“In over 3.8 million miles driven without a human being behind the steering wheel in rider-only mode, the Waymo Driver (Waymo’s fully autonomous driving technology) incurred zero bodily injury claims in comparison with the human driver baseline of 1.11 claims per million miles. The Waymo Driver also significantly reduced property damage claims to 0.78 claims per million miles in comparison with the human driver baseline of 3.26 claims per million miles.“

The annual list is always full of interesting facts.

“The US Defence Department earns $100m/year operating slot machines used by soldiers on their bases.“

“In the 19th Century, champagne was sweetened depending on local tastes. Russians had 300 grams of sugar added, the British just 50 grams. In 1842 Perrier-Jouët introduced unsweetened champagne. It failed and people called it ‘Brut’, but that’s how all champagne tastes today.“

“In 2004, it took one year to install 1 gigaWatt of solar power. In 2023, installed 1 gigaWatt of solar power every day.“

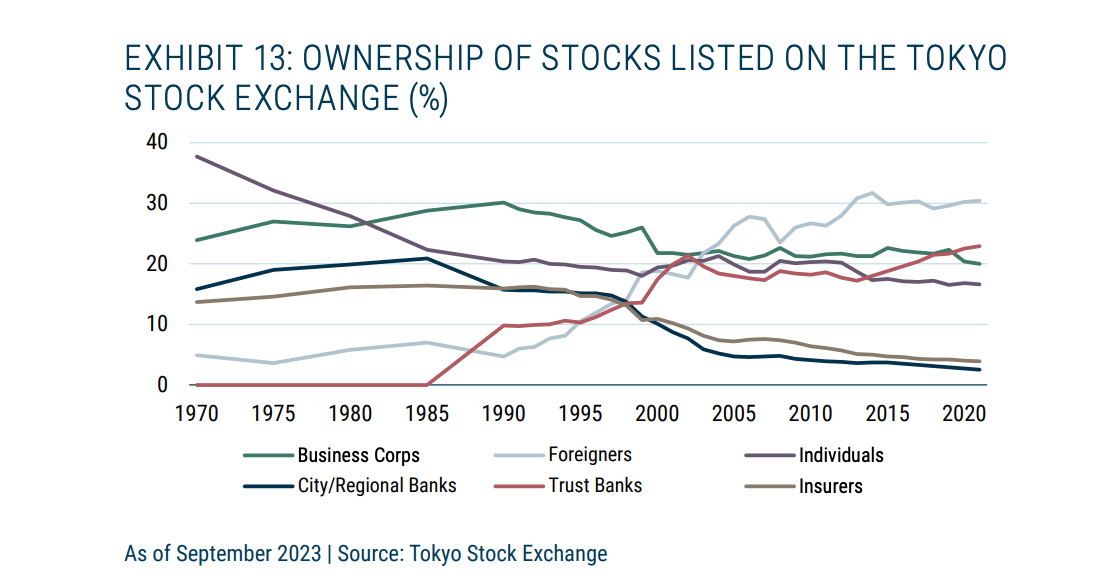

If you split it up into insiders (financial/corporate) and outsiders (everyone else), the former ownership peaked at 70% during the bubble years and has come down to 20%.

