Interesting latest piece (page 15) from Hosking Partners on why the rotation into value stocks will persist.

(1) They perform well at the end of recessions (2) stimulus favours value (3) Covid recovery will be long and is only getting underway now in some countries (4) fund managers are entrenched (5) Interesting ESG angle.

There is also a full webcast that is worth listening to.

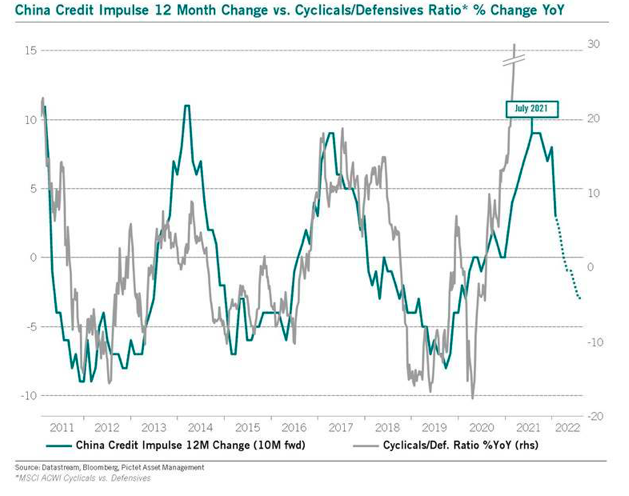

There is a considerable debate raging right now on the future level of inflation, exacerbated by the consensus busting April CPI print (here, here and here).

This piece, written by economists, is worth reading.

It proposes looking at median CPI to construct the Phillips curve, as it better reflects macroeconomic conditions.

The resulting relationship is stable pre- and post-pandemic and suggests, under bullish unemployment scenarios, that implied core PCE could hit 1.8-2.3% by 2023, “broadly consistent with the Fed’s average inflation targeting strategy with inflation modestly overshooting its long-term level following a number of years of undershooting it.“

They also don’t see, unlike others, temporary government spending causing an unanchored inflationary spiral given a better communication framework from the Fed and positive supply side effects of infrastructure spending.

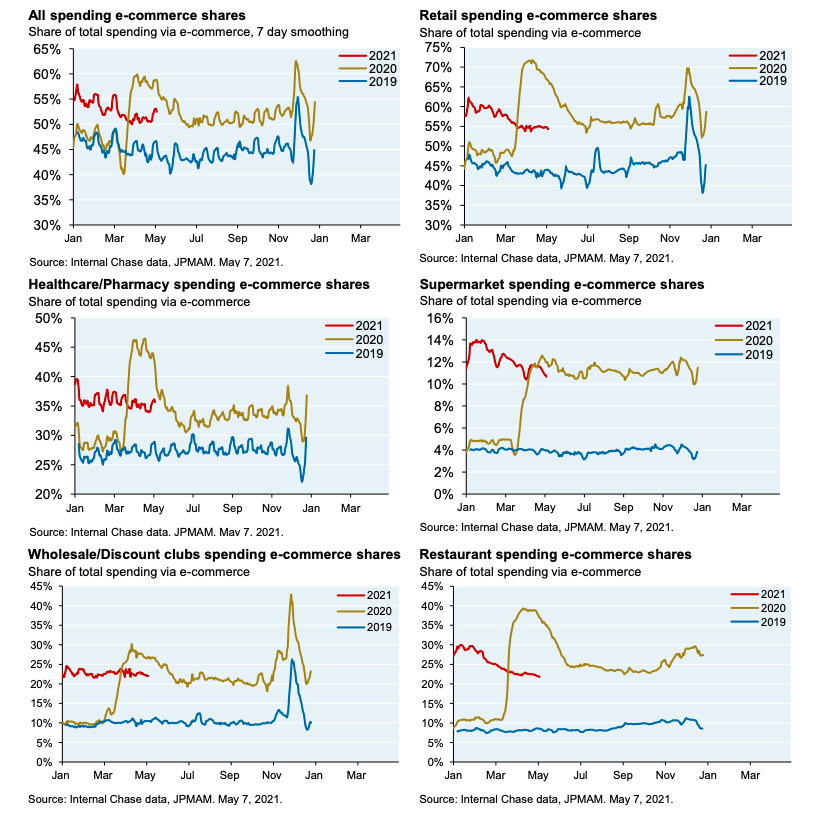

With almost 5 months of 2021 behind us, it is interesting to check in to see how eCommerce sales as a % of total spending are doing across various sectors.

