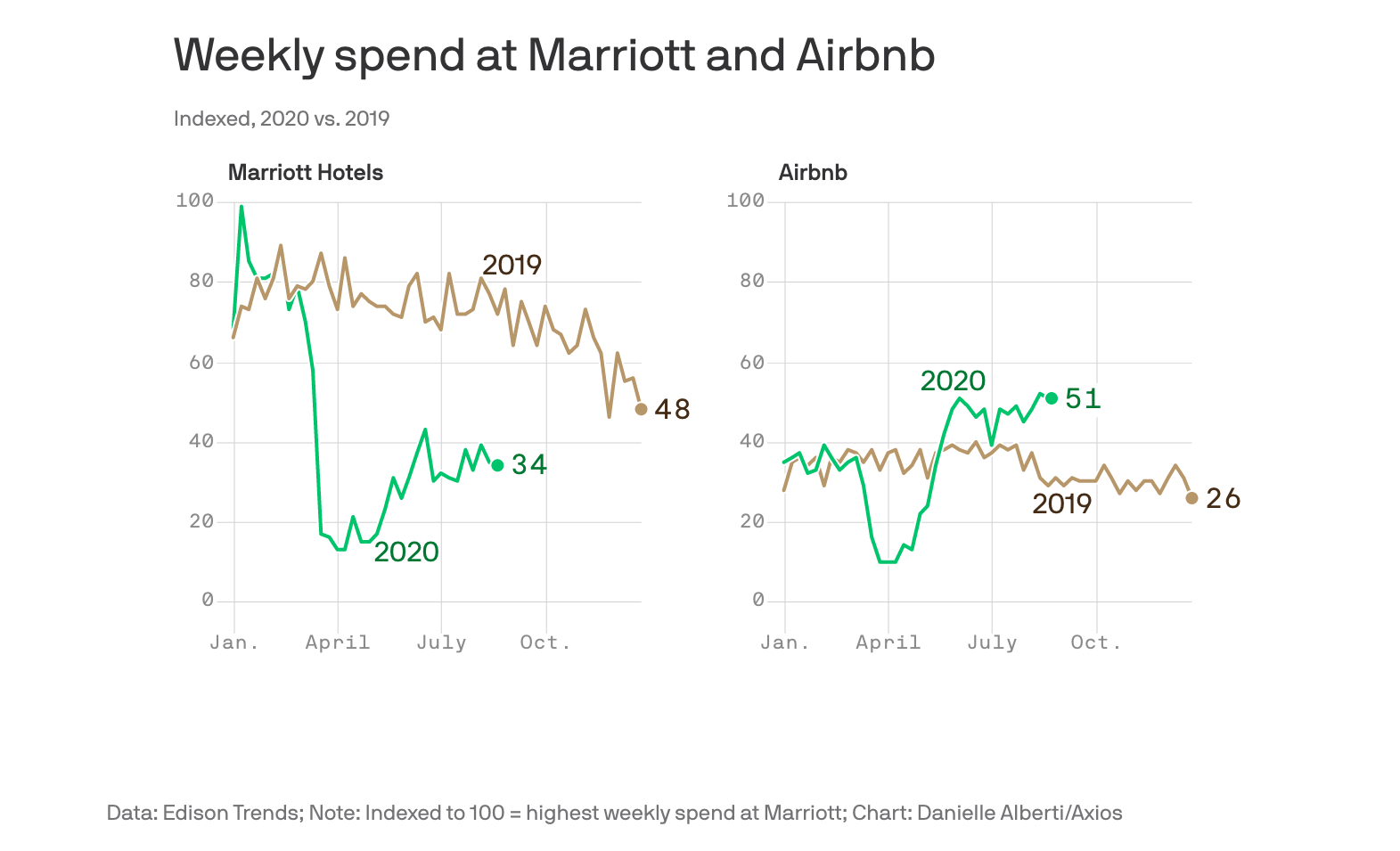

“Airbnb spending is running a whopping 75% higher than this time last year according to Edison Trends, based on a panel of spending data including more than 65,000 Airbnb transactions.“

