On culture – “part of daily life at Netflix with a daily Circle of Feedback and annual written and live 360 Assessments, in which you meet with the team to get ripped apart.“

Bessemer Venture Partners are famous for publishing their anti-portfolio.

Recently they took to learning from their success and published a series of memos from some of their most successful venture investments.

“One pattern that consistently emerges is that Bessemer’s best investment decisions centered on people. In retrospect, the early products themselves are barely recognizable today. Rather, passionate, analytical and relentless founders zigged and zagged their way to that elusive “product-market fit”, and these memos provide a glimpse of those winning entrepreneurs before they were famous.“

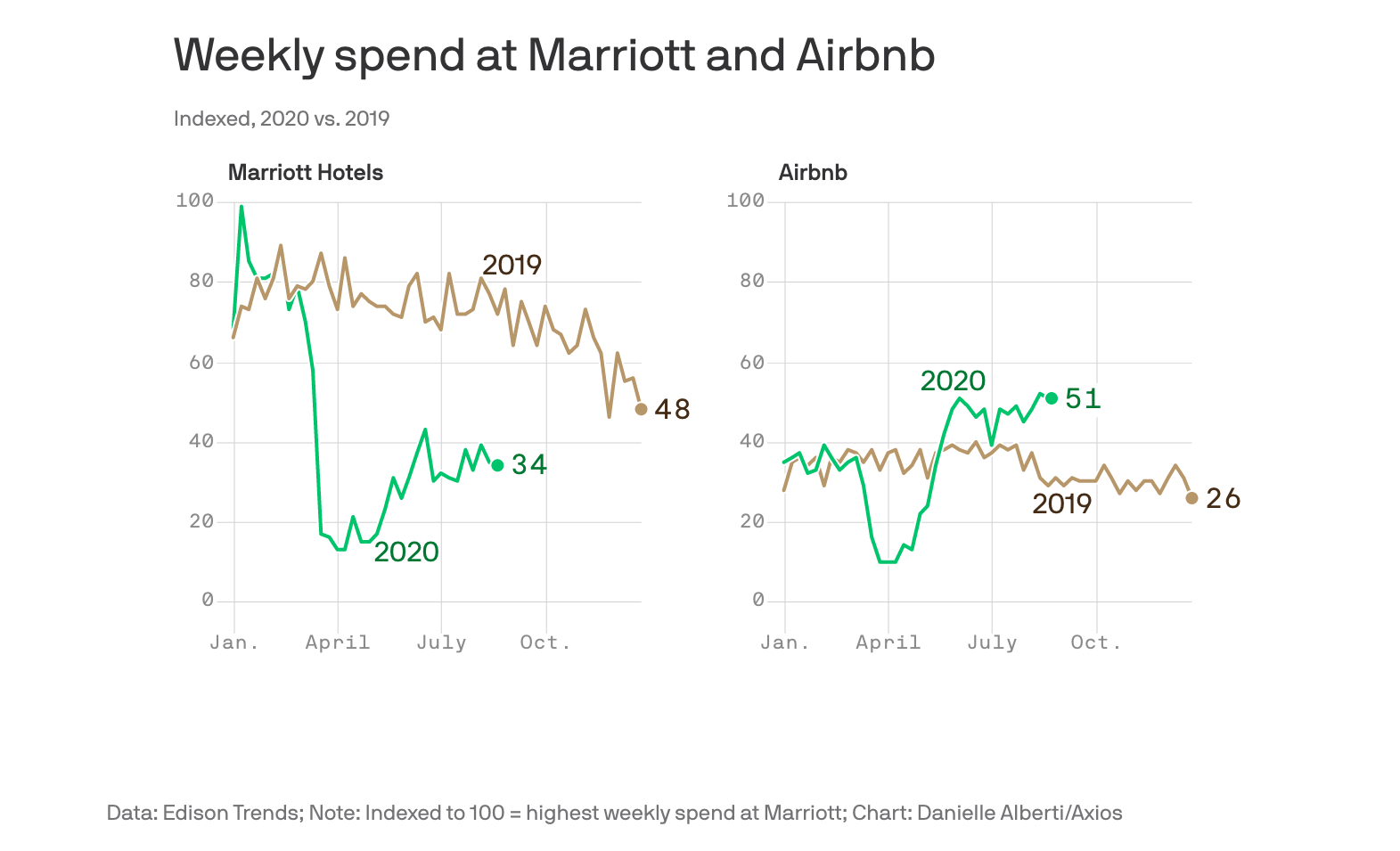

“Airbnb spending is running a whopping 75% higher than this time last year according to Edison Trends, based on a panel of spending data including more than 65,000 Airbnb transactions.“

