A great piece of analysis applying Helmer’s 7 powers to the content business in order to establish if content has ability to maintain profitability and resist competition.

Scale is one such power – this chart shows there is a slight positive linear correlation between size of budget and eventual box office returns.

Network effects are also interesting – given the social dynamics of shared experience and discussing content. Franchises really shine here.

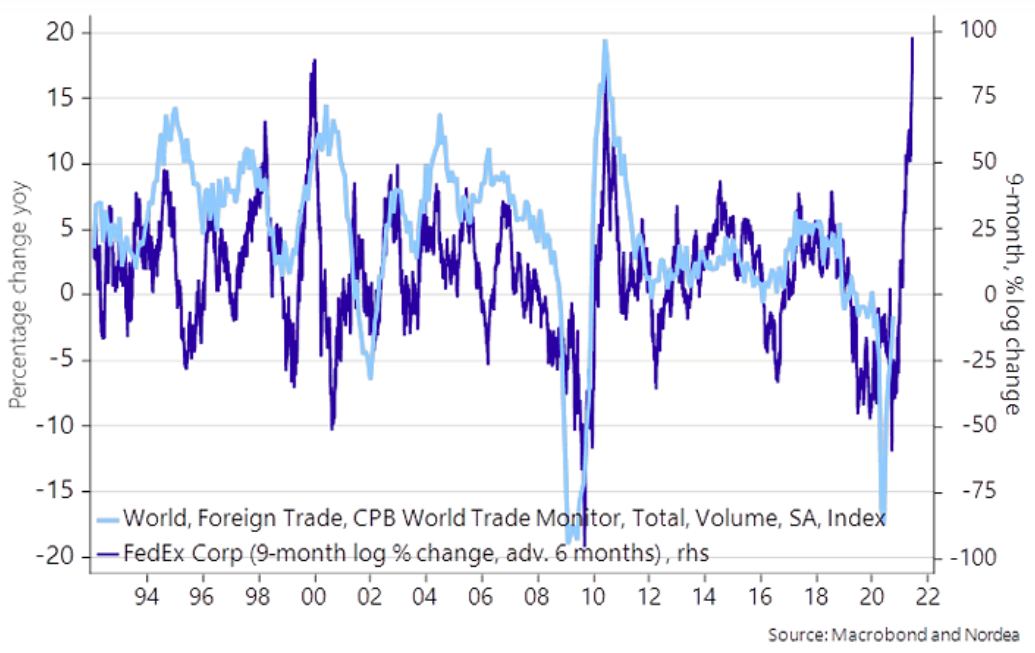

An investigation by Reuters suggests China is using “gray-zone” warfare to subdue Taiwan via military exhaustion.

“The risk of conflict is now at its highest level in decades. PLA aircraft are flying menacingly towards airspace around Taiwan almost daily, sometimes launching multiple sorties on the same day. Since mid-September, Chinese warplanes have flown more than 100 of these missions, according to a Reuters compilation of flight data drawn from official statements by Taiwan’s Ministry of National Defense.”

We leverage the Snippet ecosystem to expand our footprint holistically in the space we operate. We have a long runway for our KPIs. After all it is a global and iconic brand.

A fun list of banned corporate “words” from FundSmith.

Business lessons from a man who at one point commanded one in every nine dollars in the United States.

“Vanderbilt’s legacy provides timeless and universal lessons in business success. He thrived in an era of enormous technological change as railways revolutionised the American economy. Yet his approach to business is evident in many of the successful businesses we see today; tapping new markets through lower prices, respecting shareholders, sharing scale advantages and sacrificing short term profits for long term gains.“

Some amazing stats on the state of US federal finance – debt levels are about to hit World War II peaks (as % of GDP), and the projected 2020 deficit (at 16% of GDP) is the largest since 1945.