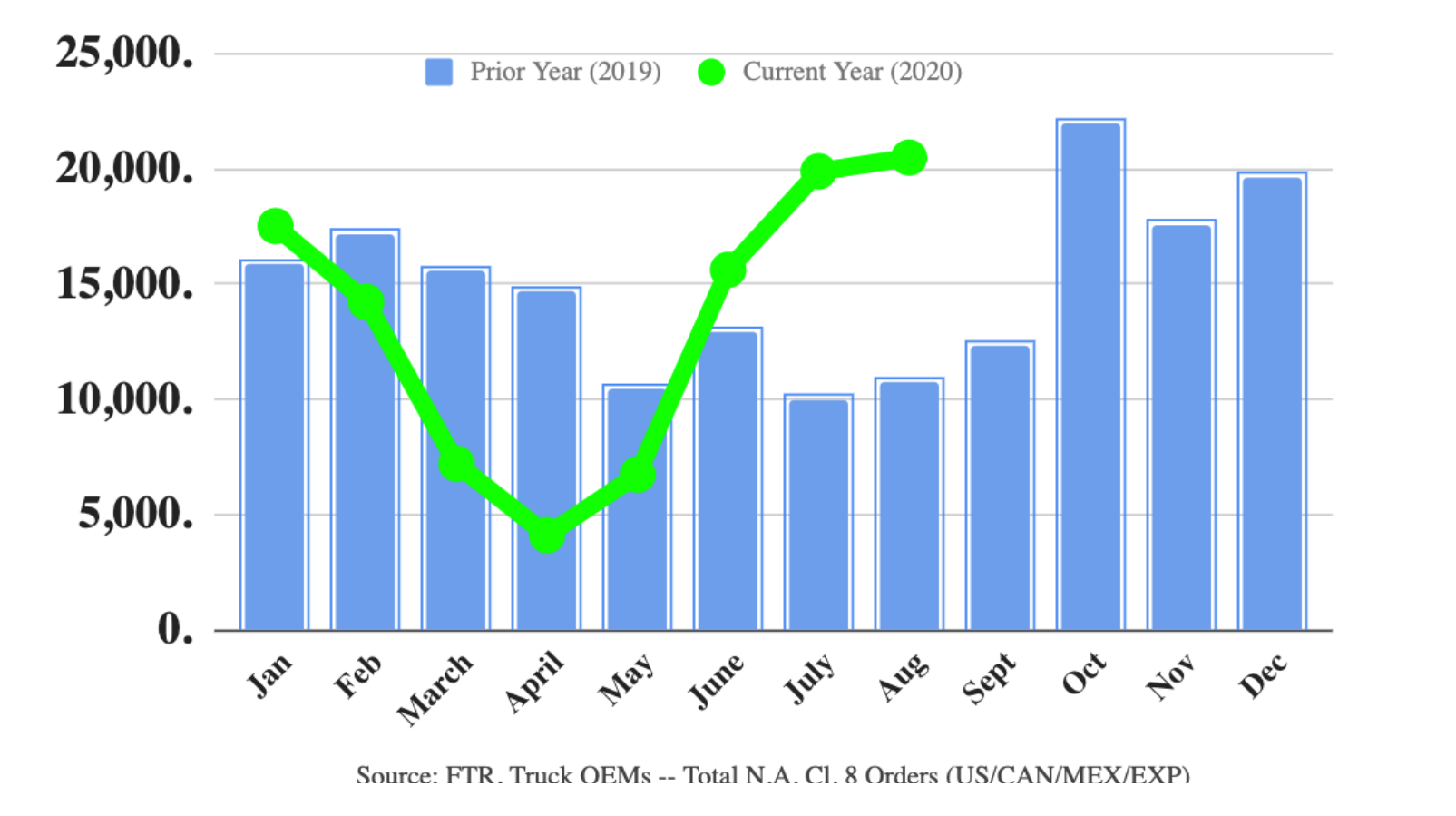

The very economically sensitive orders of heavy (Class 8) trucks in the US continue to be robust.

“This is an odd situation. We are in a highly uncertain, yet very stable, environment. You have a pandemic, a presidential campaign, and social unrest all occurring at the same time. However, the economy is briskly recovering and generating ample freight. Fleets are ordering only what they need, and thus, orders are aligning very closely to production rates.“

“It took nearly a century for the flush toilet to approach 80% household penetration. Electricity took 30 years to get to 80%; Refrigerators 20 years; cell phones 15 years; Social media 12 years.“