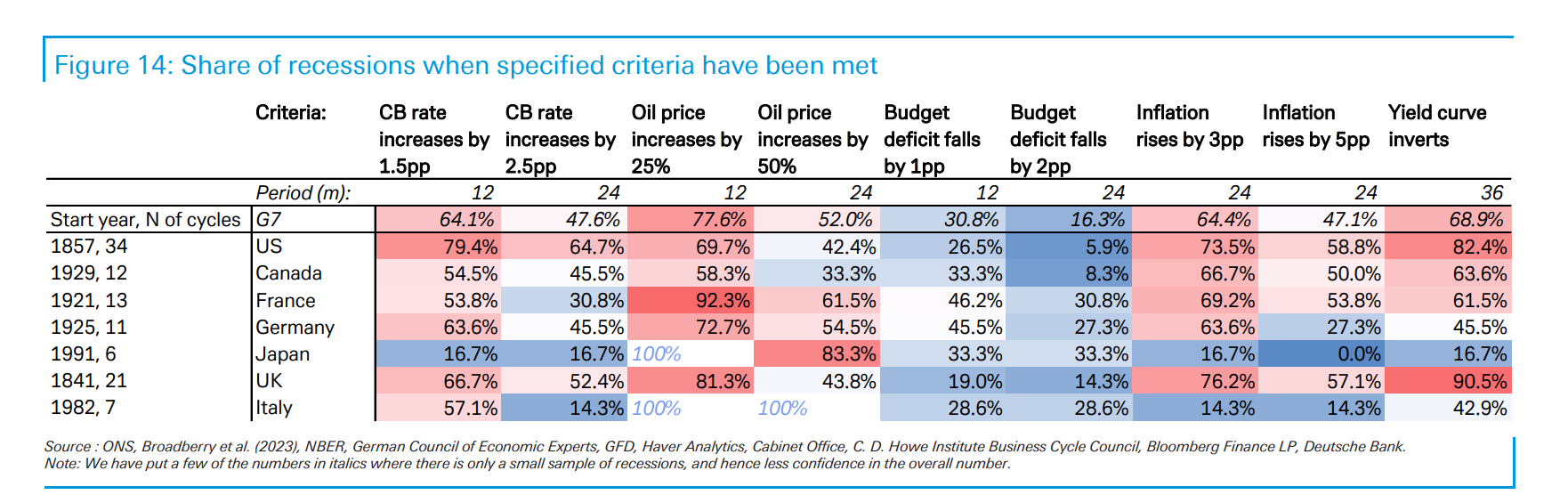

“79% of US recessions over the last 170 years have seen the central bank policy rate rise at least 1.5pp over a rolling 12-month period within 3 years prior to a recession. It’s 65% if you use 2.5pp of hikes over a rolling 24-month period. So most US recessions are preceded by tighter monetary policy“.

