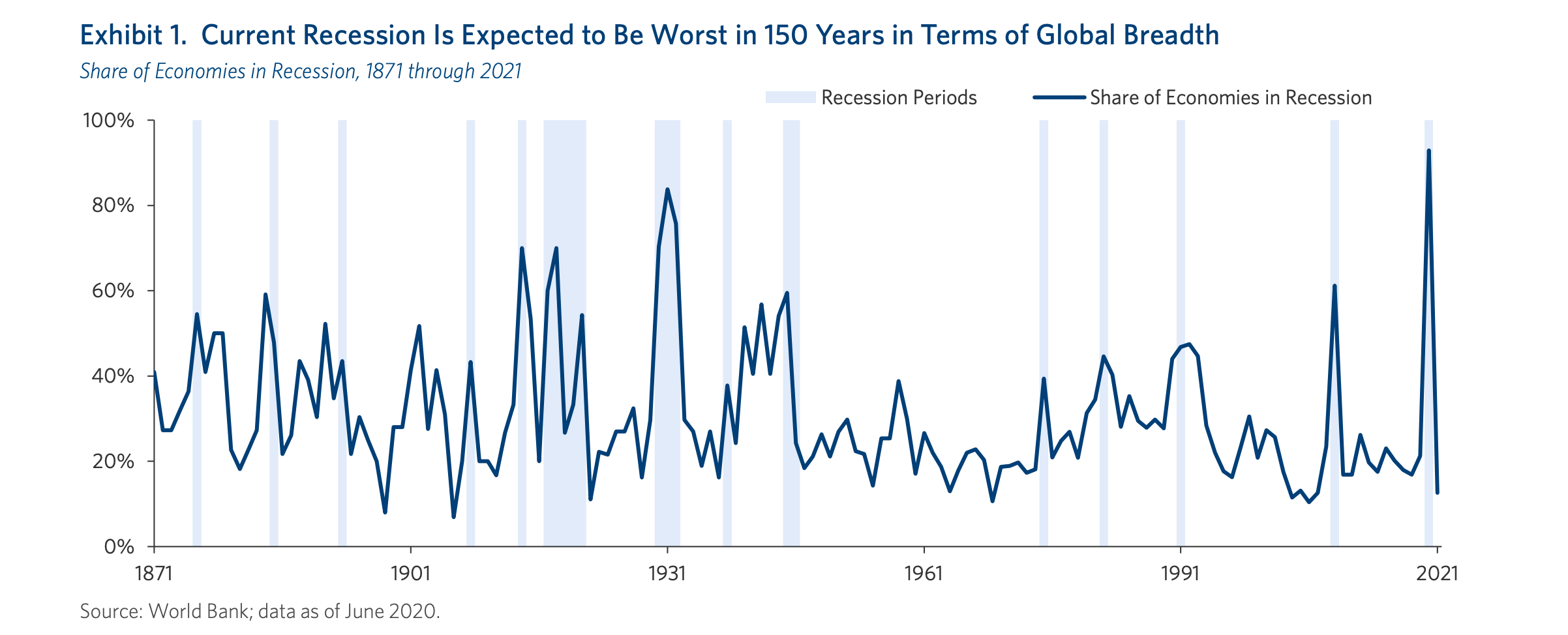

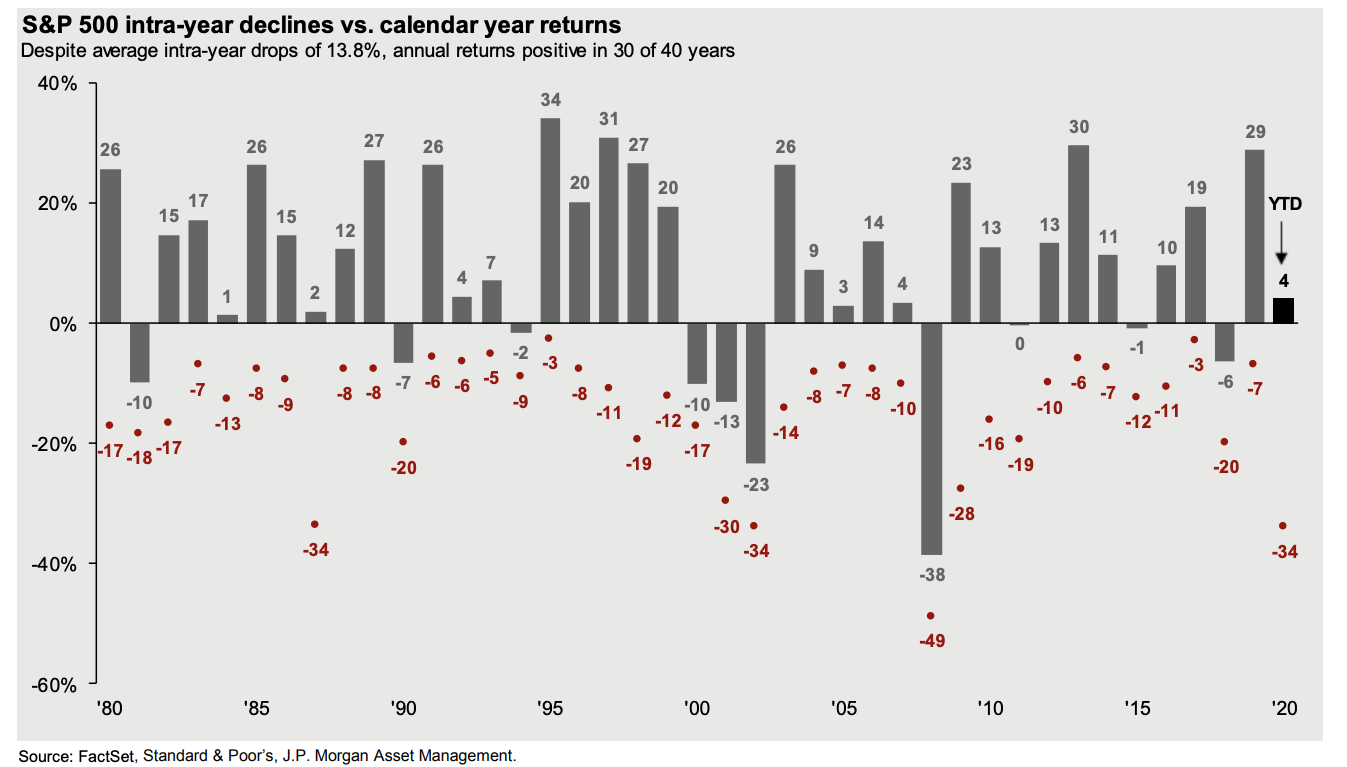

The World Bank is forecasting that more than 90% of the world’s economies were in a recession – the most broad based contraction of the past 150 years.

