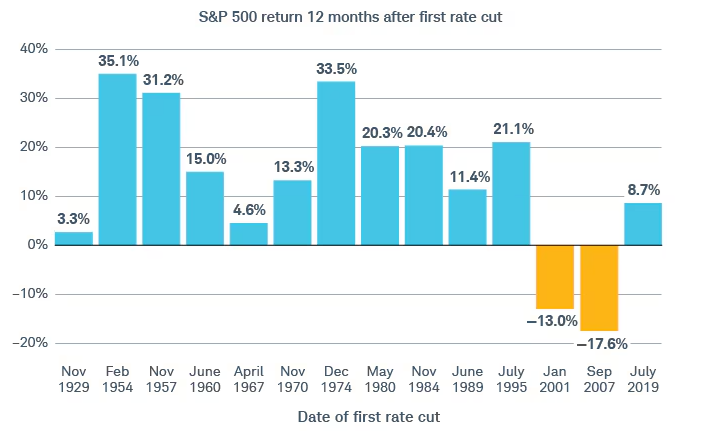

Finance is perhaps unique of all the industries that venture capital has set its sights on in one way – it has been around a very long time and therefore seen its fair share of disruption attempts.

Here is a list of fintech business models that the author thinks are bound to fail – some interesting lessons there.

In understanding Russia today, it helps to understand what World War II meant for the country.

“In the Soviet Union and later in Russia, reference to World War II played a central role in the decades after 1945. The reference has never lost any of its intensity and is currently reaching a new climax.“

