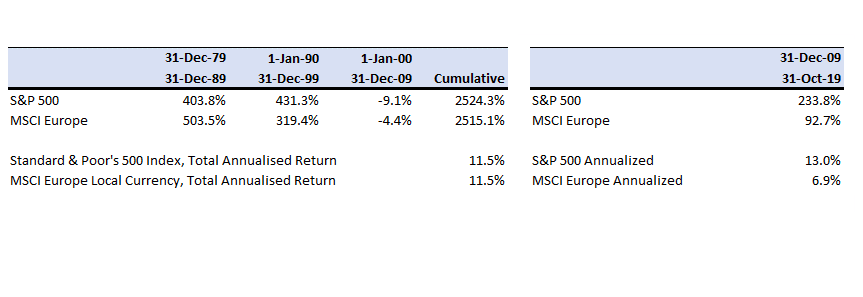

“Just over 20 years have passed since the publication of Mark Carhart’s landmark 1997 study on mutual funds.

Its conclusion—that the data did “not support the existence of skilled or informed mutual fund portfolio managers”—was the capstone of an academic literature, which began with Michael Jensen in 1968, that formed the conventional wisdom that active management does not create value for investors.

We review the literature on active mutual fund management since the publication of Carhart’s work to assess the extent to which current research still supports the conventional wisdom.

Our review of the most recent literature suggests that the conventional wisdom is too negative on the value of active management.“

An interesting and novel conference organised by the Fed on Climate Change Economics. Live stream available.

“It’s important for us from a monetary policy perspective to know what the potential growth rate of the economy is and if climate events or climate risk is going to shave that off, even if it’s over the long term,” San Fran Fed chief Mary Daly said earlier this week.

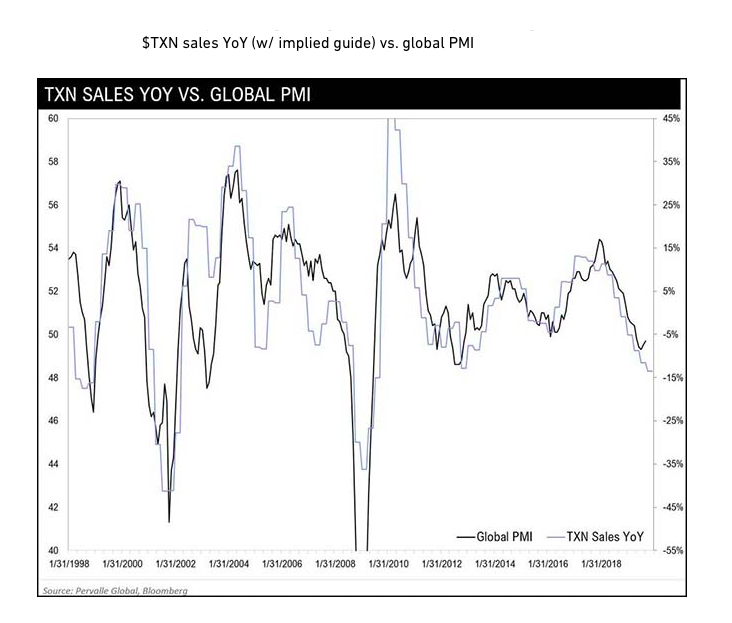

“Revenue decreased 11% from a year ago and came in below the midpoint of our guidance as we saw most end markets continue to weaken further … the weakness we’ve seen in the third quarter was broad-based across all markets and most sectors … We saw weakness across all major customers, regions and technologies … our sense is that customers are just far more cautiousthan they were certainly a year ago, but even 90 days ago.”

A fascinating piece from a16z, the US venture capital firm, on biology.

They run a $650m Bio fund and invest in many new technologies.

“Bio today is where information technology was 50 years ago: on the precipice of touching all of our lives. Just like software—and because of it—biology will one day become part of every industry.”

Lots of links within to articles (written by a16z) on various aspects of how healthcare is transforming.

This piece is a shout out to the now famous 2011 article by a16z “Why Software is Eating the World”.