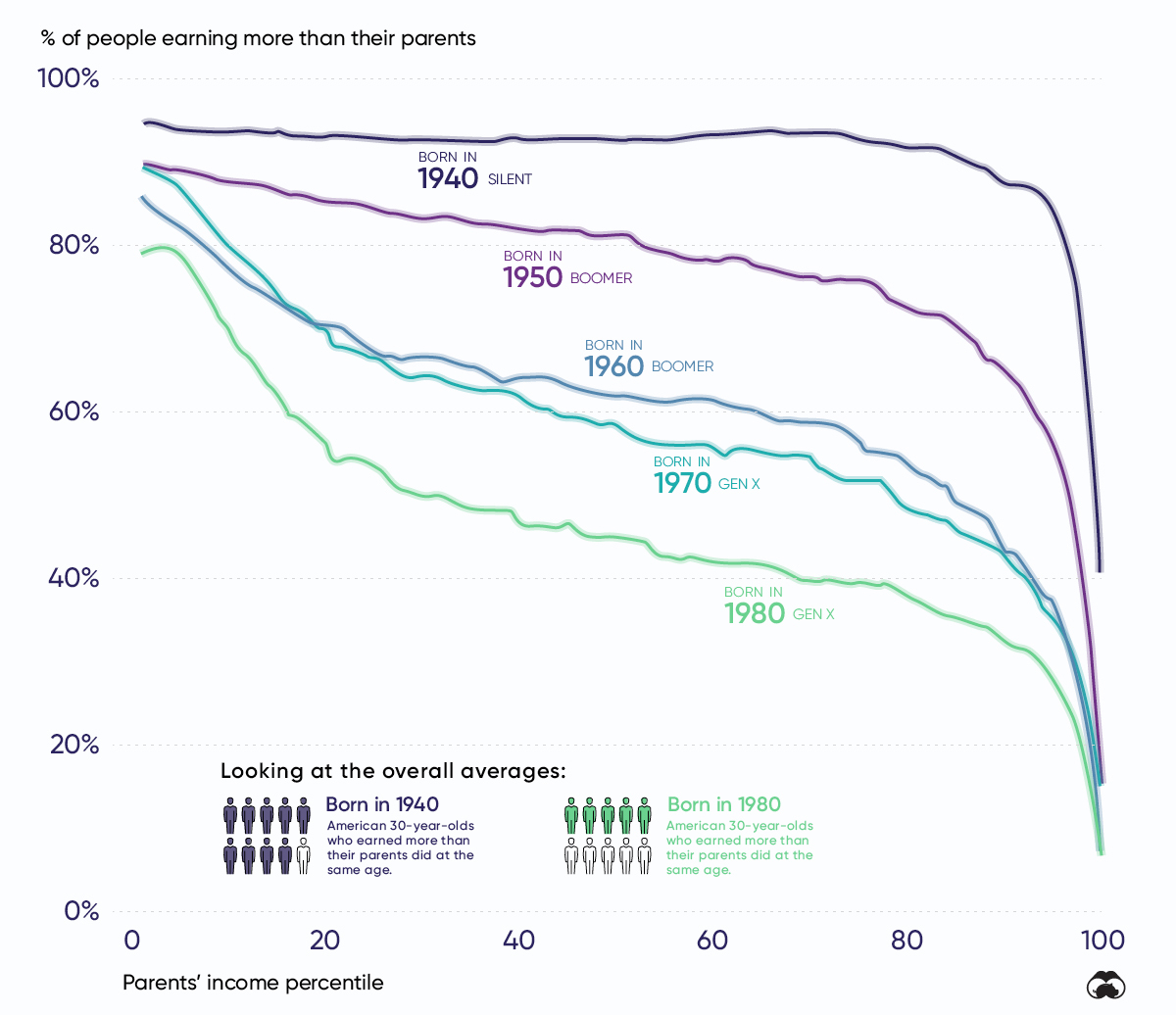

“This graphic plots the probability that a 30-year-old American has to out earn their parents (vertical axis) depending on their parent’s income percentile (horizontal axis). The 1st percentile represents America’s lowest earners, while the 99th percentile the richest.“

Take the 50th percentile (“middle class”) – the probability of someone out-earning their parents has fallen precipitously – it was 93% for people born in 1940 and dropped to 45% for those born in 1980.