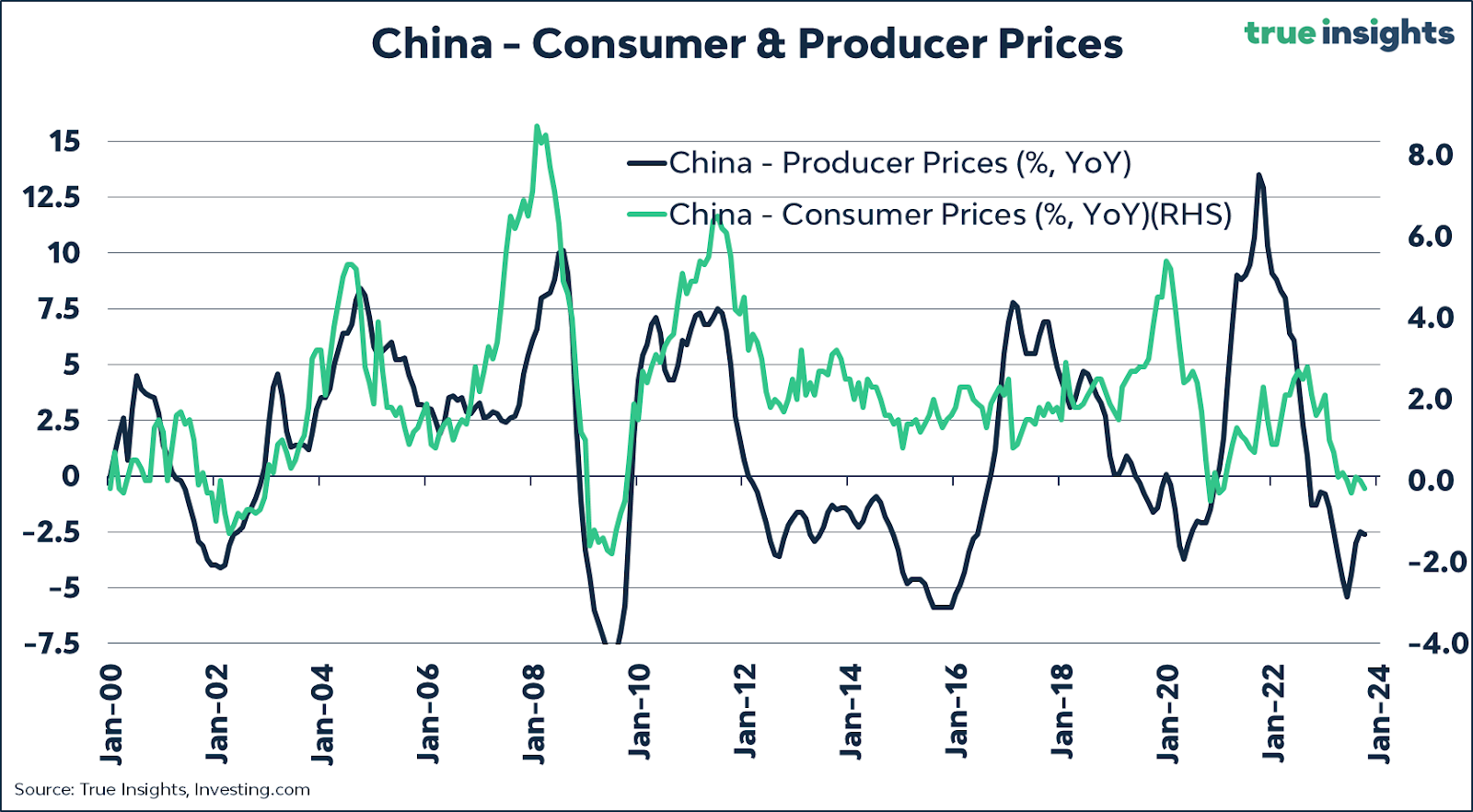

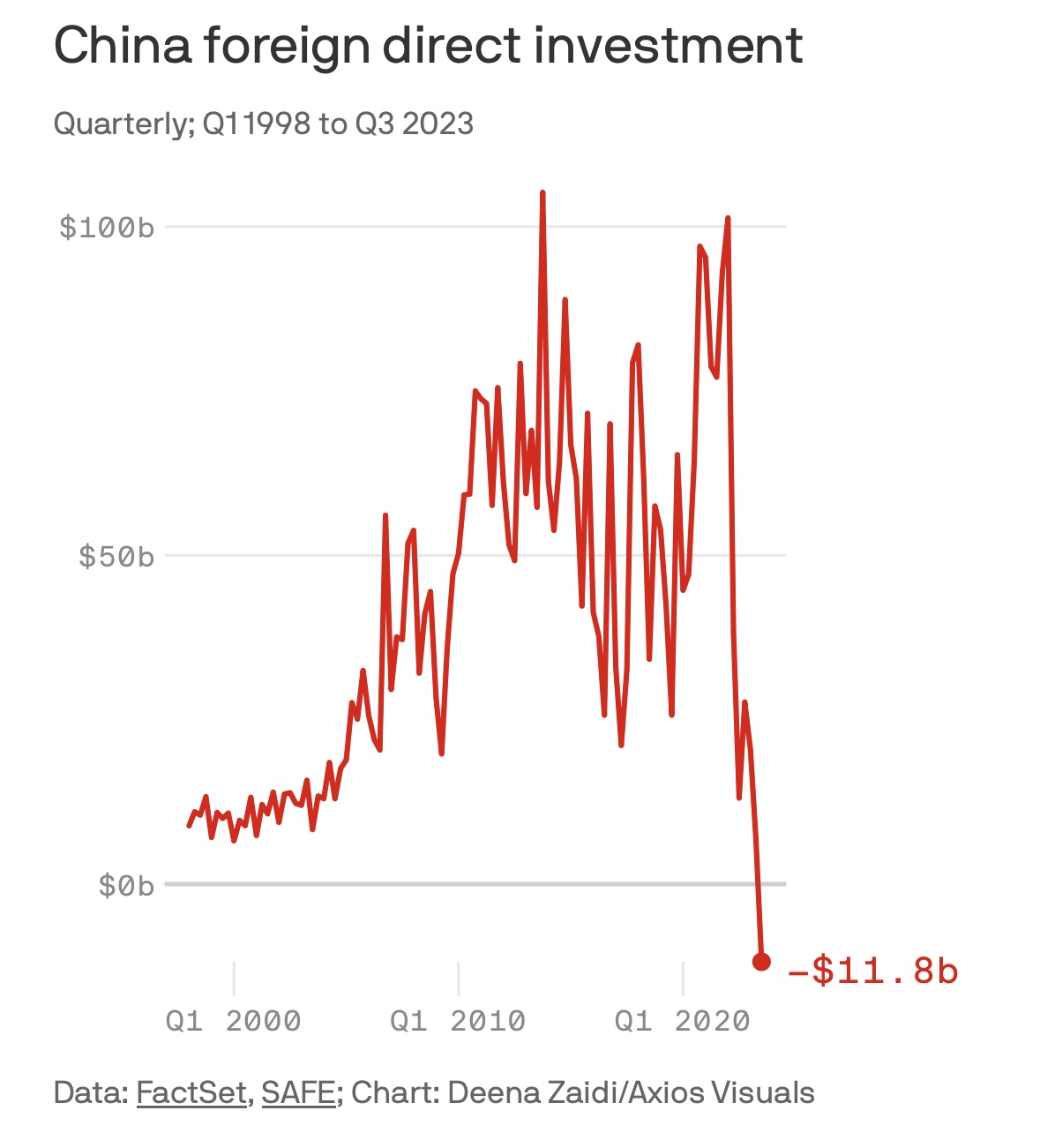

Has gone negative for the first time in many decades.

Some have pointed out that this is due to retained earnings repatriation out of China and not true investment, but the concern still remains longer term.