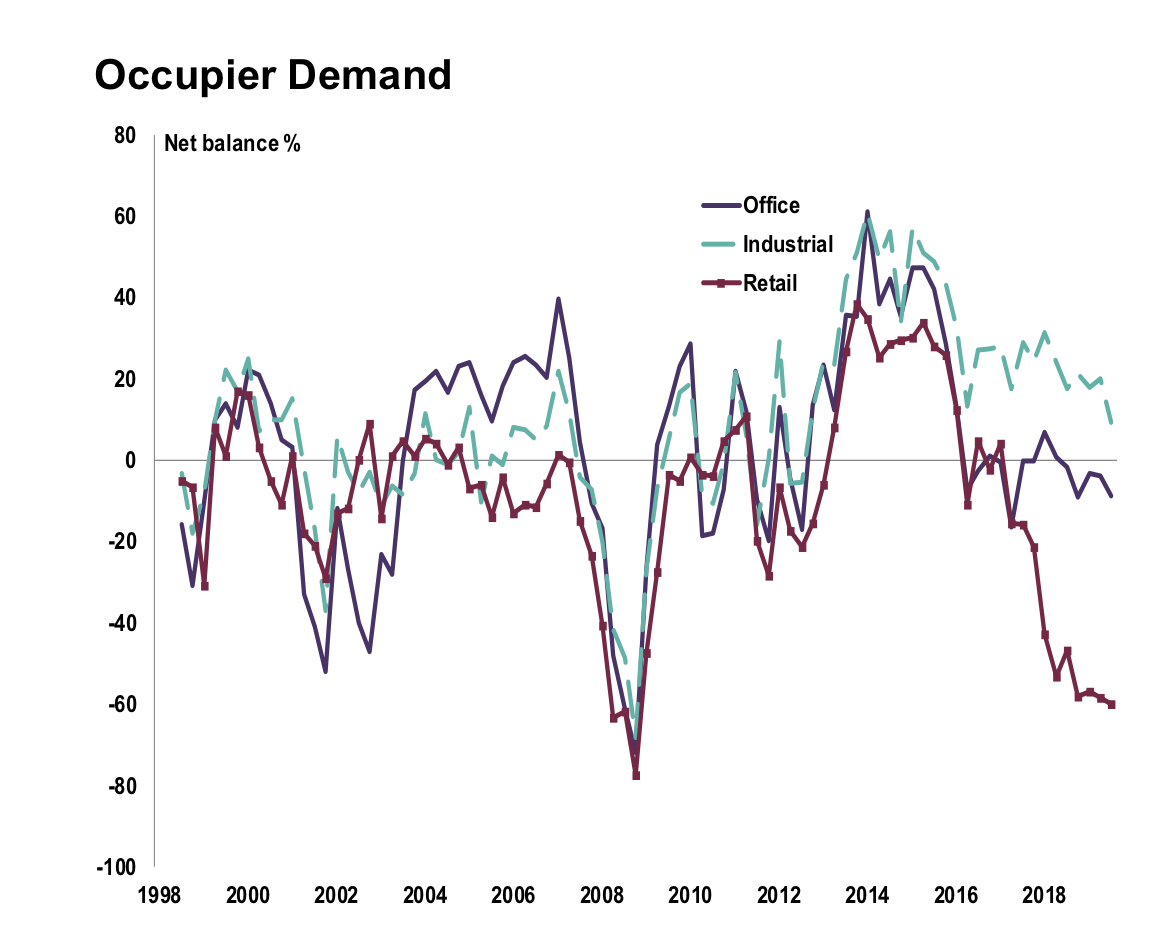

Royal Institution of Chartered Surveyors (RICS) Q3 survey of UK commercial property is out this week.

“The Q3 Survey results point to a deterioration in sentiment over the period, with 62% of respondents now sensing the market is in the downturn phase of the property cycle.“

Grub Investor Letter after their recent profit warning (and -43% fall in the shares) is worth a read.

We have previously pointed out how alternative data was suggesting competitors were beating Grub.

The letter points out how the online takeout market is getting a lot more competitive.

“Furthermore, we believe online diners are becoming more promiscuous … our newer diners are increasingly coming to us already having ordered on a competing online platform, and our existing diners are increasingly ordering from multiple platforms … the easy wins in the market are disappearing a little more quickly than we thought.”