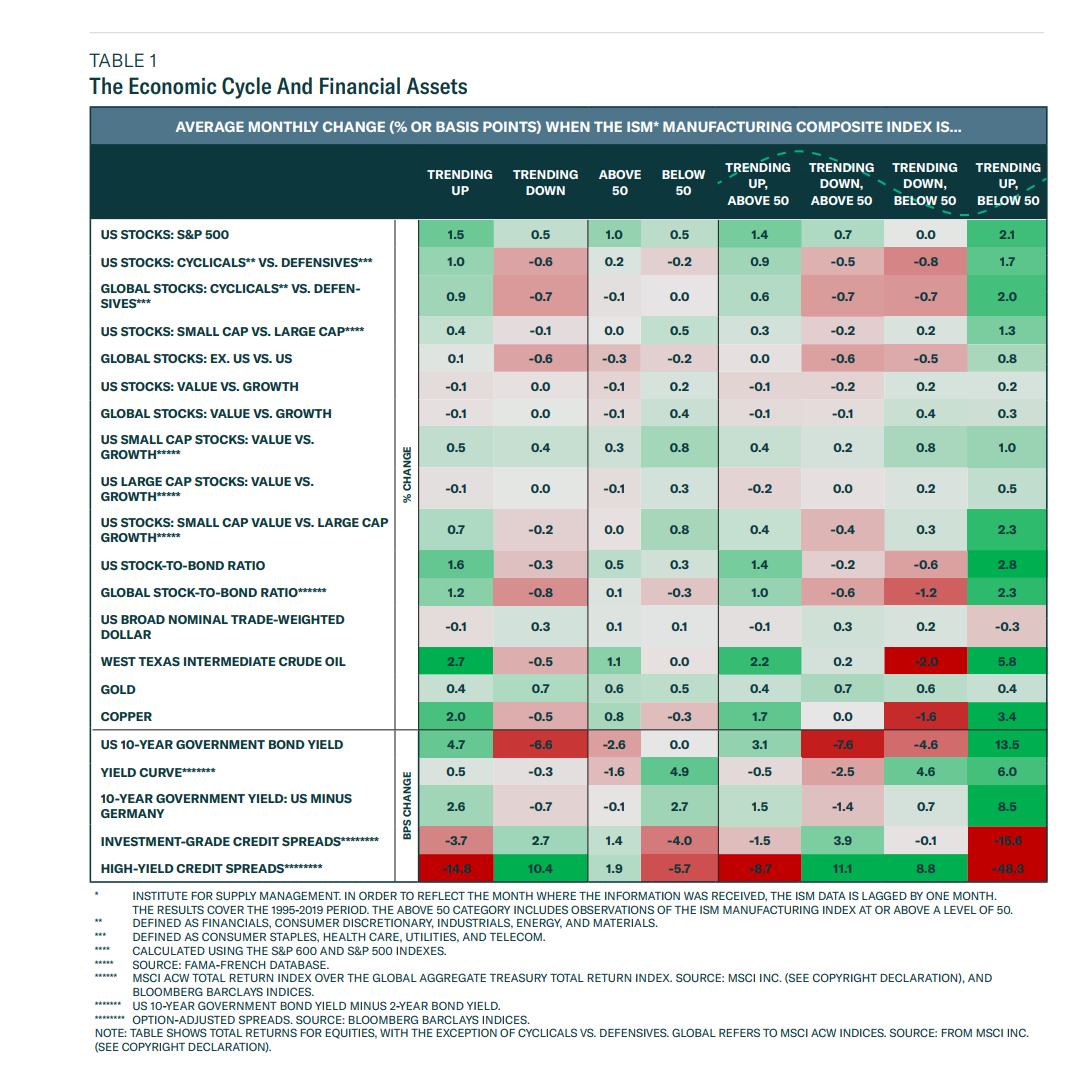

It shows how various financial assets (down the rows) react to the changing economic cycle (columns) as measured by the ISM Manufacturing Composite Index.

It covers the period 1995 – 2019.

Right now we are above 50 on the ISM index (59.9) but trending down.

How bad? “Forty million acres of land in the US consists of lawns. Maintaining them requires 800 million gallons of mower fuel and three million tonnes of (carcinogenic, endocrine-disrupting) fertilisers a year, and they guzzle up to 60 per cent of fresh water in urban areas.“

To make matters worse, grass only works as a carbon sink if it is left wild.