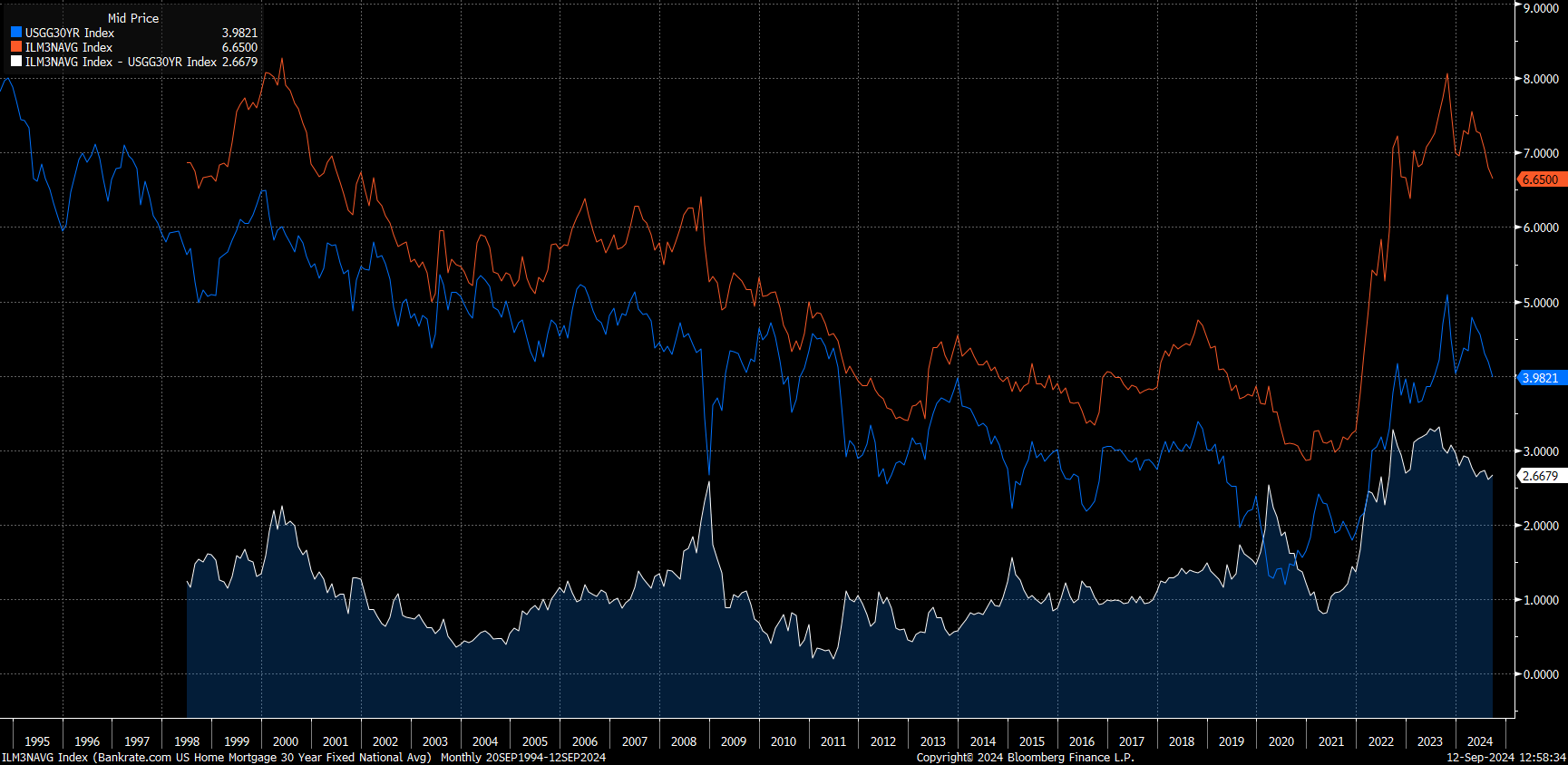

US 30-year fixed mortgage rates (orange line, bankrate data) are coming down, pushed by falling 30-year treasury rates (blue line).

Interestingly, the spread to 30-year US treasuries (white line) went up a lot this rate cycle and remains (2.67%) well above the historic average (1.3%). Normalisation here could be a big boost.

Market structures are changing all the time and even staunch fundamental investors need to pay attention.

The list is long right now – passive, pod shops, short volatility, options trading boom.

This is a good read on the rise of WallStreetBets (founded in 2011) and the culture of the millions of retail traders that have joined the market during and after the pandemic.

It is interesting in that it highlights how authorities (DOJ, FTC) are looking at new ways companies price fix – here via OPIS a PVC industry newsletter.

FTC is looking hard at intermediaries (e.g. trade associations) as a means for company price coordination.

