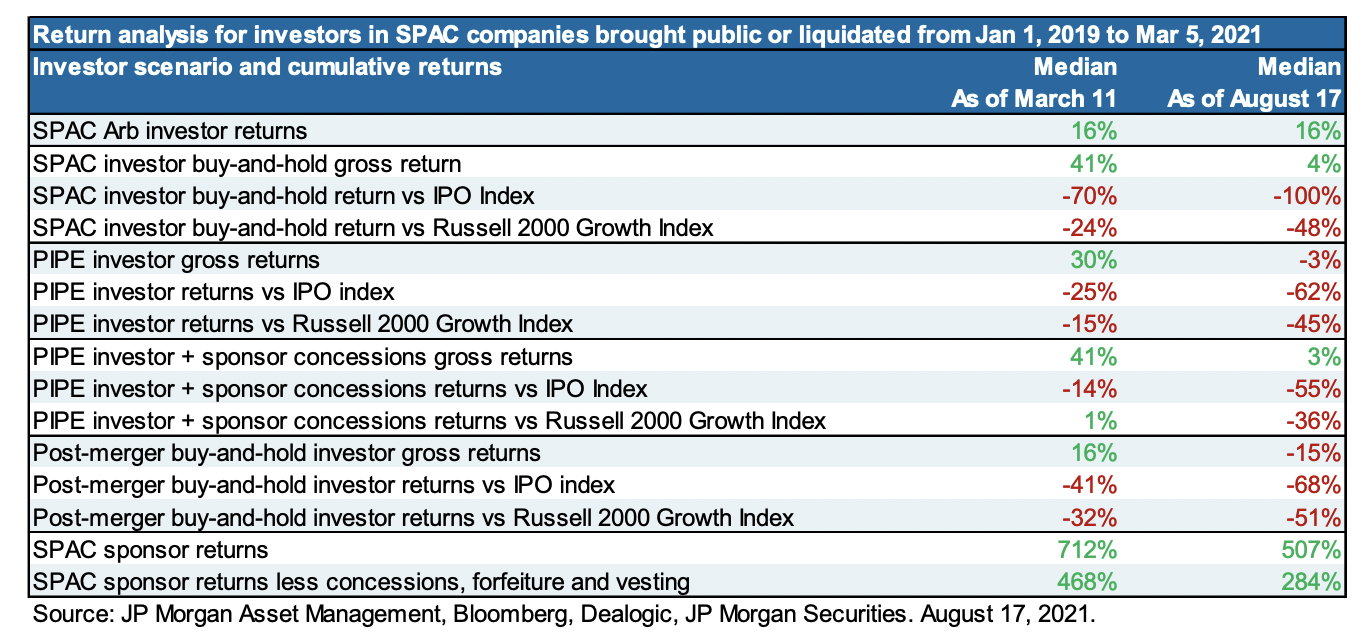

JPM analysed 98 SPAC deals that closed or liquidated from Jan 2019 to March 2021.

It isn’t a pretty picture – “while SPAC sponsors and “SPAC Arbitrage” investors are still making money, it’s an unsightly picture for everyone else in the SPAC ecosystem“.

Things didn’t get any better for the 85 SPAC mergers since March 2021 – the same patterns hold.

This was a great post looking at the crazy things going on recently in the SPAC world.

George Lucas was forced to sell Pixar to fund his divorce.

Venture capitalists, 35 of them, refused to back the firm as did eight strategic partners, but Steve Jobs agreed.

“If we’d had any other investor than Steve, we would have been dead in the water.“

He forced the firm to succeed “He’d berate those of us in management, then write another check”

Pixar was eventually sold for $7bn to Disney “This is astounding considering they could have had us for free in the 1970s when we approached them on bended knee.”

“Splitting a good black jack hand” is a great way to describe how Michael Dell pulled off perhaps the most daring deal of the last decade.

“Before the LBO, he owned 15.6% of his company, shares worth less than $4 billion. Thanks to the miracles of his financial engineering, he will own 52% of Dell and a 42% stake in VMware. The total value of his Dell holdings is $40 billion.“

Craigslist, the world’s largest classified ads platform, was rolled out in a staggered fashion from 1995 to 2009.

This created the perfect testing ground for its impact on 1,500 US daily newspapers.

Researchers found that:

As one would expect local newspapers reduced staff by 6% (14% for those that relied more heavily on classified ads).

There was also a sharp decline in circulation which isn’t made up by other sources of news consumption.

Most fascinating though, there was a significant decline in political content of newspapers (see chart) while things like sport, entertainment and crime didn’t change.

This has very stark implications discussed in the link.