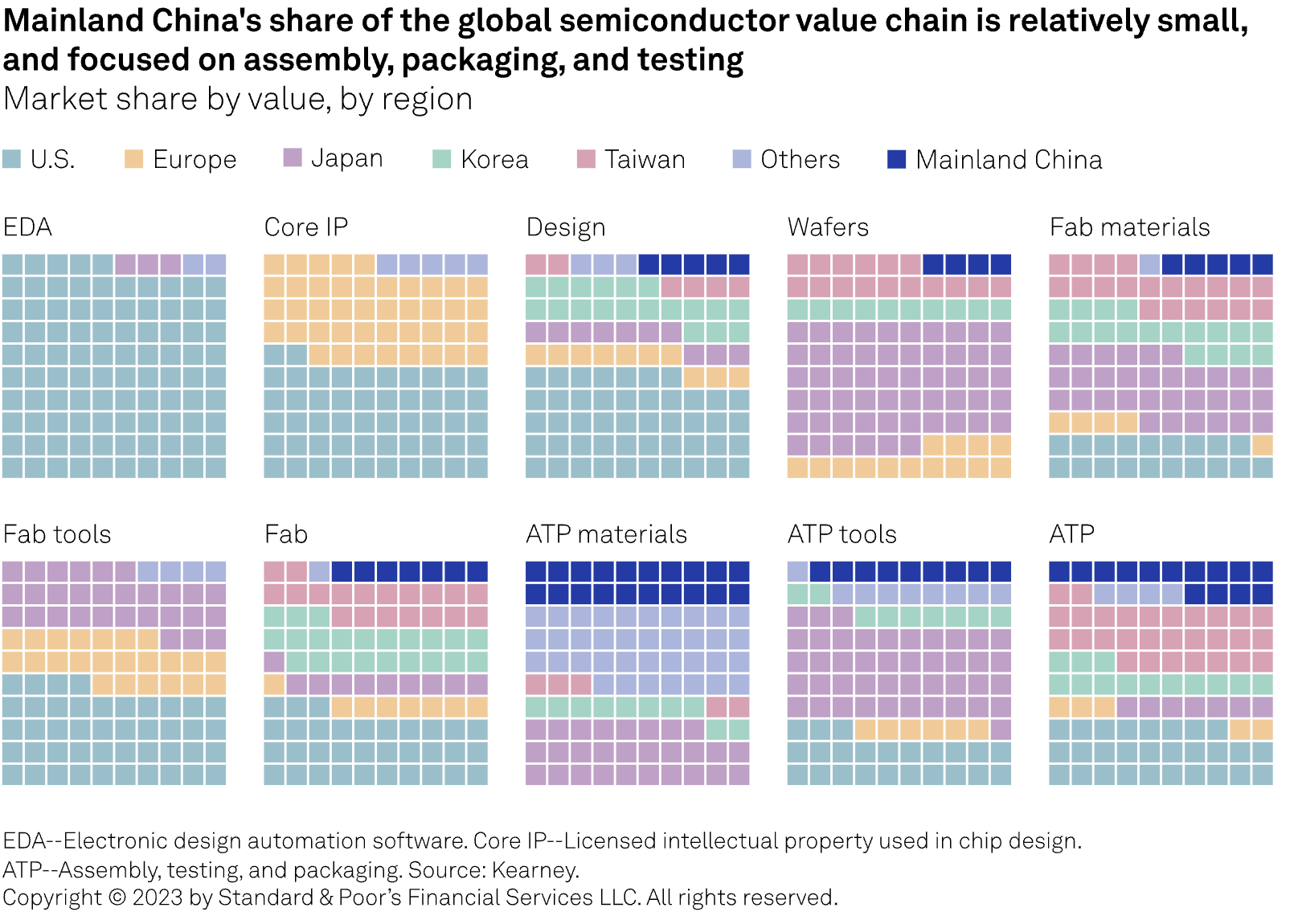

This chart is paired nicely with a very interesting article from the New Yorker – “China’s Age of Malaise”.

Some fantastic anecdotes “a leak from a Chinese social-media site last year revealed that it blocks no fewer than five hundred and sixty-four nicknames for him, including Caesar, the Last Emperor, and twenty-one variations of Winnie-the-Pooh.”

The trucking industry is undergoing another downcycle.

In a classic capital cycle, weakening demand has met over-expanded supply.

Bankruptcies have abounded from established trucking firms like Yellow (30,000 employees 100-year-old trucking firm)

to start-ups that tried to disrupt the less asset-intensive freight brokerage market such as Convoy (once valued at $3.8bn), where it looks like financing (both VC or otherwise) has met cold reality.

