Fascinating that the presumed beneficiary is actually struggling.

“if customer behaviour were to return to normal by August it is likely that the additional cost headwinds incurred in our retail operations would be largely offset by the benefits of food volume increases, twelve months’ business rates relief in the UK and prudent operations management.”

There are clearly huge operational challenges.

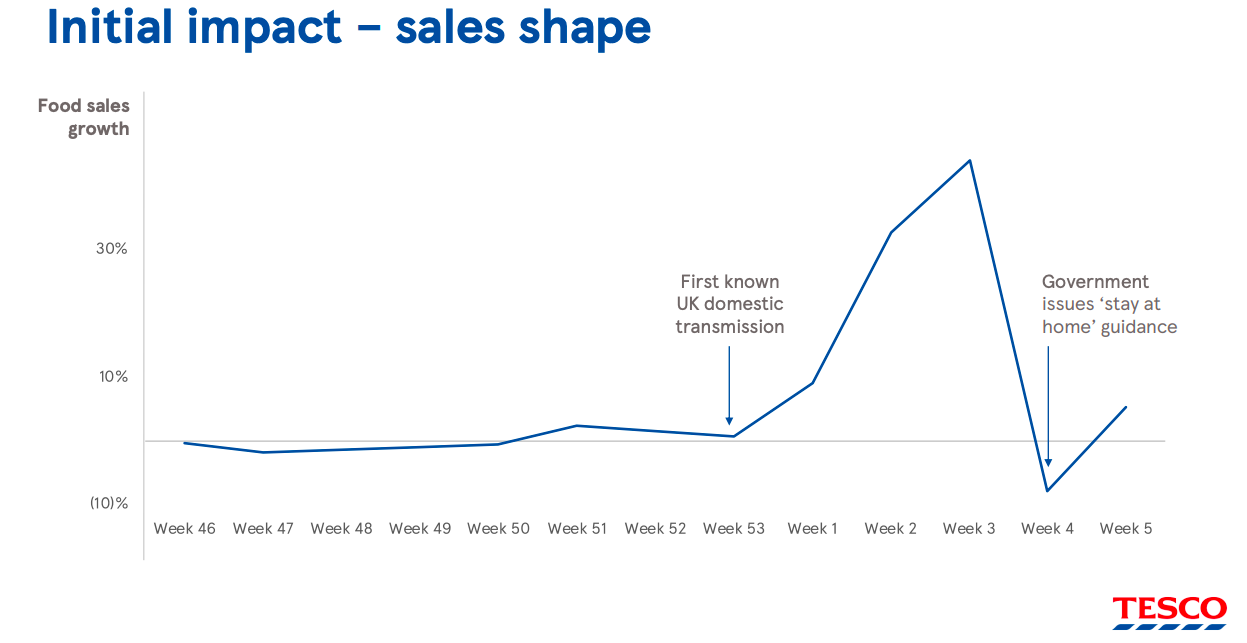

Interestingly – the initial spike in volume (pictured) was driven by 30% of customers buying 60% of the volume (slide 23). Certain items flew off the shelves (slide 24) – you can guess which.

General merchandise, clothing, and fuel have been hit hard (FT suggests the latter two by -70%).

Staff has seen a massive spike in absence and they have had to recruit 45,000 people since 20th of March.

Scaling online has proven very difficult.

Additionally Tesco Bank will swing from £193m profit to a loss this fiscal year (due to bad debts and fall in income).