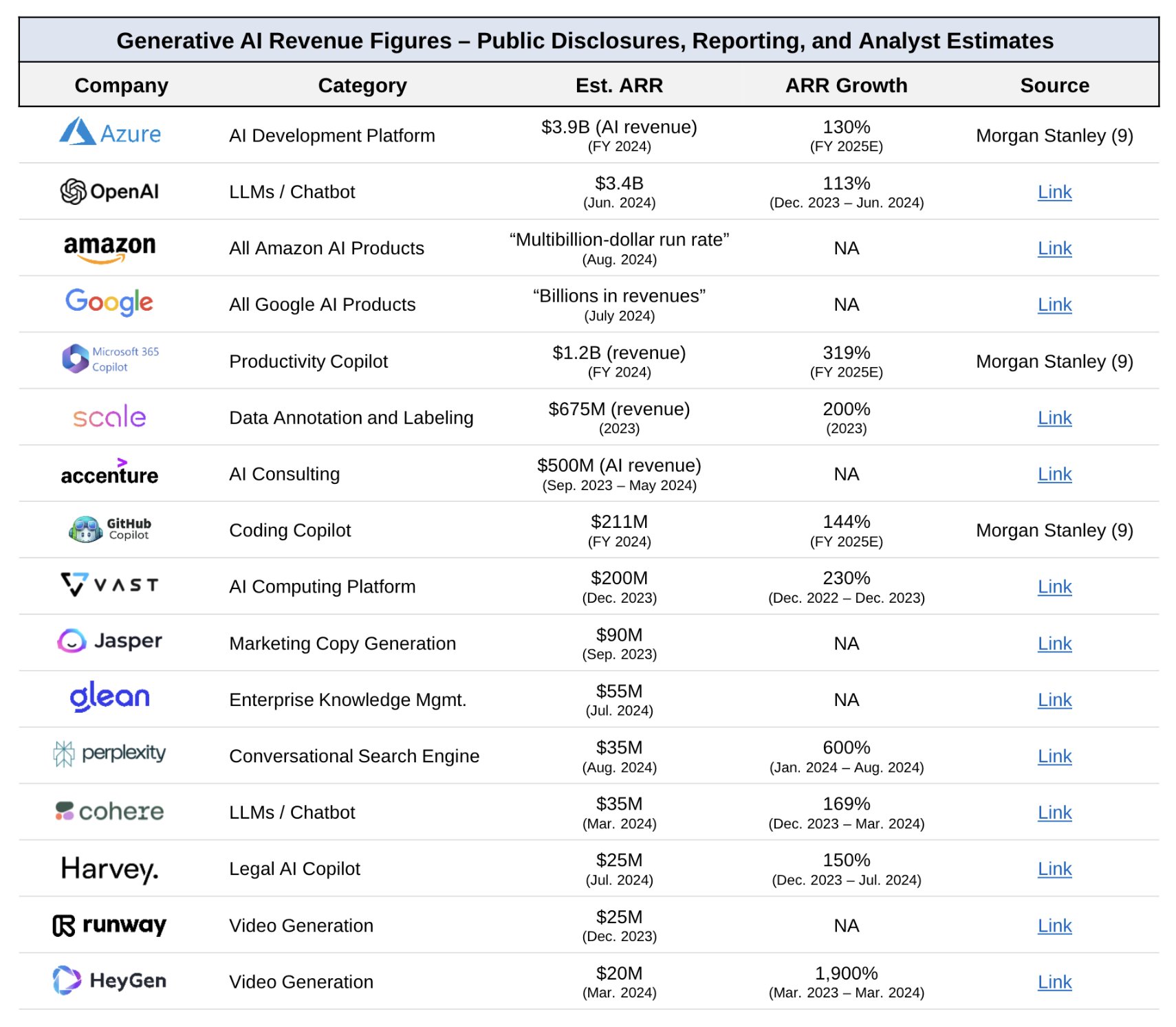

Interesting paper on the rise of the now $1.5 trillion private credit market.

“In equity, the two great trends have been the shift from public markets to private ownership and the consolidation of American companies’ stock in the hands of powerful investment funds. In debt, by contrast, the great trends have been a shift from private loans to quasi-public markets, democratization and dispersed ownership. In this Article, we chronicle the recent and dramatic reversal of these trends in the debt markets. Private investment funds executing a “private credit” strategy have become increasingly important corporate lenders, bringing into corporate debt the same forces of de-democratization and consolidation that have been reshaping the equity markets.“