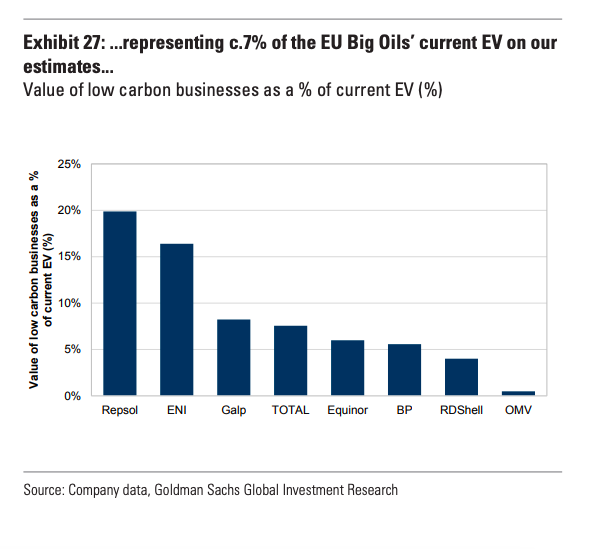

Low carbon businesses (renewable power, retail power and bioenergy) represent an estimated 7% of EU big oil enterprise value (EV) on aggregate with Repsol and Eni leading the pack.

Investment in these areas has really accelerated in the last four years.

This analysis excludes future technologies like hydrogen and electric vehicle charging, that are not material today but are a big part of the transition at these companies.

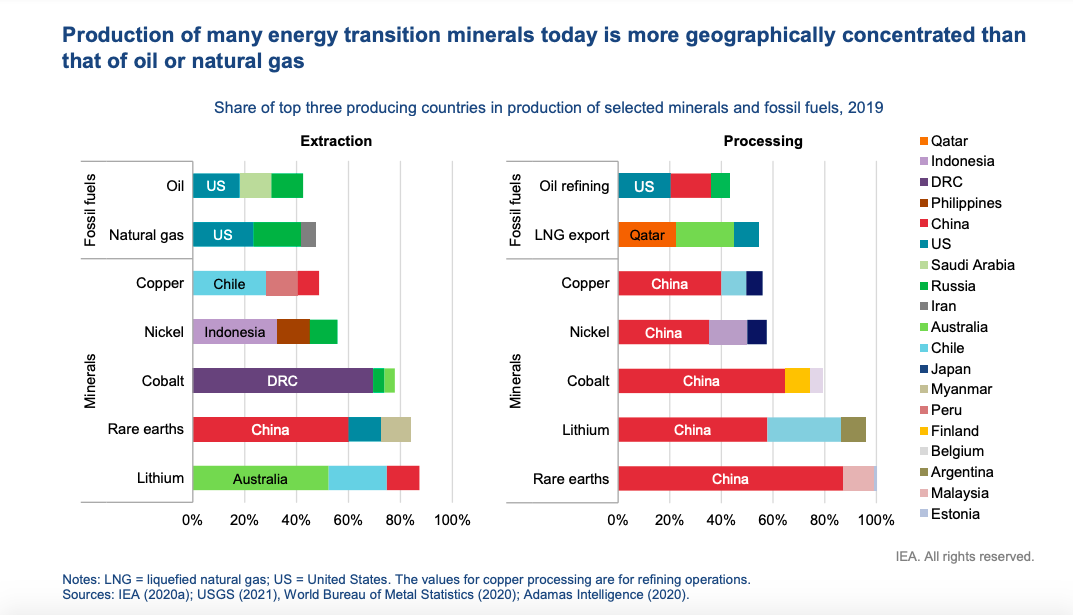

This surge in investment has meant the energy sector is now a leading consumer of minerals.

A brilliant set of short anecdotes each carrying an important lesson.

An example – “When we condemn [the past] for slavery, or for Native American removal, or for denying women their full role in the life of the nation, we ought to pause and think: What injustices are we perpetuating even now that will one day face the harshest of verdicts by those who come after us?“

Really interesting review of Lee Freeman Shor’s “The Art of Execution”

“Shor’s most powerful point is that investment performance is largely dictated by what an investor does after they buy a stock, specifically by how they deal with both losing and winning positions over time.”

The book uses a dataset of 30,874 trades made by 45 top managers who ran money as part of Shor’s “Best Ideas” fund from June 2006 – October 2013.

This is a useful paper on a new metric – the market expected return on investment – that aims to give a more accurate view of returns in a world increasingly dominated by intangible assets.

“Contrary to the conventional wisdom, disinflation is more likely than accelerating inflation. Since prices deflated in the second quarter of 2020, the annual inflation rate will move transitorily higher. Once these base effects are exhausted, cyclical, structural, and monetary considerations suggest that the inflation rate will moderate lower by year end and will undershoot the Fed Reserve’s target of 2%. The inflationary psychosis that has gripped the bond market will fade away in the face of such persistent disinflation.“

Apple is upending the traditional (x86) CPU markets.

It is doing this by offering the same M1 chip in laptops, tablets and desktop PCs.

The same M1 chip at all price points (from $699 to $1,699).

“Apple’s willingness to position the M1 across so many markets challenges the narrative that such a vast array of x86 products is helpful or necessary. It puts Intel and AMD in the position of justifying why, exactly, x86 customers are required to make so many tradeoffs between high performance and low power consumption. Selling the M1 in both $699 and $1,699 machines challenges the idea that a computer’s price ought to principally reflect the CPU inside of it.“