“Maintaining a patch of blank land on which no food grows, no animal feeds and no carbon is stored is as absurd as installing fake plastic grass.“

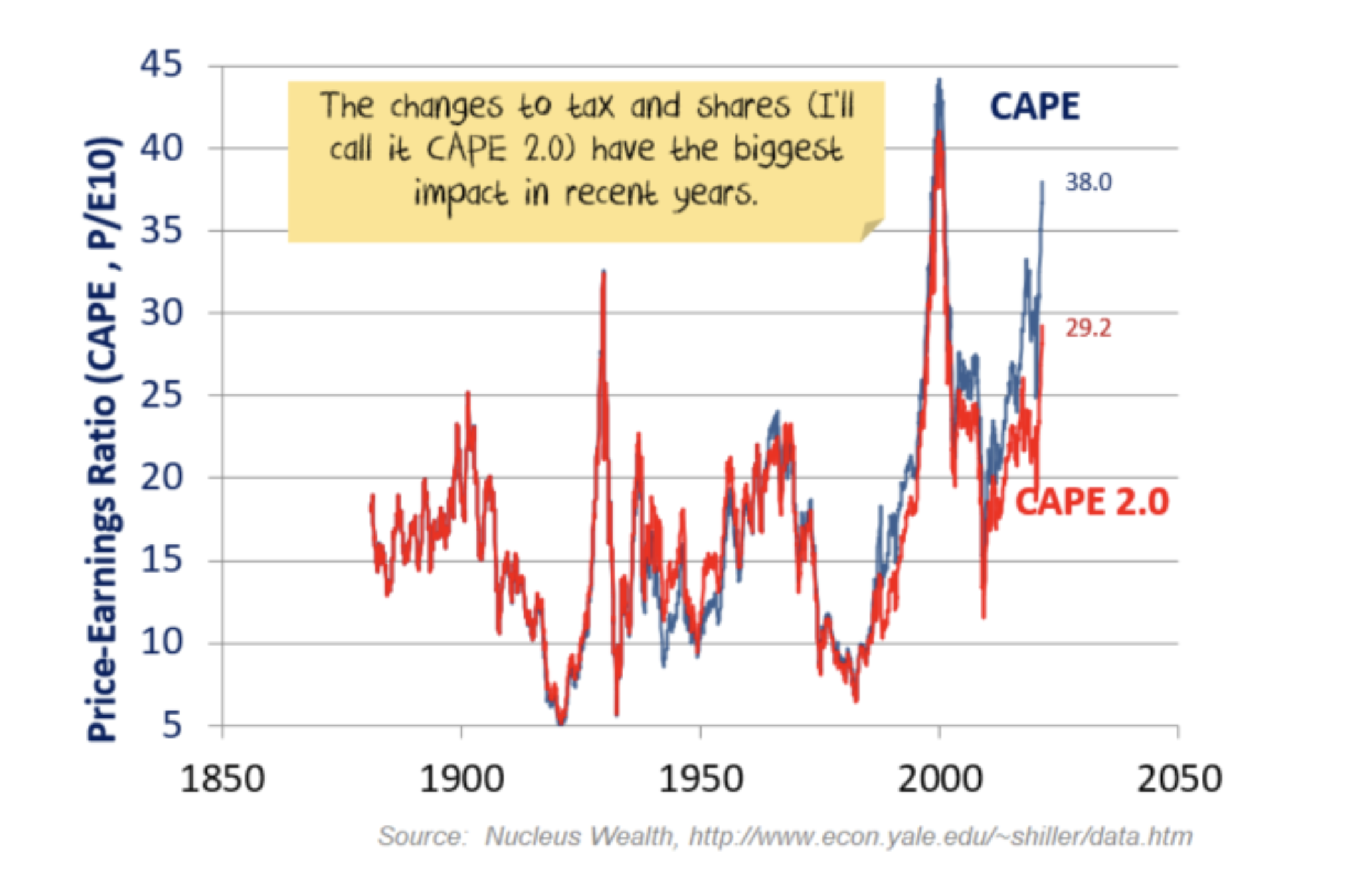

Interesting take on Shiller’s cyclically adjusted price earnings ratio (CAPE).

The analysis argues that one should be using today’s tax rate and adjusting for buybacks.

This leads to a CAPE 2.0 of 28x – far below the current CAPE of 38x and nowhere near the Dotcom peak.

This is the “basic” version and for those interested there is a more advanced (and more controversial) version that results in “the last 20 years go from being an expensive aberration to a typical investment period“.