“For a firm that eats, sleeps, and breathes discounted CEFs, this is the most compelling entry point we’ve seen in 15+ years,” Matisse’s Nik Torkelson, whose firm invests in and researches closed-end funds, wrote in a note.

Interesting opportunities in closed-end funds as discounts have blown out. This is the case in the UK as well which has a large investment trust industry.

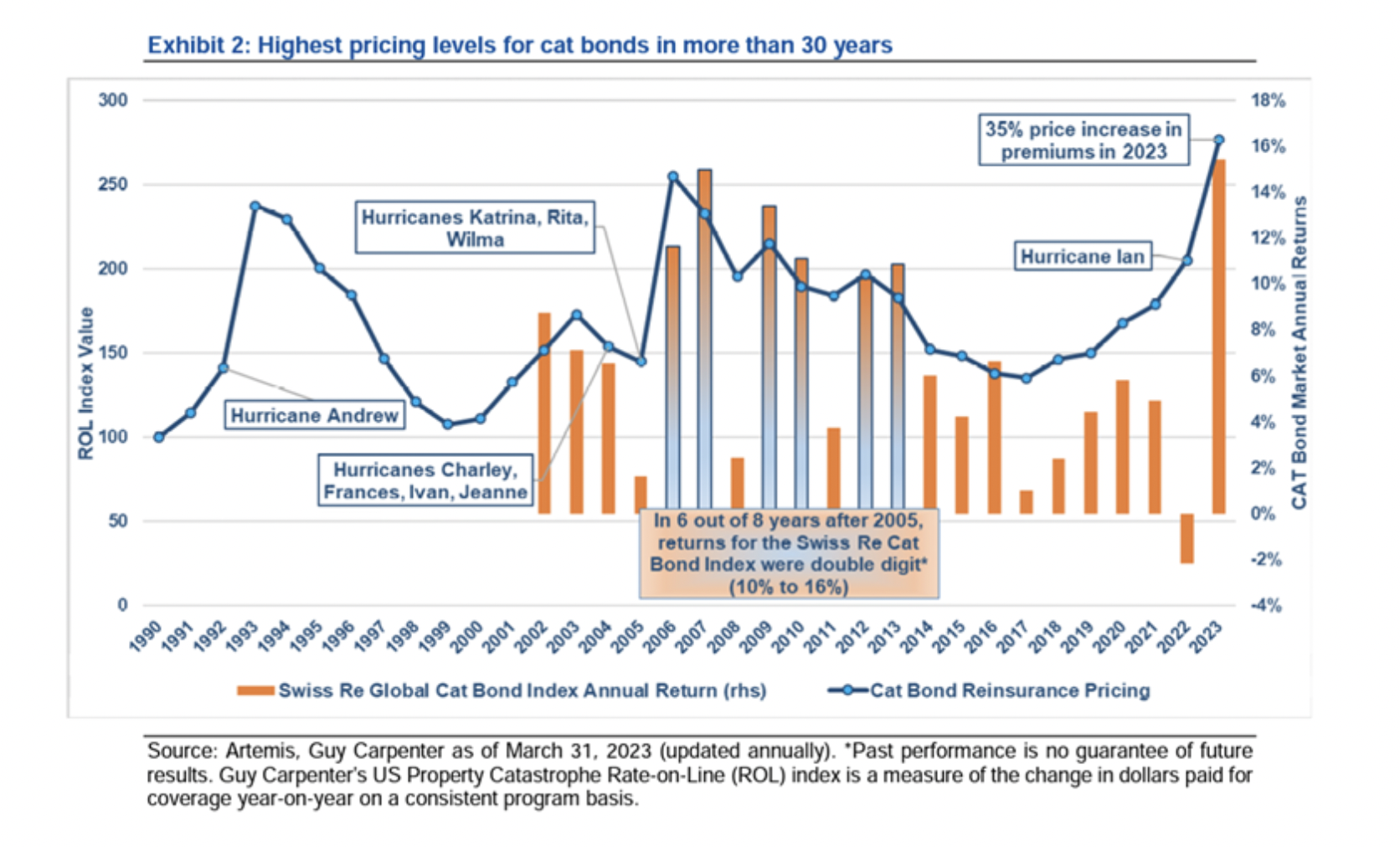

Pricing levels of Catastrophe Bonds (explained here) have hit a 30-year high.

“According to estimates by Guy Carpenter, a global risk specialist and provider of ILS sourcing and pricing information, the premium, or rate on line, of cat bonds increased by an annual rate of approximately 30% in January 2023, only the third time in three decades prices have reached such a level.”