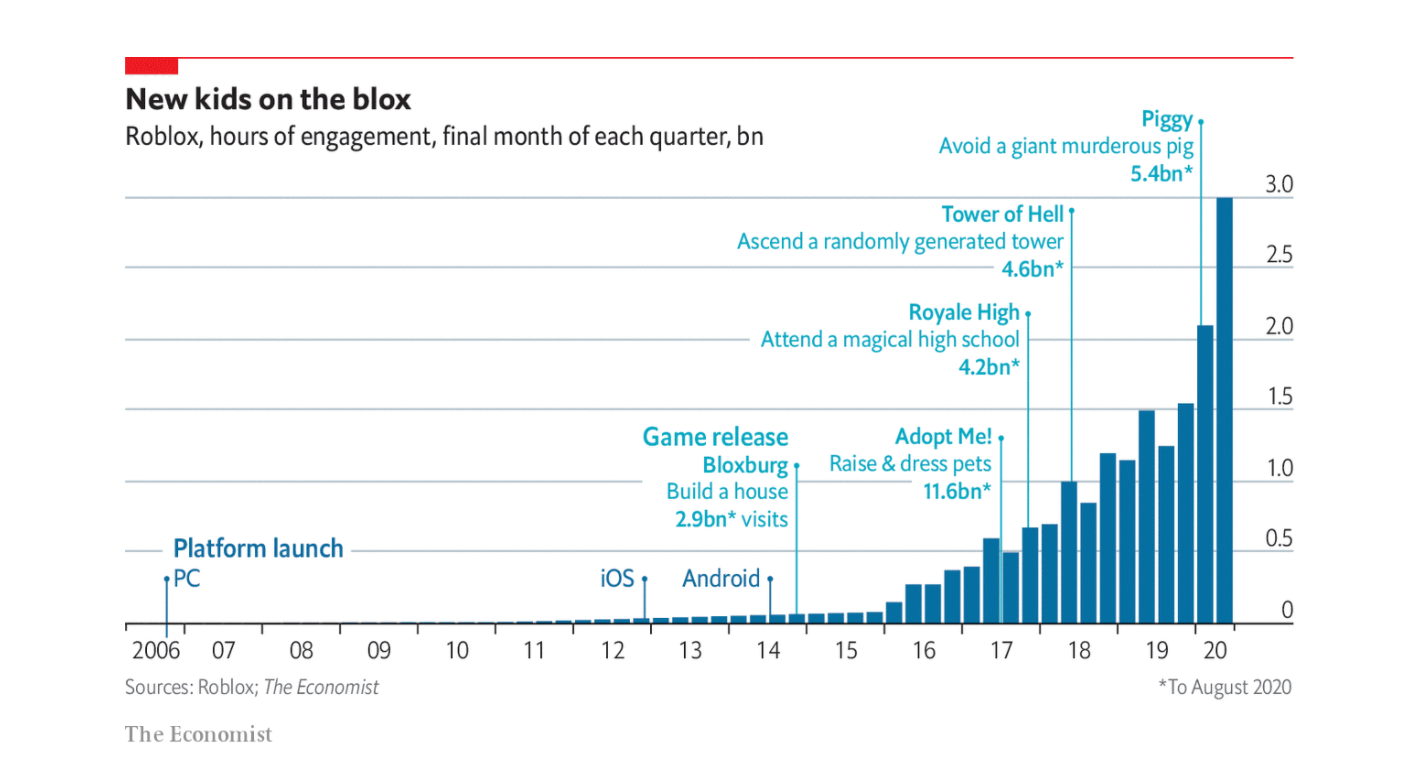

Remarkable chart. Sourced from a nice presentation on China.

“A great meeting has three key elements: the desired outcome of the meeting is clear ahead of time; the various options are clear, ideally ahead of time; and the roles of the participants are clear at the time.“

“I think that’s the single largest source of optimization for a company: the makeup of their meetings. To be clear, it’s not about fewer meetings because meetings serve a purpose. Rather, it’s key to improve the meetings, themselves. A lot of my efforts focus on teaching people this framework. Ironically, I find that most people are just challenged by that stuff.“

Really good long read from Guardian on the state of the airline industry.

What it takes to store planes at Schipol is fascinating:

Fuel tanks were emptied, although not entirely: “You still need some weight in the plane, for the bursting wind we get here in Amsterdam.” The blades of the engine fans were locked into place with straps, so that, on gusty days, they didn’t whirl around endlessly and wear their parts out.

Every seven days, someone would climb into the plane and run the engines for 15 minutes to keep them functional. The air conditioning was switched on to keep the humidity at bay. “And the tyres – well, it’s the same as a car. If you keep a car parked for more than a month, you get flat tires,” Dortmans said. So a tug pulled the plane forward and back every month, to keep the wheels and axles in shape.

Still, there were some surprises. In the absence of the roar of jets, birds began to appear around Schiphol again, and one day, a ground engineer told Dortmans that he’d found a bird starting to nest in a cavity in the auxiliary power unit. “I’m hearing all these birds and now I find this,” he told Dortmans. “It feels like I’m out in the woods.”