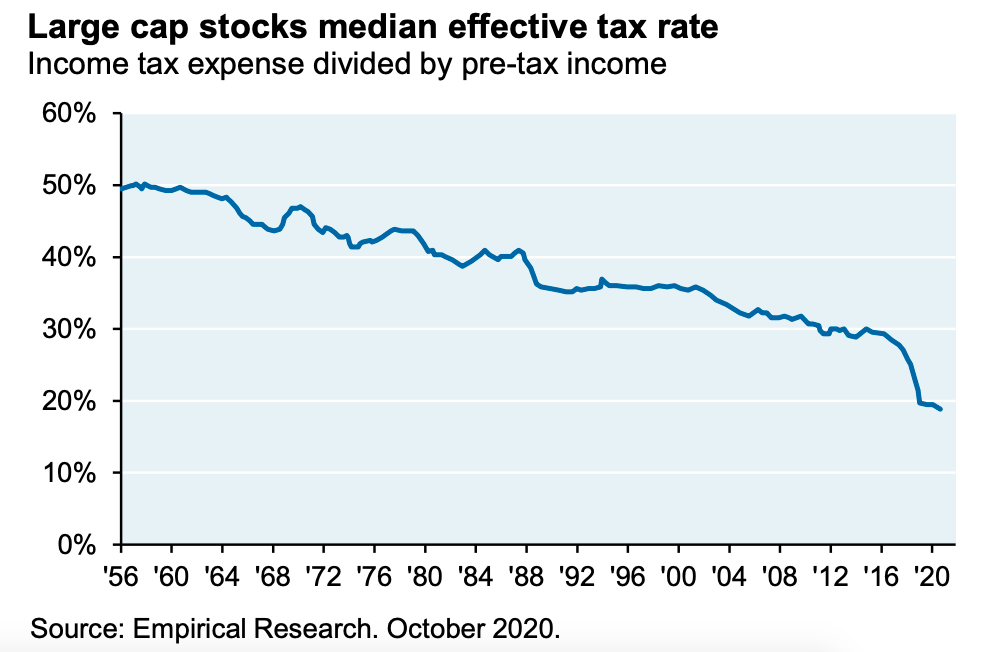

This interesting chart shows the fall in the corporate effective tax rate for large cap stocks over the years.

Under Biden’s plan – which will raise $2.2trn by raising and broadening corporate taxes (vs. $700bn Trump corporate tax cuts) – this trend could reverse (costing 10% of S&P EPS).

As the new year starts many, myself included, look to start forming new habits.

As the third instalment of the Snippet Blog I felt it would be useful to give a few tips on how to make sense of the world and separate signal from noise.

