Disney is planning to charge $35 for its standalone ESPN service.

As a result, The Information now calculates that after all the prices rises for streaming a permutation of the main “channels” starts to cost $90 per month … the price of Comcast’s cable package.

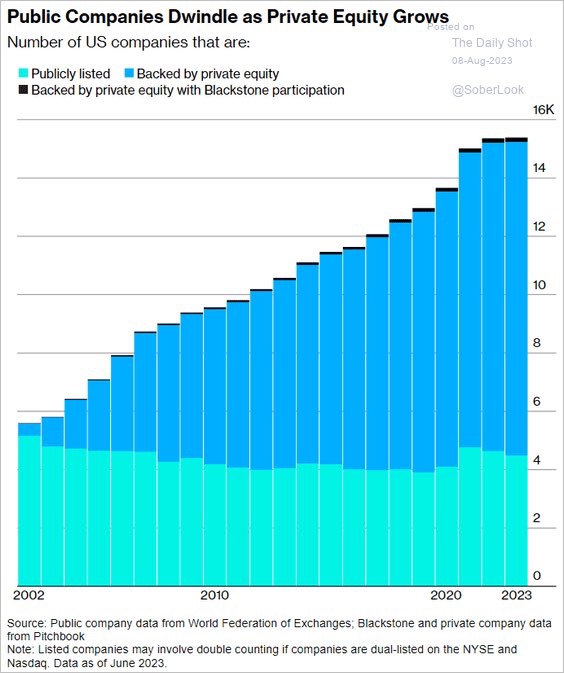

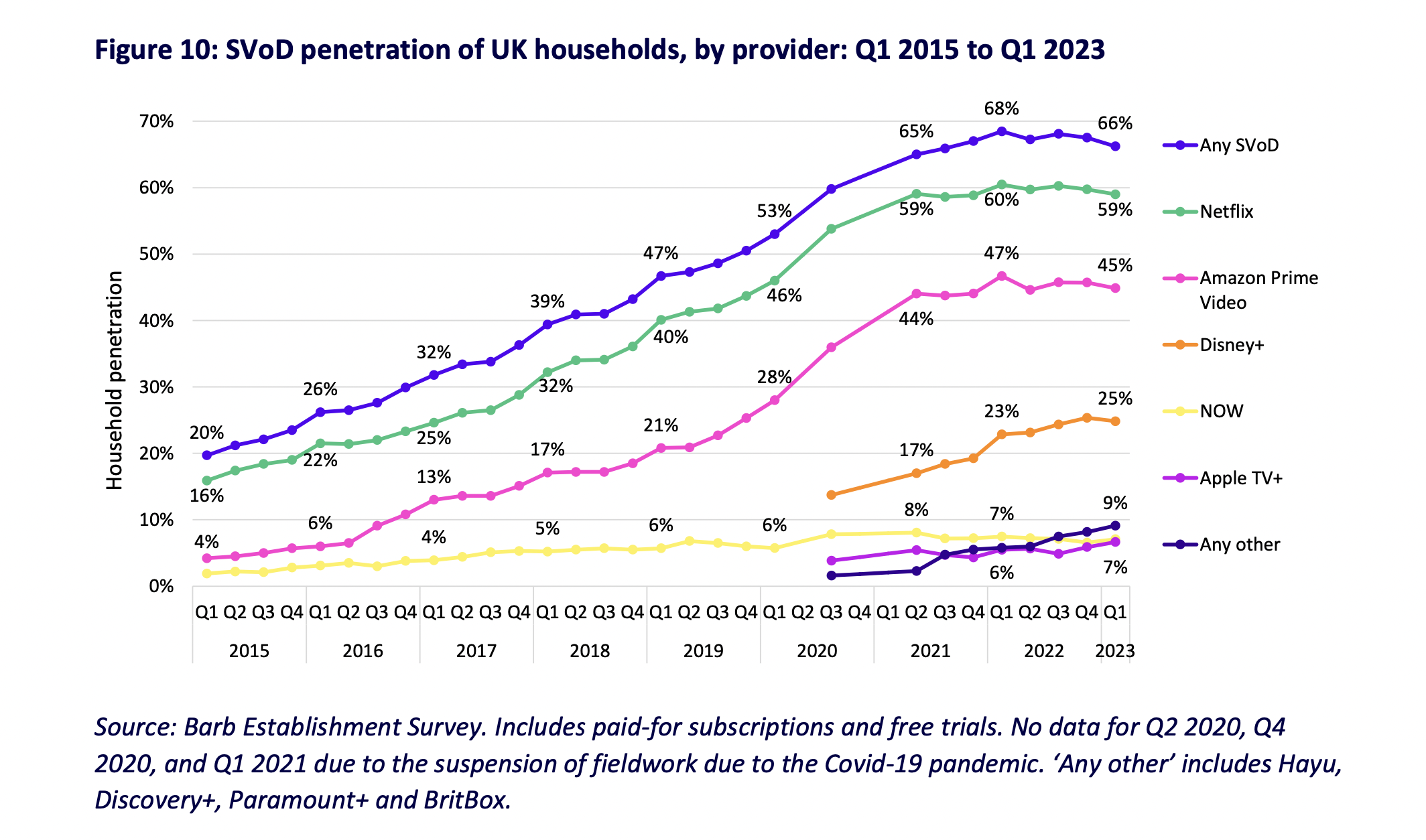

Data for the UK suggests we have hit saturation point.

