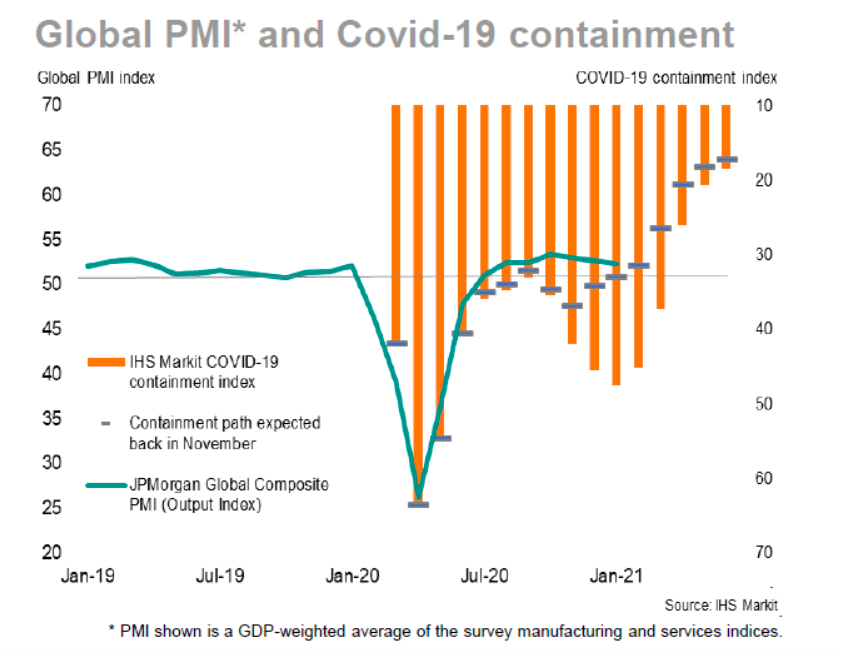

Although JPM Global PMI index has been slipping for three months, at 52.3 it still indicates solid growth.

Most interestingly as seen in the chart “the adverse impact on global GDP from the pandemic in recent months so far looks considerably less severe than seen during the first half of 2020“

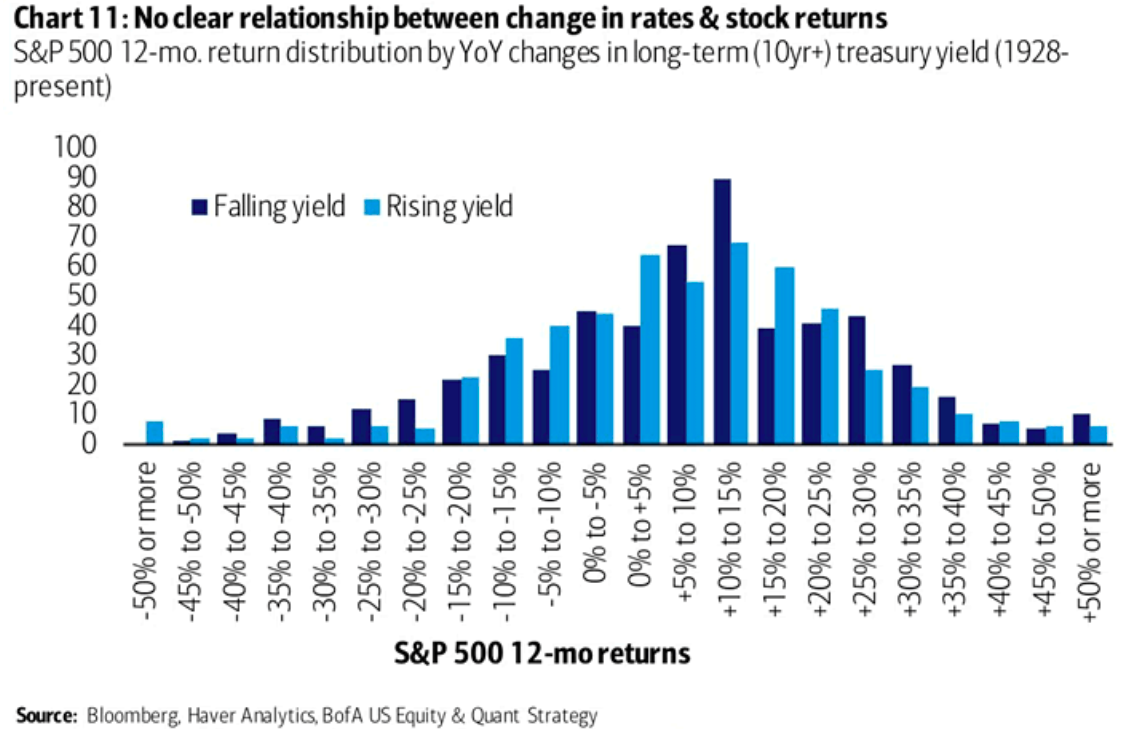

This chart suggests there is no clear relationship between changes in rates (captured by 10-year treasury yield) and S&P 12 month returns using data from 1928 – today.

Covid is having one huge positive impact if governments seize it.

In its results Roche said of diagnostics equipment – “we are installing in one year what we have installed the prior five years. So we are more than doubling our installed base out there of the systems.“

This huge increase in capacity, they go on to say, could be used to detect HPV (saving 300,000 women’s lives who die of cervical cancer every year), HepC (helping 80 million people who live with this disease), and Tuberculosis (“one-fifth of population has infection of the bacteria of tuberculosis worldwide”).

“We need to start to recognize what health care systems can do by intervening much earlier. And I have to say, there is such an opportunity and governments need to get going on this. I’m sorry to get a bit emotional on this, but I have been fighting for 10 years with governments to include HPV screening and all the clinical data is out there, and they need to get going, and not just you know let it go, like they have in the past.“

“…we do expect some significant cost inflation in the year…The top two inflation drivers for this year are expected to be pulp and polymer based materials. Together those two input costs represent more than half of the inflation outlook.” – Kimberly-Clark (KMB) CFO Maria Henry

“We expect prices to be positive based on all the inflation that we are seeing.” – 3M (MMM) CFO Monish Patolawala

“…the transportation market is very tight. Spot market rates have increased by more than 30%…And just a bit more color on commodities…we see headwinds on our major commodities right now. But not only on our major commodities, but some of the smaller purchases of raw and packing materials that we use across the rest of our business.” – Church & Dwight (CHD) EVP-Global Operations Rick Spann

“…we are starting to see a little bit of inflationary pressure, particularly around freight and a little bit in the supply chain as well.” – Danaher (DHR) CFO Matt McGrew