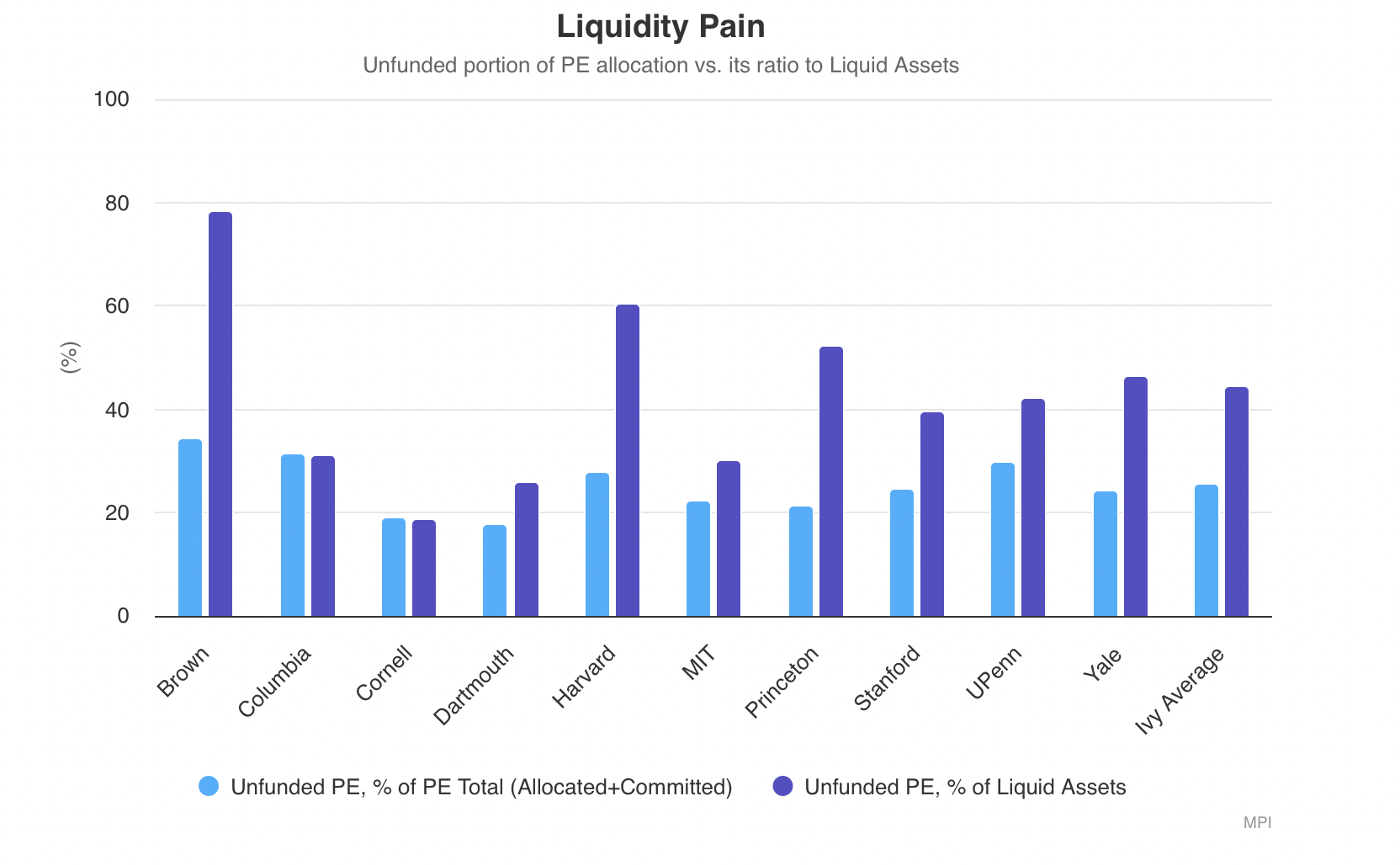

Are rising sharply according to Carta (just one data source).

This is hurting VC funds of certain vintages “Only 9 per cent of venture funds raised in 2021 have returned any capital to their ultimate investors, according to Carta. By comparison, a quarter of 2017 funds had returned capital by the same stage.“