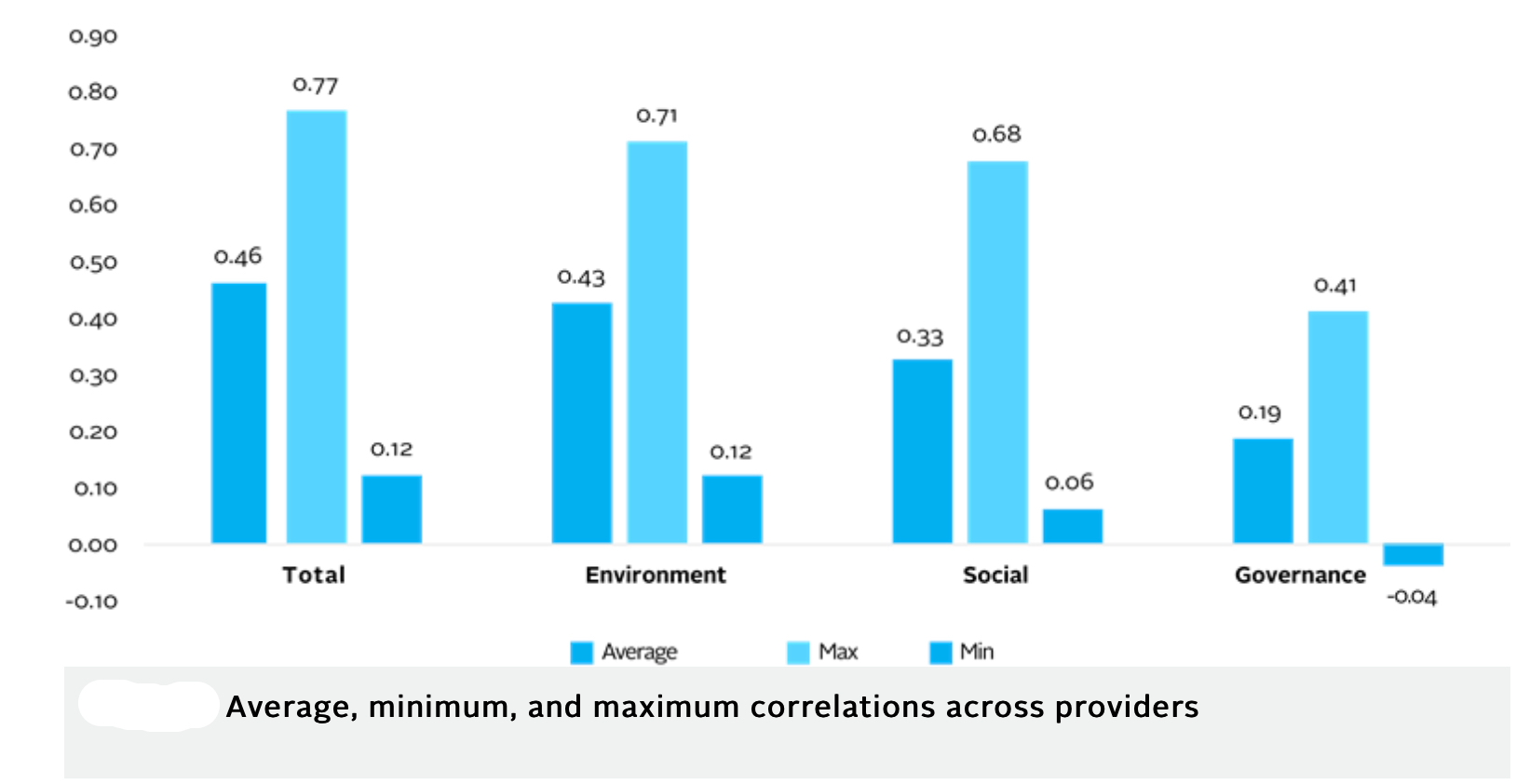

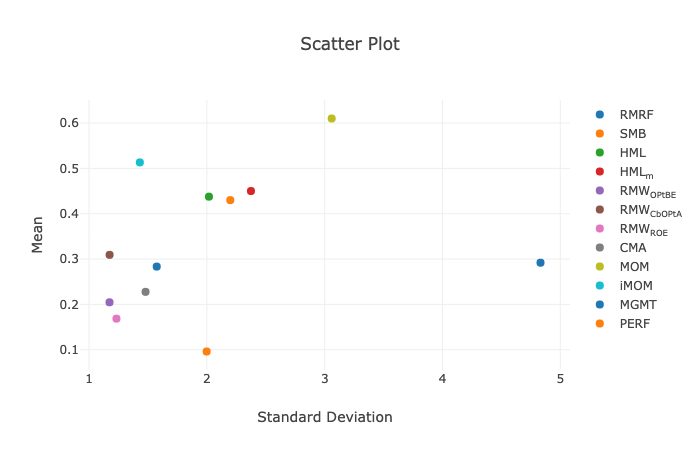

Current ESG scores are contradictory as seen in the chart showing correlation across providers.

This point, rarely raised about ESG, argues that markets adjust to price things in – “If there is an investing lesson embedded here, it is the unsurprising one that investors who hope to benefit from ESG cannot do so by investing mechanically in companies that already identified as good (or bad), but have to adopt a more dynamic strategy built around either aspects of corporate social responsibility that are not easily measured and captured in scores, or from getting ahead of the market in recognizing aspects of corporate behavior that will hurt the company in the long term.”

Very comprehensive post on the landscape of companies involved in financialising new asset classes or democratising access to existing ones and creating markets.

“Whether it’s the long tail of “alternative alternative” assets, venture-backed company shares, software contracts, or sport teams the financialization of everything is on its way.”