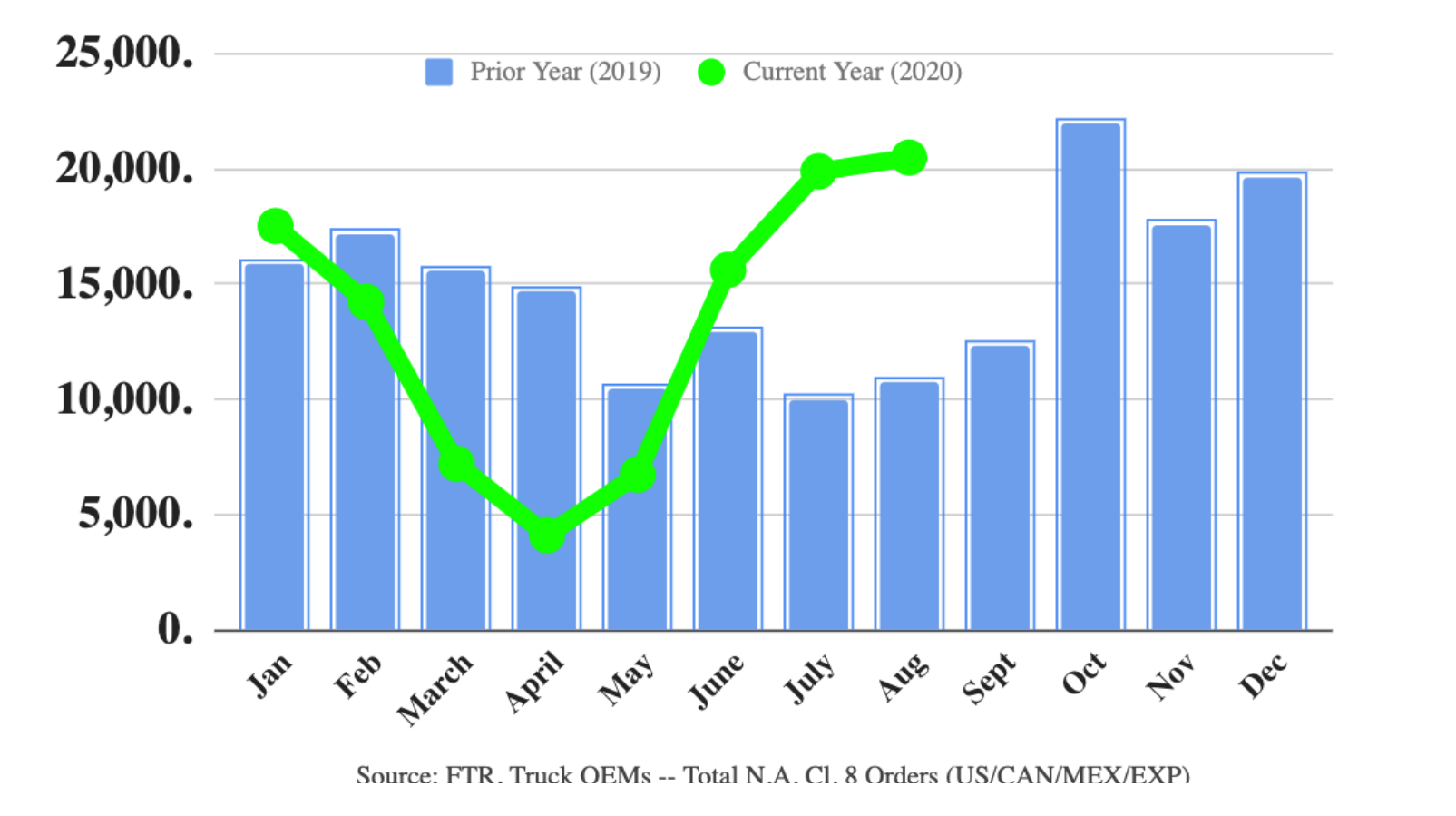

The very economically sensitive orders of heavy (Class 8) trucks in the US continue to be robust.