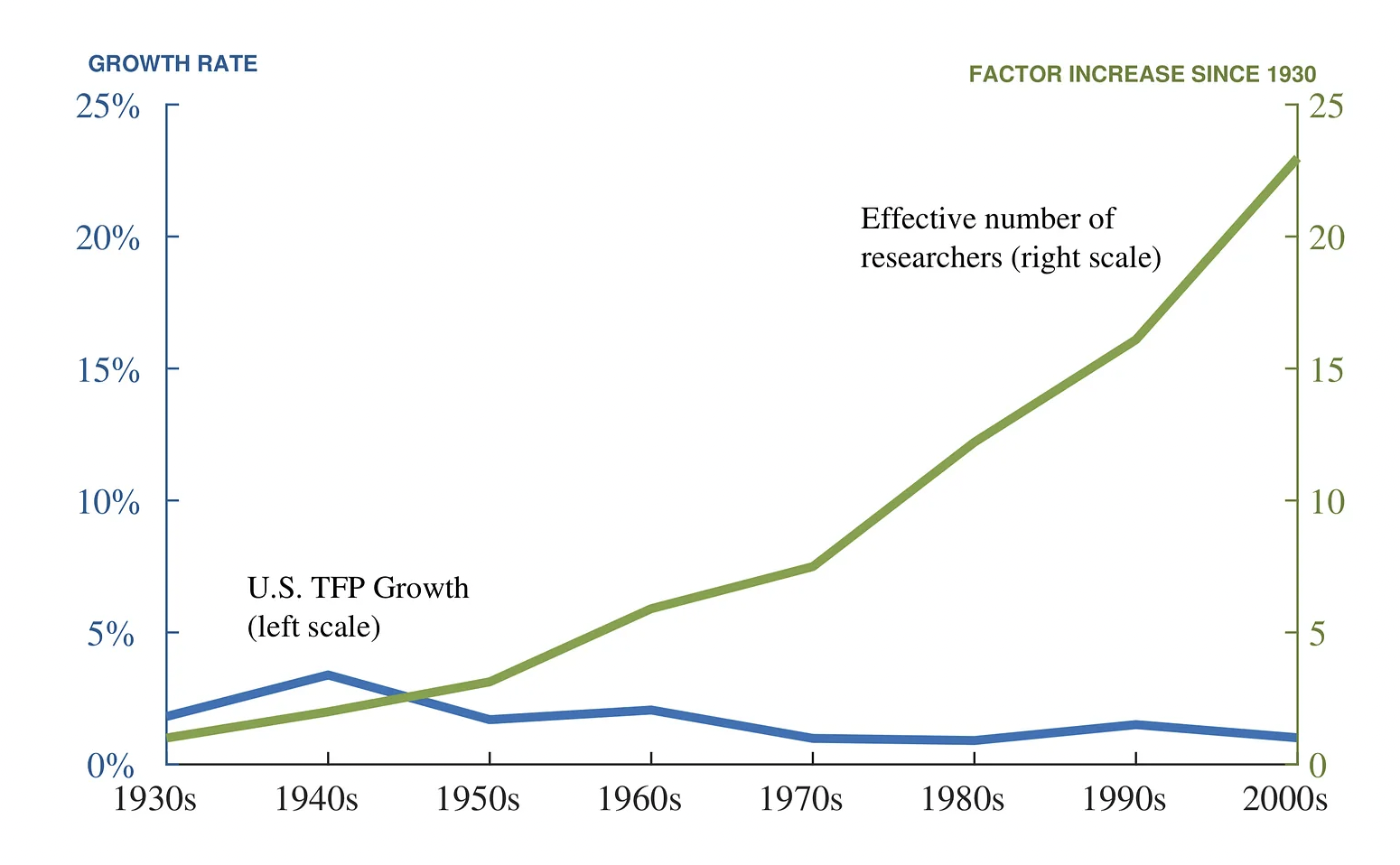

This blog post argues that tech monopolies are good, short lived, and ultimately “fund” the next disruptor.

Within it is an interesting concept of Slack – “Some group of people must exist who are educated, aware, motivated, and at the bleeding edge of a field…who nonetheless have some spare hours in the workweek to spend innovating on something instead of slavishly executing a task.“

“It’s necessary to be slightly underemployed if you are to do something significant.“

Fascinating paper on credit markets going dark i.e. the rise of private credit – “We offer new data that illustrates the meteoric rise of the now $1.5 trillion private credit industry and explore the allure and implications of private credit.“