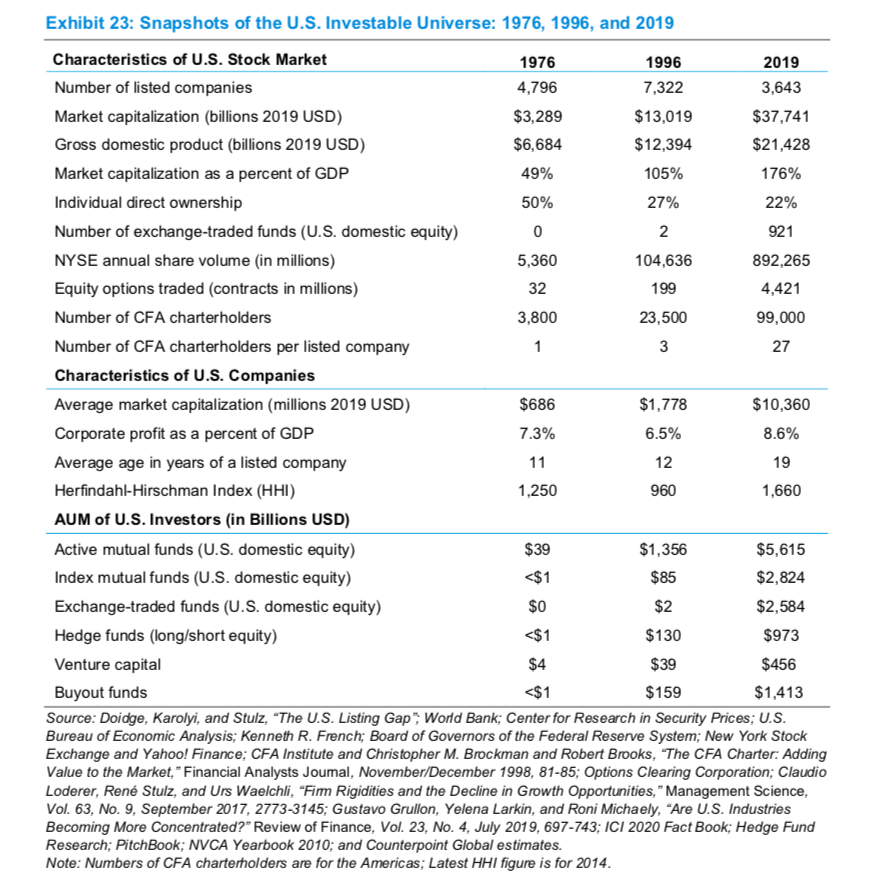

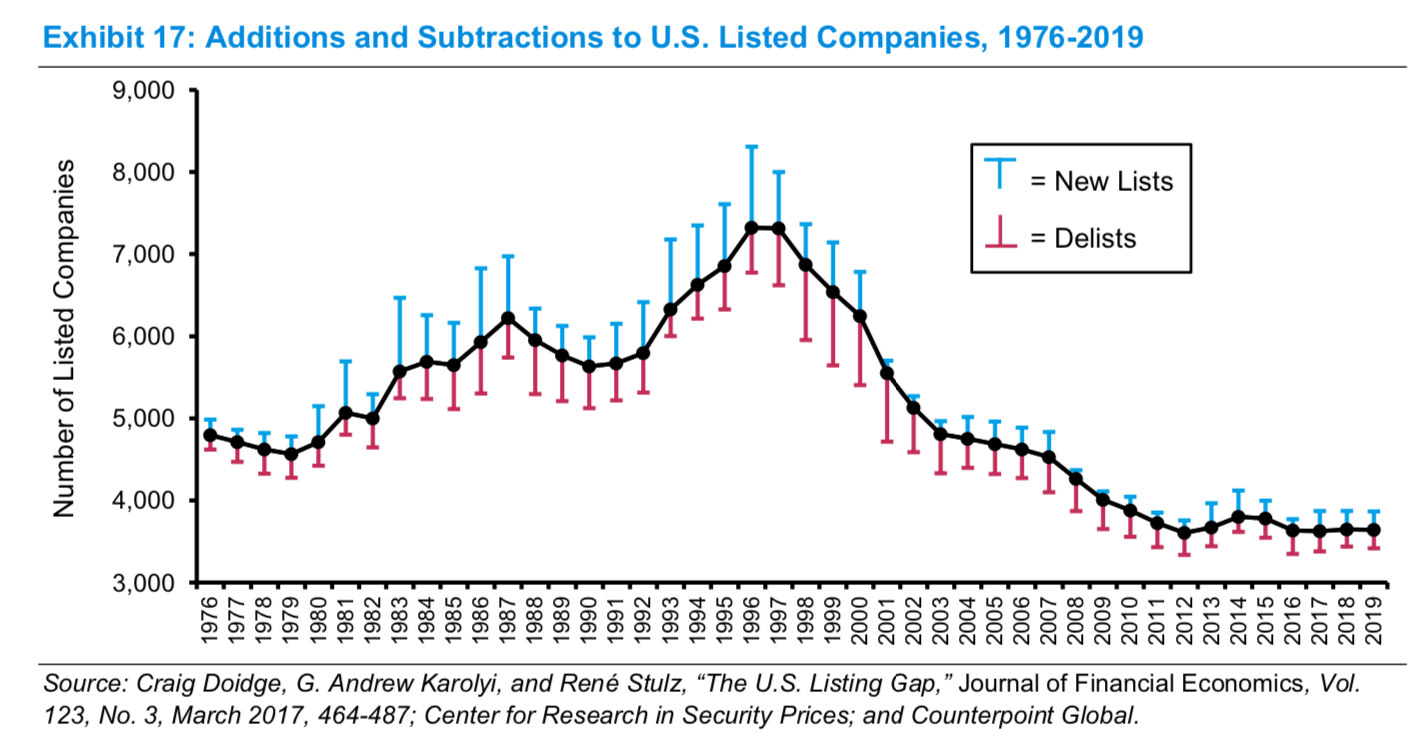

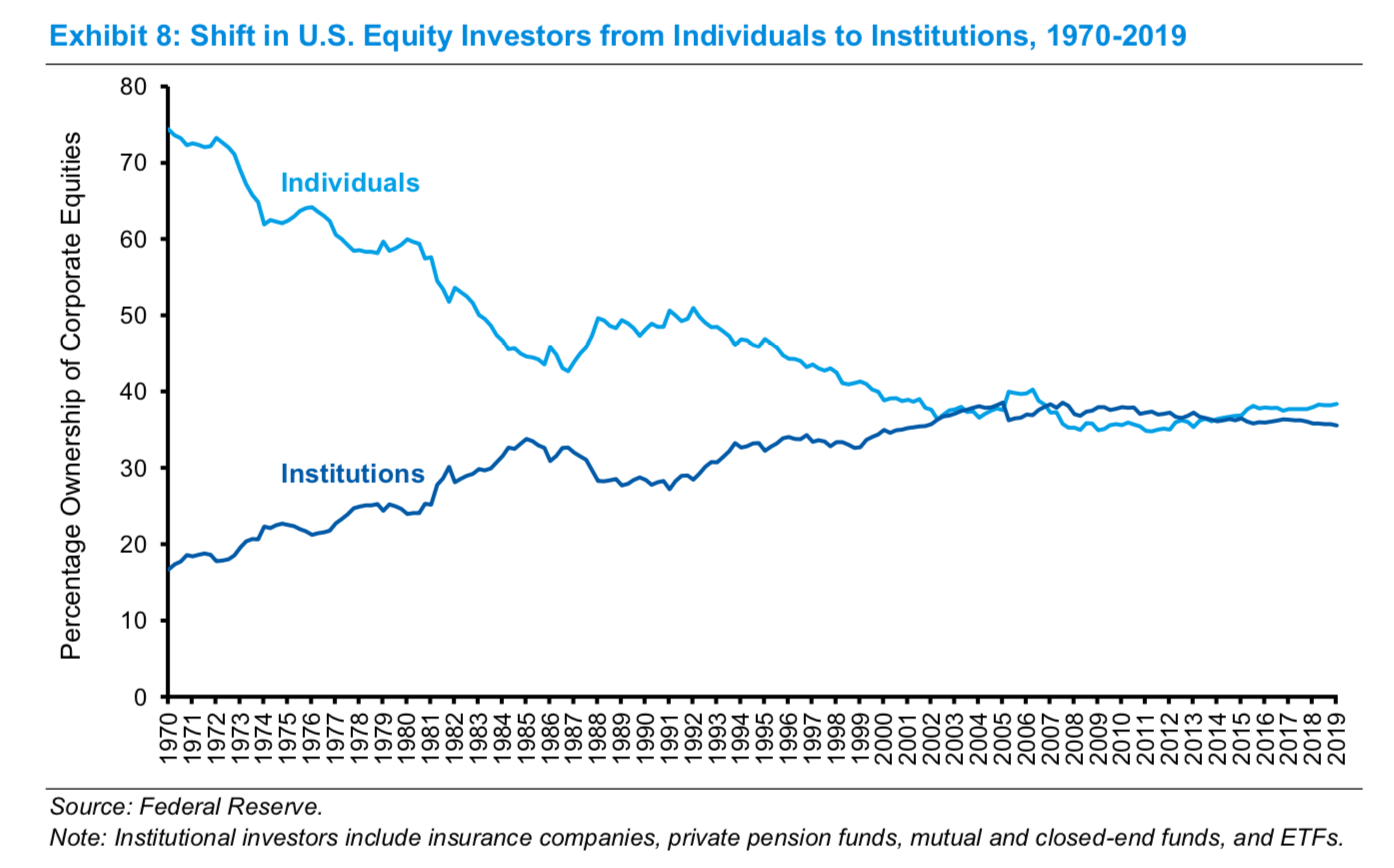

The number of publicly listed companies in the US has fallen since the mid-1990s.

This chart captures this decline in the total number of listed stocks, including additions and subtractions each year from 1976 to 2019.

“There are one-half as many public companies as there were in 1996 and three-quarters as many as there were in 1976. The Wilshire 5000 Total Market Index, launched in 1974 to reflect the complete U.S. equity market, had 3,473 stocks as of December 31, 2019.”

“Over the past quarter century there has been a marked shift in U.S. equities from public markets to private markets controlled by buyout and venture capital firms. This change has had reverberations for asset managers, investors, executives, and policy makers.“