“This is an odd situation. We are in a highly uncertain, yet very stable, environment. You have a pandemic, a presidential campaign, and social unrest all occurring at the same time. However, the economy is briskly recovering and generating ample freight. Fleets are ordering only what they need, and thus, orders are aligning very closely to production rates.“

“It took nearly a century for the flush toilet to approach 80% household penetration. Electricity took 30 years to get to 80%; Refrigerators 20 years; cell phones 15 years; Social media 12 years.“

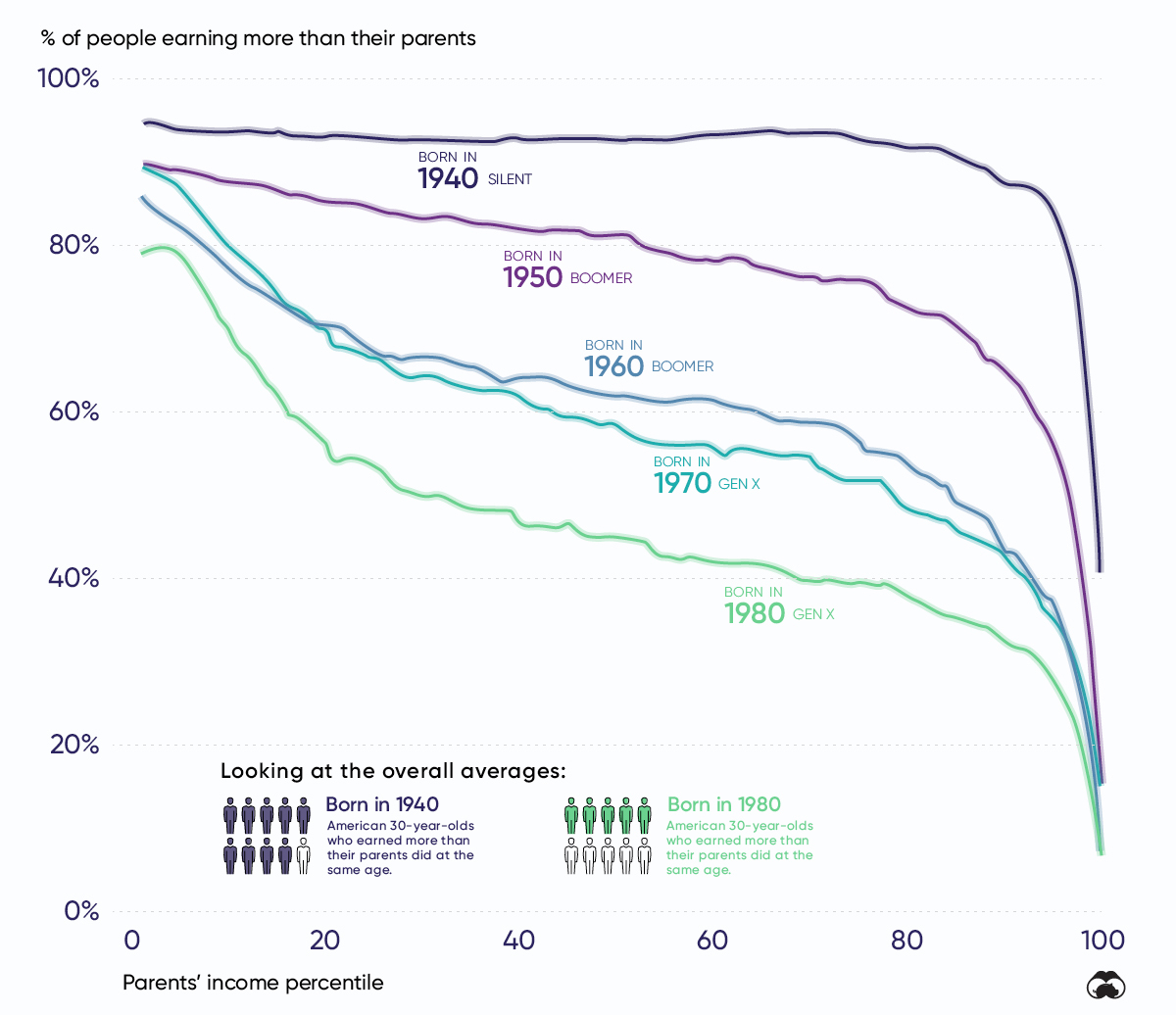

“This graphic plots the probability that a 30-year-old American has to out earn their parents (vertical axis) depending on their parent’s income percentile (horizontal axis). The 1st percentile represents America’s lowest earners, while the 99th percentile the richest.“

Take the 50th percentile (“middle class”) – the probability of someone out-earning their parents has fallen precipitously – it was 93% for people born in 1940 and dropped to 45% for those born in 1980.