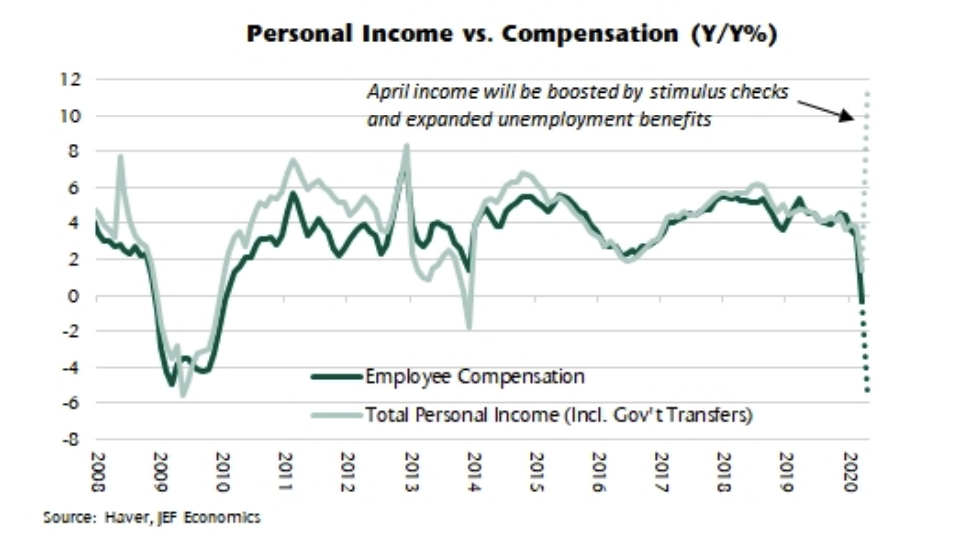

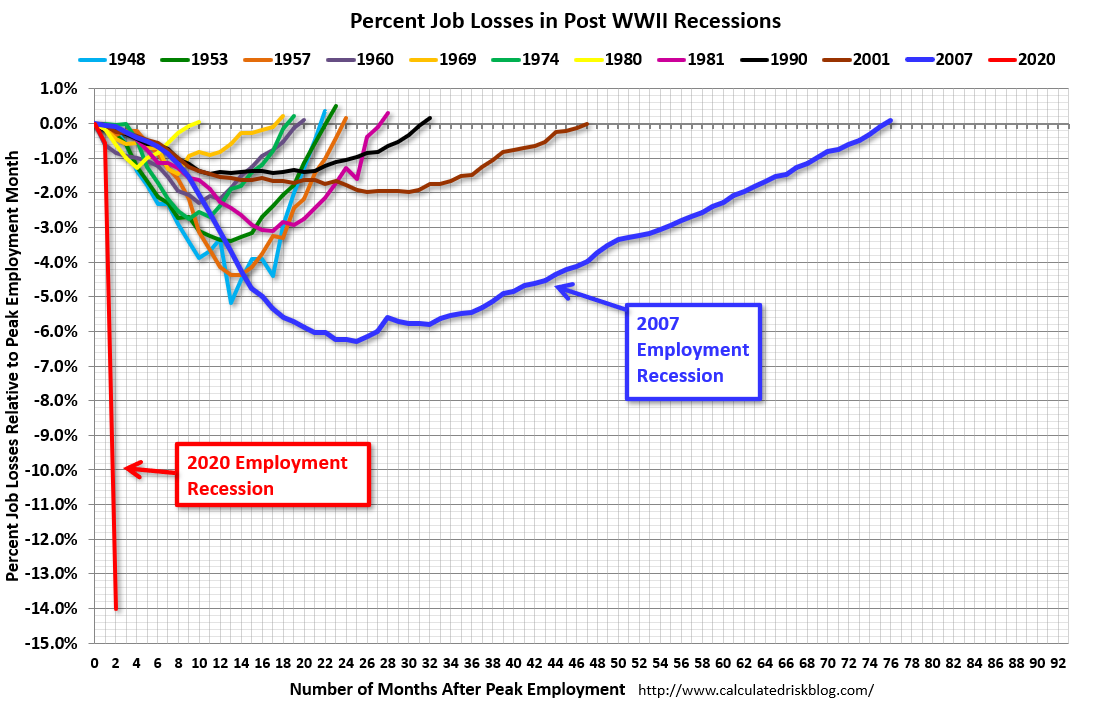

Interesting chart from Jefferies on the US Economy.

They crunched the numbers and found that, because of various bits of stimulus more than offsetting falls in compensation, personal income has actually surged in April.

Stimulus is of course front-end loaded and, unless extended, this picture likely fades with time.

Nevertheless, it is very interesting to see how strong its impact has been.

“I am pleased to say, but I would not get overly excited about it, that we have seen nice growth coming into May. And essentially, what we have seen is both growing out green shoots in the areas you would expect, places where movement has become possible, where people can now start to think about their summer holidays, et cetera. We see that very quickly when that happens and cancellations have settled down. They are still at elevated levels, but they have stabilized.”Expedia Q1 2020.

“what we are seeing clearly is what you have been hearing that local, regional, domestic is certainly coming back stronger sooner.” Expedia Q1 2020.

“we are seeing a significant number of hits in searches over the weekend, particularly I think from families looking at going on the two weeks summer holiday from Northern Europe to places in Italy, Spain, Portugal, et cetera.” Ryanair Q4 2020 Results.

Really great article on Sony and their current CEO – Kenichiro Yoshida.

This was a nice quote about the CEO – Yoshida’s humility is expressed through curiosity. “He came to me and said, ‘Let’s talk about medical things,’ and we met for dinner,” said Toru Katsumoto, who heads Sony’s medical business and research and development, of their first meeting. “I spoke about medical imaging and tried to explain the technology as simply as possible, but he had read a lot before we met. I was surprised and impressed. Once or twice a month, we have a face-to-face meeting and we exchange ideas freely.”

The big thing about Sony today is the analogy with Microsoft – “A lot of what Nadella did was capitulate and say, ‘This is where we are now and this is what we are going to do,’ rather than chasing the glories of the past.”