“The growth of SVoD household penetration slowed in 2022, and this continued into early 2023 as the rising cost of living, combined with SVoD service price rises, put greater strain on household budgets.“

Interesting conversation (need sign up, grab two-week trial here) with Ted Seides and Frederik Gieschen on going back as far as Ancient Rome, on how institutional investing evolved and progressed, with lessons for the future.

What if drug development could one day be like engineering?

Artificial intelligence has the potential to make this a reality, as is so well explored in this accessible Forbes profile.

One of the most exciting parts they highlight is de novo protein design i.e. building proteins from nothing (this is a nice post about it from Derek Lowe).

Three excellent questions about the future of semiconductors and AI.

“First, is AI additive to the semis market? Will purchases of AI chips increase overall demand for semis, or will they merely replace purchases of other chips?

How will the market for AI Inference semis play out? How big will it be and who will win share?

Can Nvidia be displaced from the market dominance it currently enjoys?“

“There seems to be an unwritten rule on Wall Street: If you don’t understand it, then put your life savings into it.” Lynch.

“If you’re not willing to react with equanimity to a market price decline of 50% two or three times a century, you’re not fit to be a common shareholder and you deserve the mediocre result you’re going to get.” Munger.

“When you want to test the depths of the stream, don’t use both feet.” Chinese proverb.

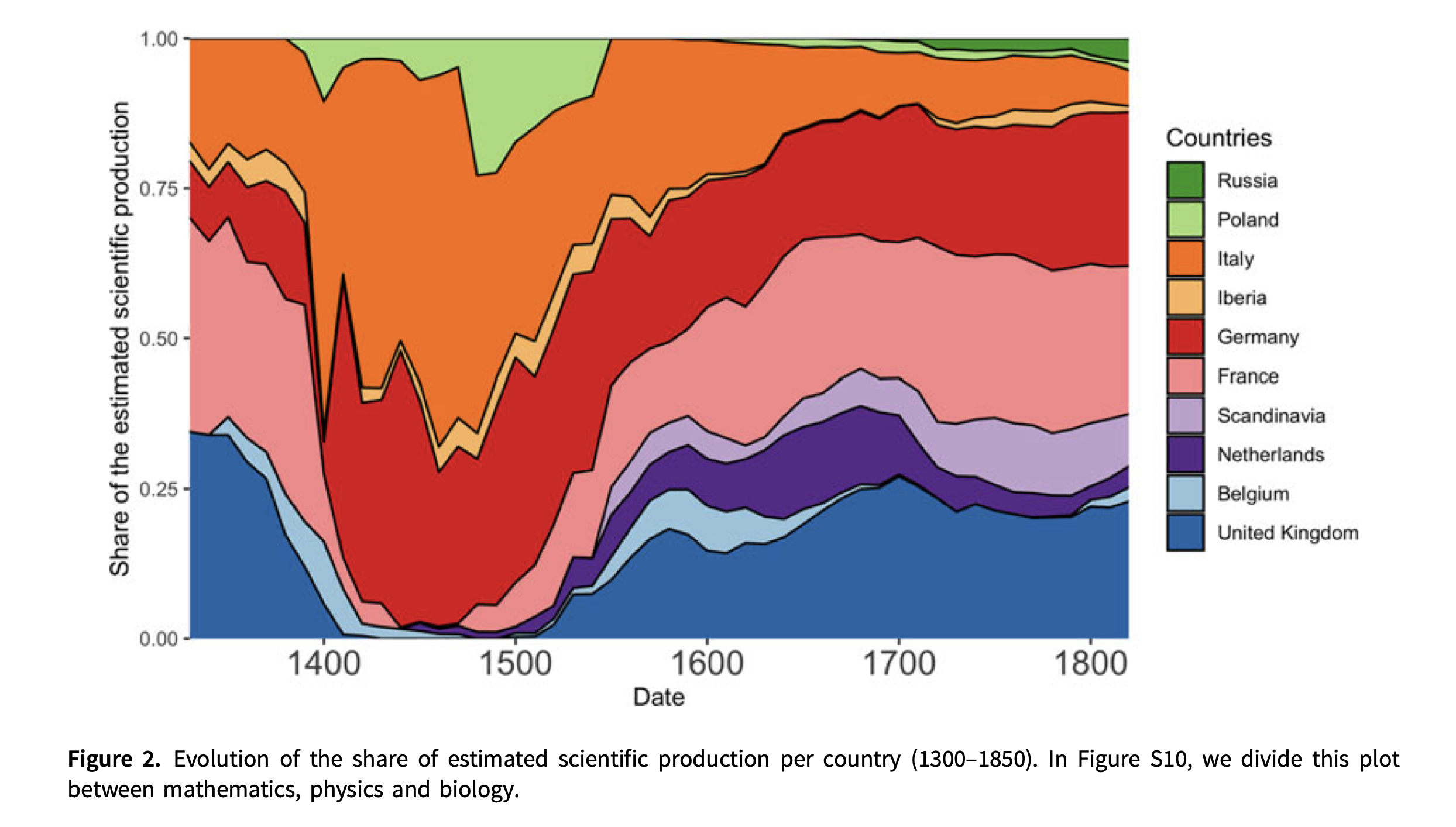

Fascinating chart showing how scientific revolutions progressed 1300-1850 between different countries.

“Here, we leverage large datasets of individual biographies (N = 22,943) and present the first estimates of scientific production during the late medieval and early modern period (1300–1850). Our data reveal striking differences across countries, with England and the United Provinces being much more creative than other countries, suggesting that economic development has been key in generating the Scientific Revolution.“