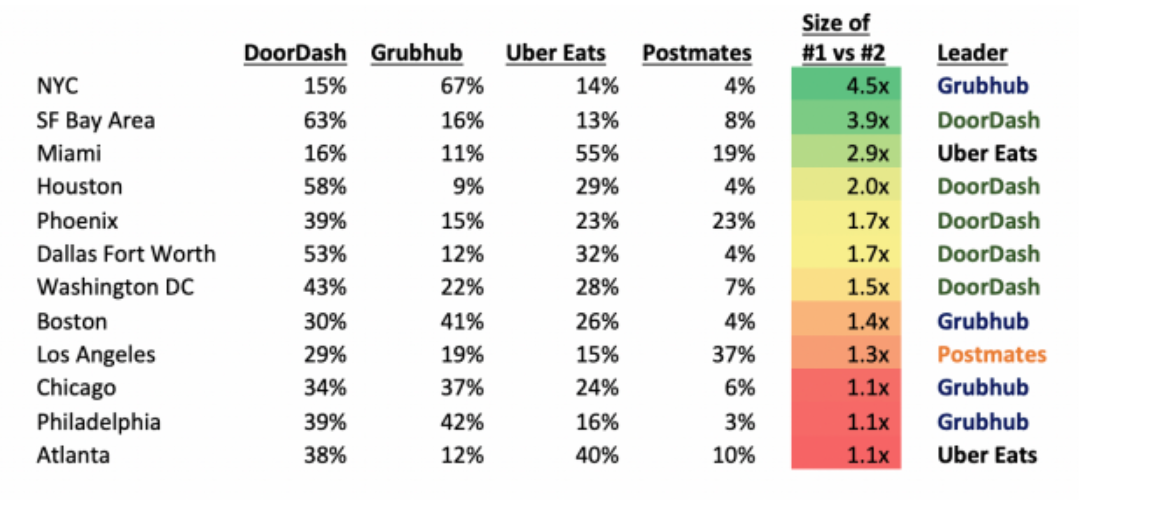

Brilliant article on the monopolistic power of food delivery businesses especially as they begin to vertically integrate and merge around the world.

“Losing money to acquire market power, or to steal from investors, is a form of counterfeiting, because it drives honest competitors that have to generate a profit out of the market“.

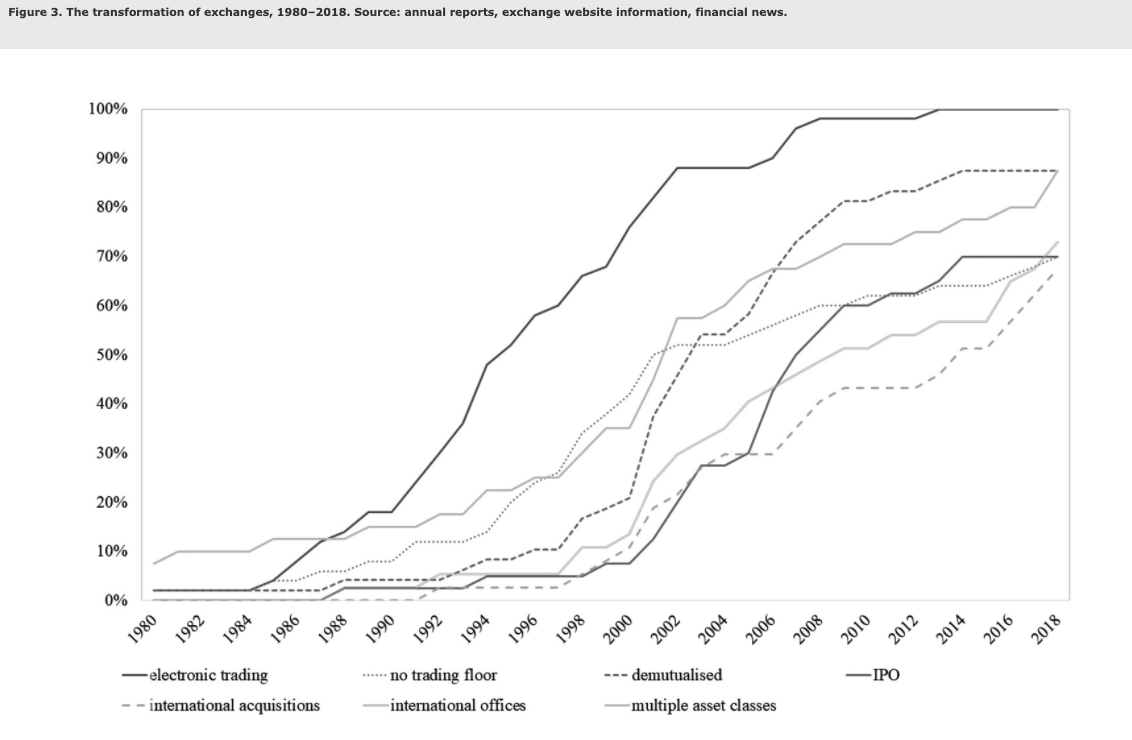

A great post about the history of Intercontinental Exchange and its founder Jeffery Sprecher. Its success was based on a few factors.

(1) “Sprecher gave away 80% of the company to his customers as an incentive for them to trade at his venue.”

(2) “the company had a lucky break when Enron went bust.”

(3) Lots of deals meant diversification especially into oil trading and clearing. 20 deals in the past 15 years. Three criteria drove these – enhance network, new content, turnarounds.

It also comes down to three insights – analogue to digital, using regulation as an opportunity and the power of data.