The partnership is an investment success story, outperforming the index by +14.3% per annum for thirteen years (2001 – 2014).

Although all are worth your time, this is nice blog post that pulls out some of the most interesting quotes and ideas. There are many.

“One trick that Zak and I use when sieving the data that passes over our desks is to ask the question: does any of this make a meaningful difference to the relationship our businesses have with their customers? This bond (or not!) between customers and companies is one of the most important factors in determining long-term business success. Recognising this can be very helpful to the long-term investor.”

This story of how brains evolved, while admittedly just a sketch, draws attention to a key insight about human beings that is too often overlooked. Your brain’s most important job isn’t thinking; it’s running the systems of your body to keep you alive and well. According to recent findings in neuroscience, even when your brain does produce conscious thoughts and feelings, they are more in service to the needs of managing your body than you realize.

Just as in tech companies, many sports franchises are trying to answer a basic question: what do the numbers today tell us about the possible outcomes of tomorrow — and what (or who) do we need to get to a winning outcome?

In basketball and tech in particular, a deeper understanding of efficiency — both in how to measure it and how to leverage that to build winning teams — and usage has changed the game in the last decade.

A great piece applying NBA sports metrics to Start-ups.

We previously covered this brilliant list of 52 things learnt for 2019 and 2018.

Here is the 2020 edition – full of gems. A few choice examples:

Most cities plant only male trees because it’s expensive to clear up the fruit that falls from female trees. Male trees release pollen, and that’s one of the reasons your hay fever is getting worse.

For VC companies in 2004, the average time from first contact to funding was 90 days. Today, it’s just nine days

Car safety laws in the US make it more expensive to have three children — women in states with mandated car seats are 0.7% less likely to have a third child. The safety measures may have saved 57 car crash fatalities each year, but caused 145,000 fewer births since 1980.

Developing and launching the iPod in 2001 took just 41 weeks, from the very first meeting (no team, no prototype, no design) to iPods shipping to customers.

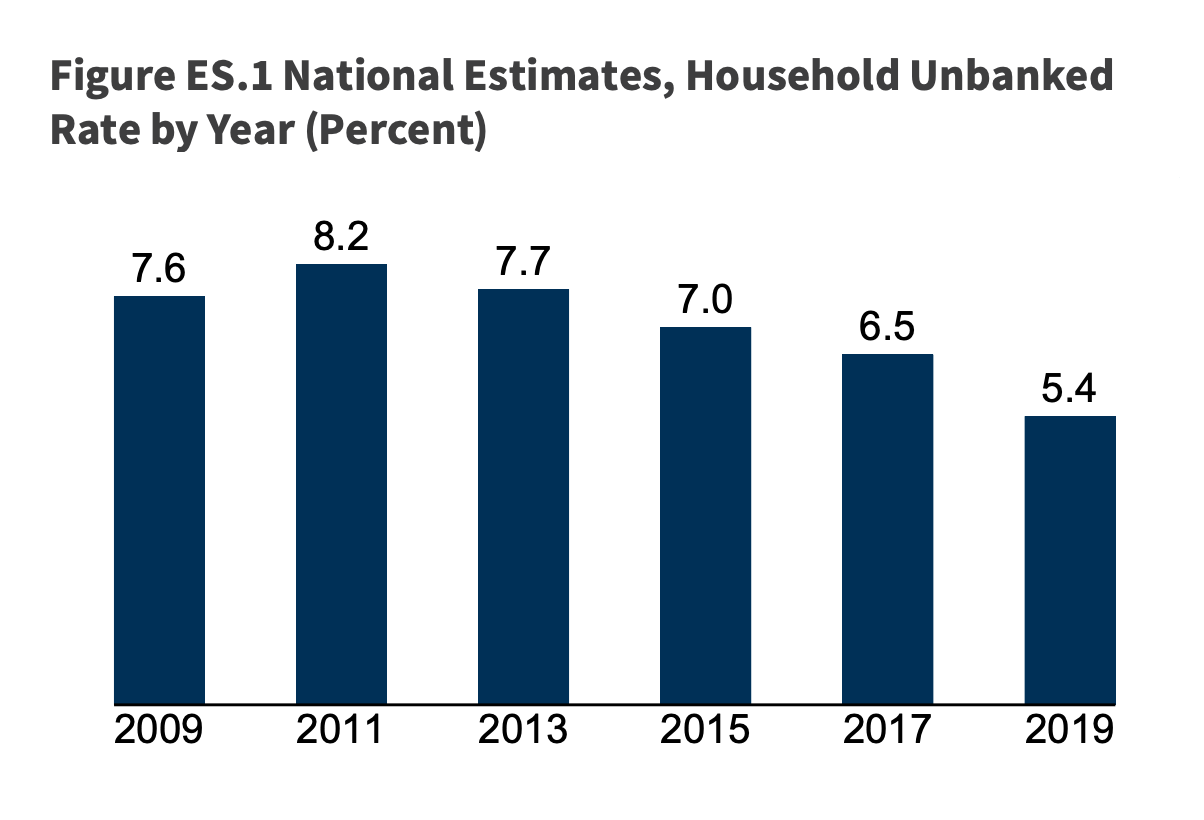

5.4% of households in the United States remain unbanked, meaning that no one in the household had a checking or savings account at a bank or credit union (i.e., bank), down from a peak of 8.2%.

Explains moves in the US to introduce the Public Banking Act.