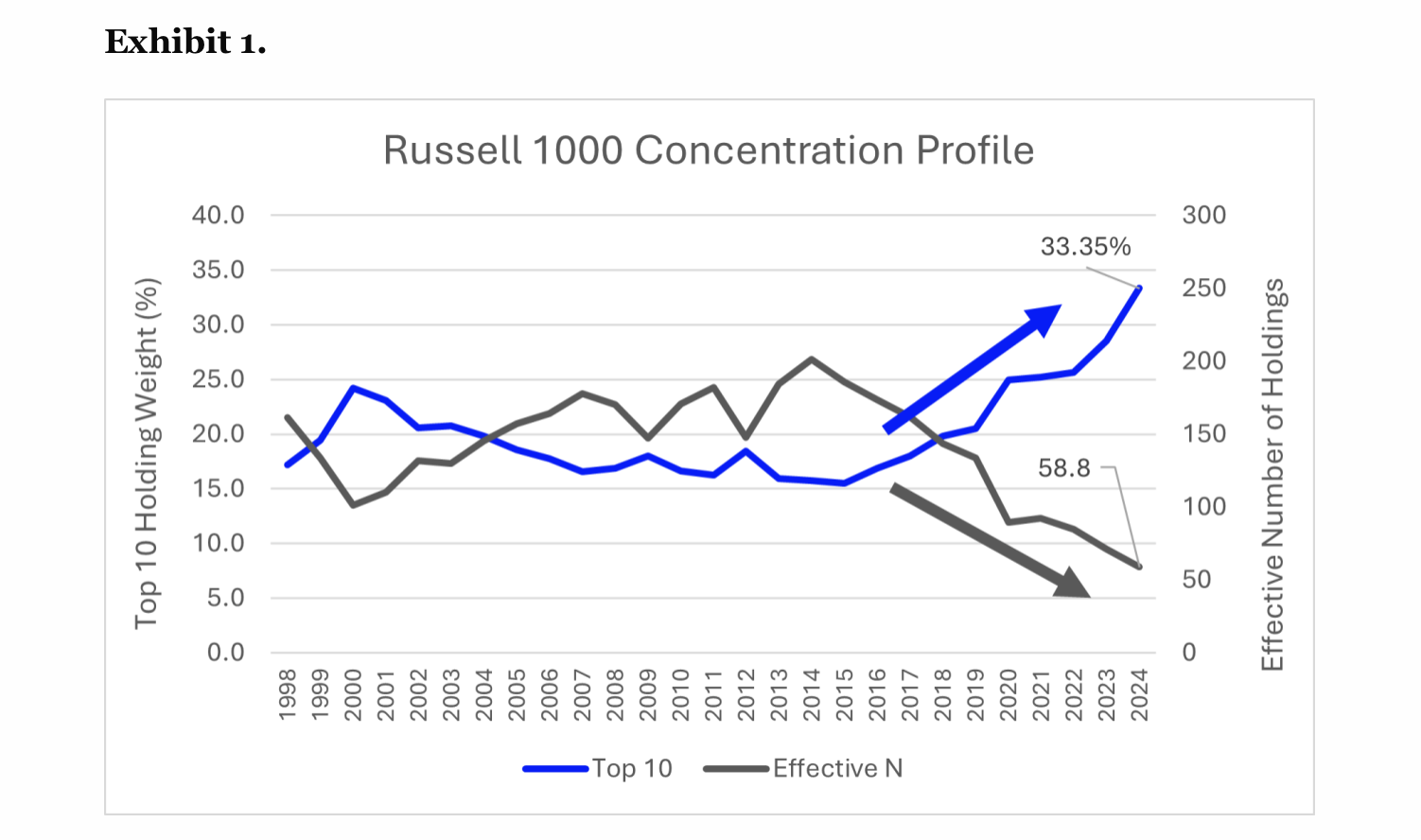

We all know indices are concentrated right now, more than ever. Just how bad is it?

“The startling conclusion is that, despite the Russell 1000 nominally providing exposure to its namesake number of stocks, the index affords an effective diversification of only 59 stocks.“

“Not only does market-cap weighting induce substantial single-stock risk, but the diversification provided by this foundational asset class has evaporated by 70% over the past decade.“

Equal weight, as the article argues, is not the solution here, as it “suffers from significant operational costs, underperformance, questionable assumptions, and skewed risk bets.“