One of the better investment books around is exactly about that.

A personal favourite was when Stanley Druckenmiller got himself involved in Tech stocks at the top of the dot-com bubble.

“Druckenmiller knew exactly what he was doing – he just couldn’t stop himself. ‘I bought $6 billion worth of tech stocks, and in six weeks I had lost $3 billion in that one play. You asked me what I learned. I didn’t learn anything. I already knew that I wasn’t supposed to do that. I was just an emotional basketcase and couldn’t help myself. So maybe I learned not to do it again, but I already knew that.‘”

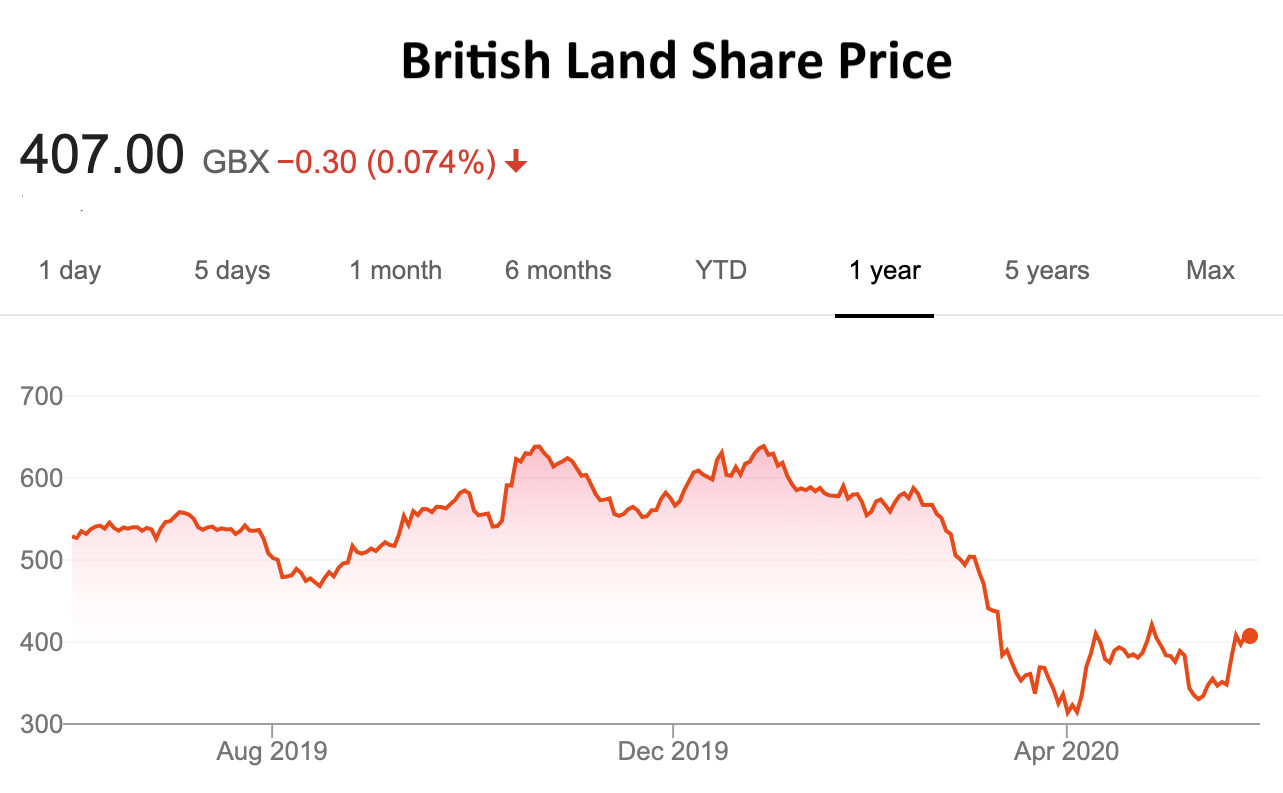

Brookfield have declared a 7.3% stake in British Land (BLND) – the UK property company.

This is interesting as Brookfield in the early 2000s bought a stake in Canary Wharf Group eventually, in 2014, taking it over (together with QIA via Songbird).

An interesting post taking a step back and understanding the investment landscape as a game including appreciating the other players and stages of development.

“Each year around 100,000 new college graduates apply for internships at investment banks. Around 10,000 get a spot. After three years of banking boot camp, roughly 4,000 of these analysts want to become investors. Add in some analysts from management consulting and accounting firms, plus a handful of lawyers, and you get around 6,000 talented candidates interviewing for buy-side positions. About one in six gets a seat. So imagine a new cohort of roughly 1,000 twenty-somethings joining 15,000 existing analysts and portfolio managers at hedge funds, and another 30,000 long-only investors.”

This is an inspiring post on how some of the biggest consumer apps acquired their earliest users.

Pinterest’s strategy was eye catching and shows real hustle – “We did all kinds of pretty desperate things, honestly. I used to walk by the Apple store on the way home. I’d go in and change all the computers to say Pinterest. Then just kind of stand in the back and be like, “Wow, this Pinterest thing, it’s really blowing up.”

Snippet Finance – While we are on this topic, I’d like to take this opportunity to thank our subscribers and hope you are enjoying the content. A lot of effort goes into curating and selecting only the most valuable snippets to inform and inspire. The best thing you can do to support the site is spread the word – each of you might have one person you know who could benefit, please do send them a link and tell them about it. Thank you in advance.

{kind=link}