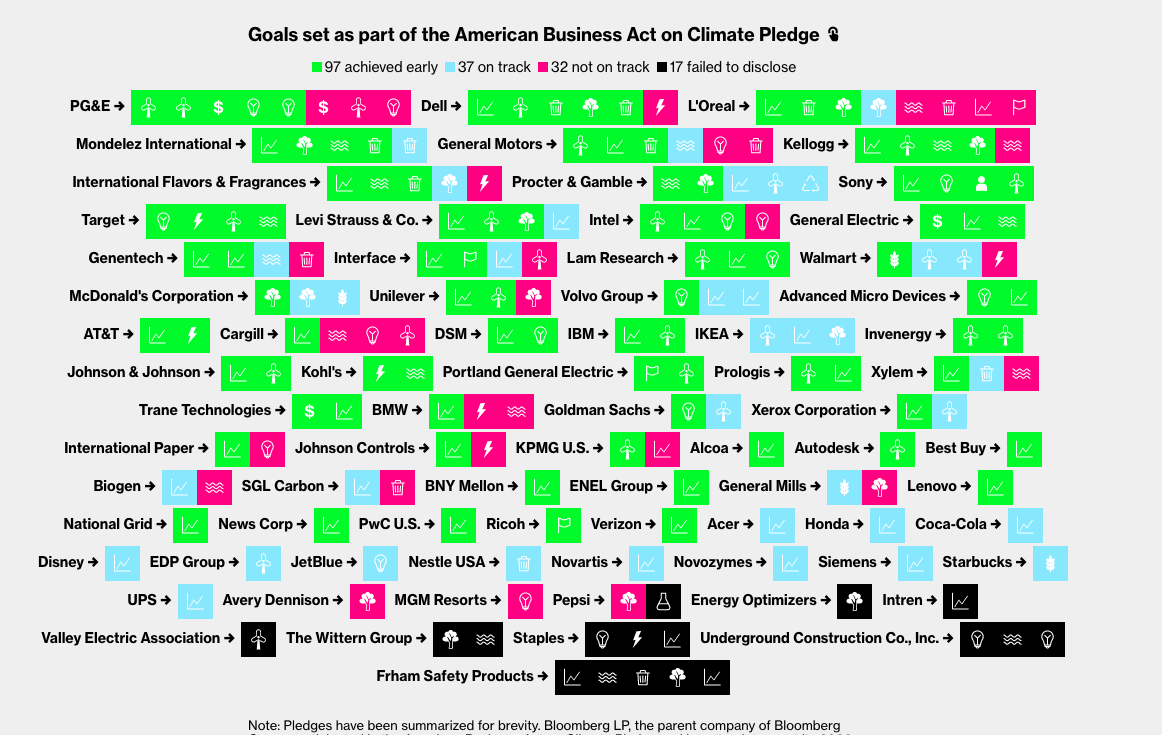

Bloomberg analysed how well companies fared against their 2020 climate goals (set in 2015).

“The good news is that most of these pledges—138, so far—have already been met or appear on track by year-end, in part because many companies set modest goals.“

Worryingly, data disclosure remains a big issue as many companies either don’t report or do so unevenly.

Looking forward many are now making stand out statements.

Microsoft has not just committed to going carbon negative (by 2030) they will, by 2050, remove from the environment all the carbon the company has emitted either directly or by electrical consumption since it was founded in 1975.

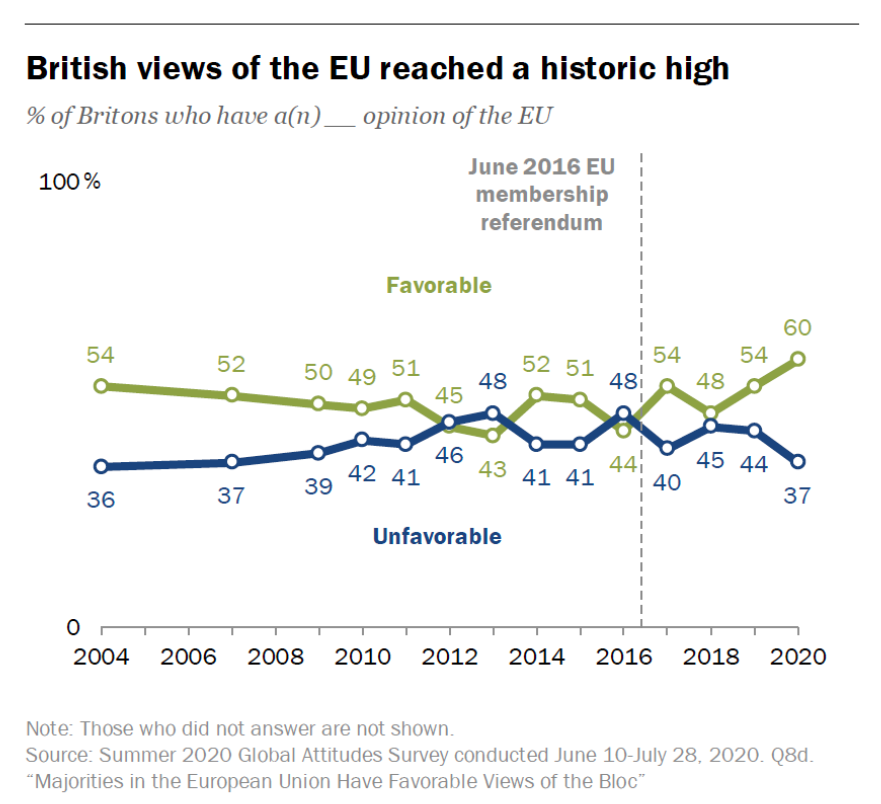

“In Pew Research Center’s first survey in the UK after Brexit, 60% of British adults said they had a positive view of the EU, up from 54% the year before and the highest percentage in surveys dating to 2004”