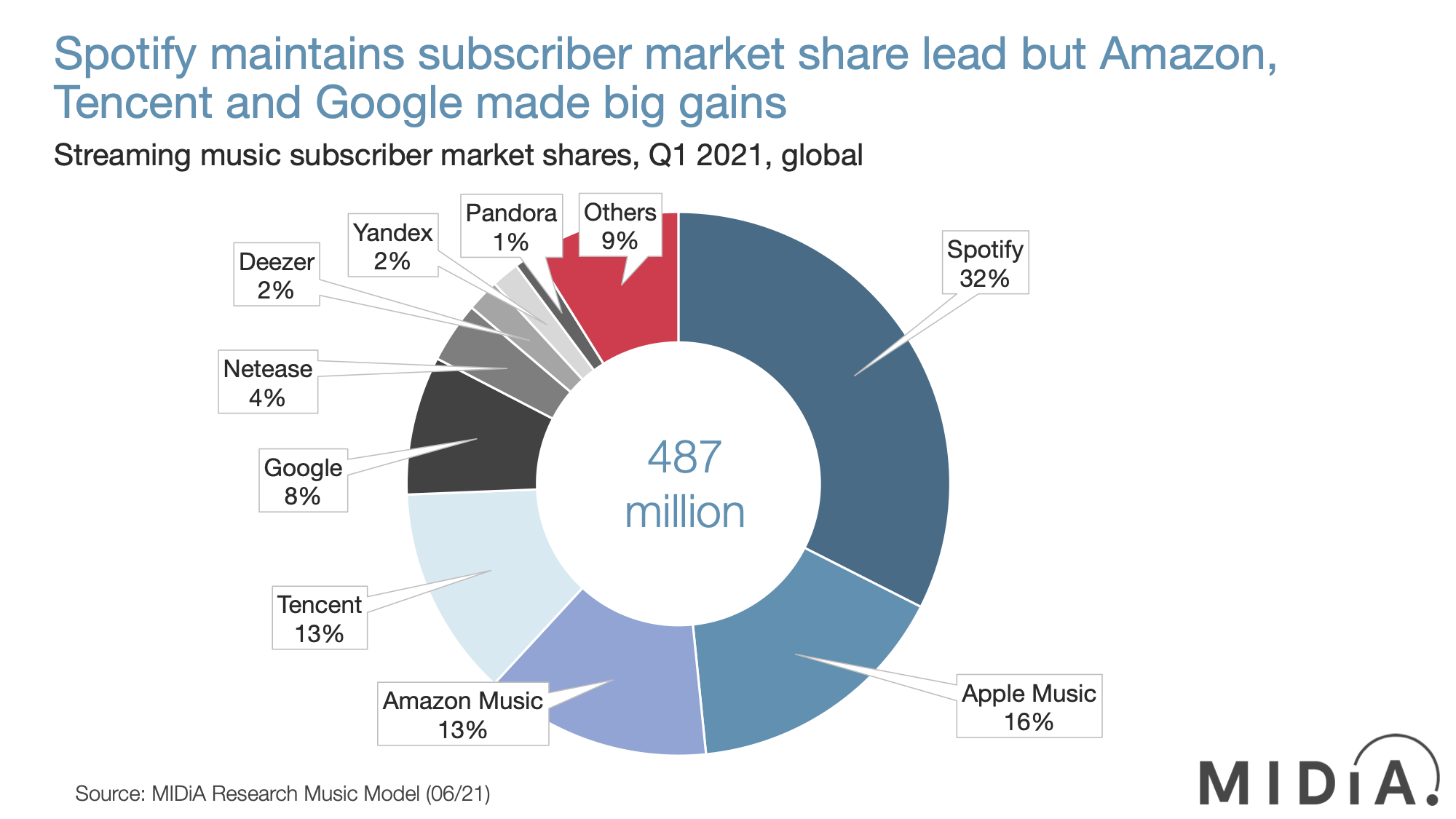

There are 487m music streaming subscribers globally at Q1 2021.

Emerging markets are now central to this market accounting for 60% of all 2020 subscriber growth.

Spotify is still the leader with 32% but has lost two points of market share since Q1 2020.

Google’s Youtube Music has been the standout story – “The early signs are that YouTube Music is becoming to Gen Z what Spotify was to Millennials half a decade ago.“

A really great and rare podcast with the legendary investor.

His points on how to frame buy and sell decisions are particularly good.

As is his view of the UK needing capital to unlock the world-class IP historically generated there and give people ambition to build global platforms instead of solving individual problems.

Finally, his advice to young people about enthusiasm really rings true.

This was a good summary of other points by a former colleague, but the full thing is absolutely worth your time.

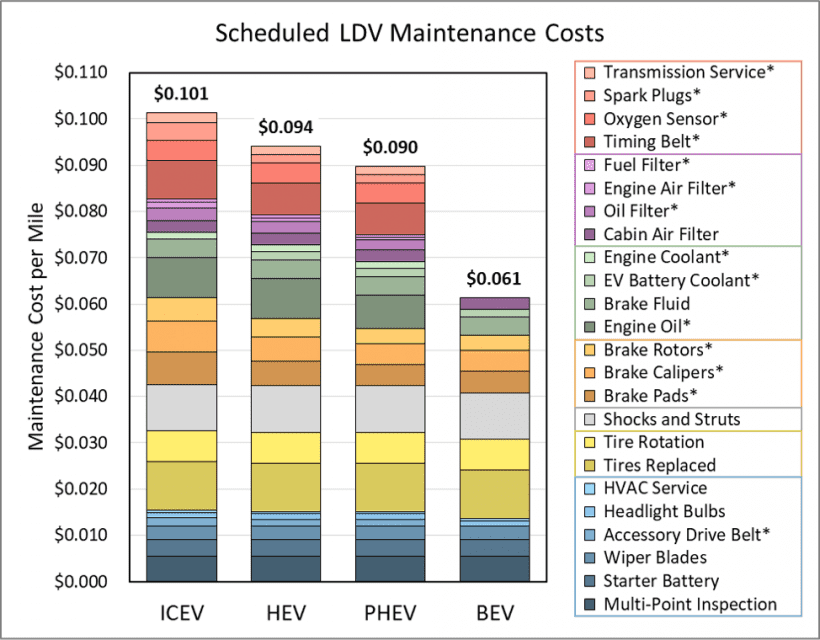

The US government estimate of fleet maintenance costs found that battery-electric vehicles (BEV) have about 40% lower cost when compared to internal combustion engine vehicles (ICEV).

Hybrids (HEV) and plug-in hybrids (PHEV) also save money.

NB this 4c per mile difference across the nearly 2 billion miles federal government vehicles covered in 2019 equates to $78 million a year in savings, and that doesn’t account for fuel costs.