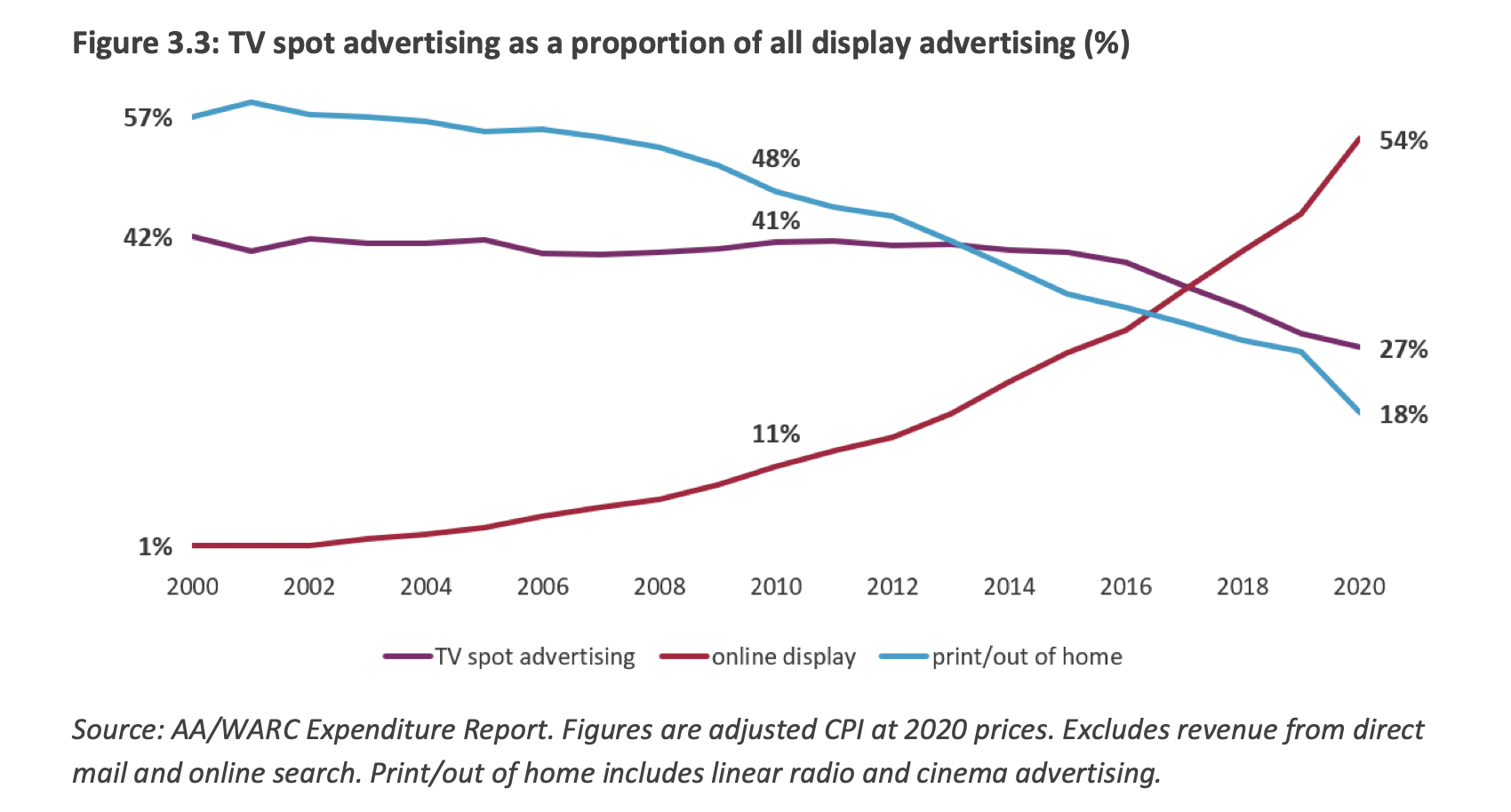

Online display advertising is rapidly displacing TV in the UK.

“However, despite the increase in online, TV advertising remains the medium of choice for big brands wanting to reach an audience quickly and at scale, with advertisers citing TV’s ability to drive both short-term sales and longer-term brand equity as a major advantage.”

The story of Renaissance Technologies and Jim Simons is worth reading in full.

But this post does a great job pulling out the key extracts.

One consistent feature of their success relates to this – “What you’re really modeling is human behavior. Humans are most predictable in times of high stress — they act instinctively and panic. Our entire premise was that human actors will react the way humans did in the past…we learned to take advantage.”

“Aptitude is the rate at which you level up, by changing the nature of the problem you’re solving (and therefore how you measure “improvement”). The interesting thing is, this is not purely a function of raw prowess or innate talent, but of imagination and taste.“

This is a nice way to think about learning in investing – as returns to a particular area diminish, it is key to open a new front.

“Crossover investors have become more active in Europe (e.g. Tiger Global, BlackRock, RA Capital, Coatue).

While in 2019 only 2 made the top 15 investor league table, now, as at the half year, 4 of these (all from the US) are part of the top 15, with the number 1 overall being Tiger Global.”