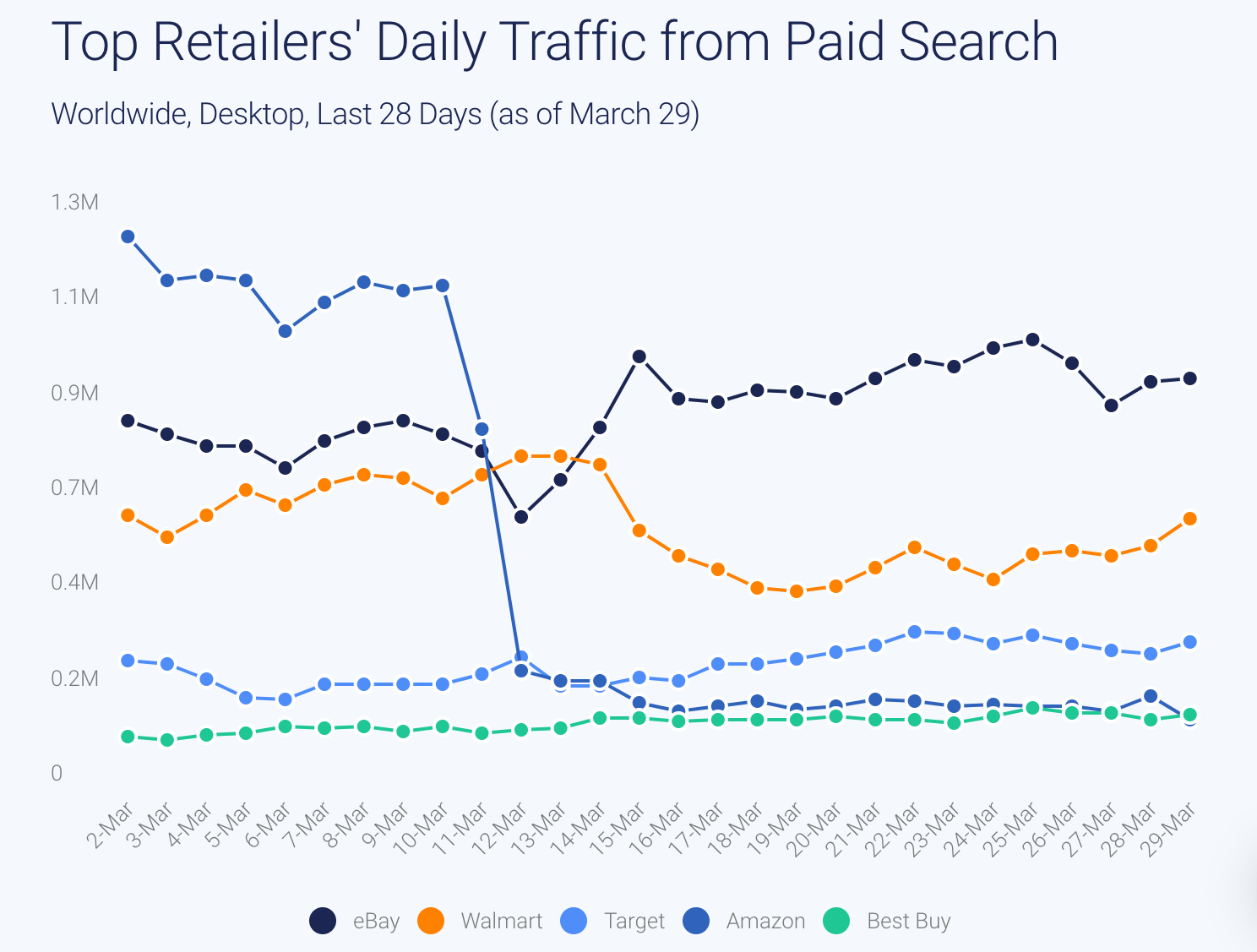

On 11th of March Amazon put a halt to almost all of its spending on Google Ads.

“Amazon seems to have completely removed itself from the competition for essential goods, effectively leaving one million daily visits on the table for other competitors to take.”

Paid search traffic to the site fell 90% almost immediately costing 11.2m visits.

Ebay has capitalised to a certain extent on this by bidding on high volume keywords – you guessed it – “toilet paper”, “n95 mask” and “hand sanitizer”.

Interesting data from Foursquare regarding foot traffic (up to 27th March) in the US.

As expected Airports -66%, Hotels -61%, Bars -60%, Gyms -64%, Malls -61%, Clothing Stores -72%, Movie Theatres -75%, Restaurants -73%.

There are some interesting observations though.

Despite restaurant traffic being down 73%, fast food is only -17% – likely due to take away.

Interestingly after the initial stocking spike traffic to supply stores, grocery stores (pictured) and liquor stores is now well down from the peak (but still up overall).

Drug stores on the other hand are seeing a +28% and hardware stores continue to see strong traffic (+27%).

Gas station traffic initially ticked up but are now seeing -7-8% decline.

Outdoors is booming with visits to trails +34% and parks +10%.

Under the radar the FDA has introduced a new regulatory pathway for insulin biosimilars (generic copies of biologic drugs).

“Today is a milestone for the future of insulin and other important treatments – potentially a new era of proposed biosimilar and interchangeable insulin products.”

This will increase competition.

Likely a big issue for the insulin oligopoly Sanofi, Novo Nordisk and Eli Lilly.

Blaming ratings agencies doesn’t exactly fill anyone with confidence.

Softbank put out this statement asking for Moody’s to withdraw rating due to “excessively pessimistic assumptions regarding the market environment and misunderstanding and speculation that SBG will quickly liquidate assets without any thorough consideration and without making improvements to its financial condition“

Really interesting Interview with the CEO of Drägerwerk, the world leader in the production of ventilators.

On car plants being repurposed to make ventilator components – “There is little point in adapting unused production capacity to manufacture respiratory aids. I spoke with Daimler over the weekend. They would also like to help. But it’s unfortunately not so simple. We can’t build cars either.

Repurposing devices – “There is a lot of potential there... I believe it’s possible to use devices from ambulance service or anaesthesiology departments. Such devices aren’t meant for long-term respiration, but they can serve that purpose.”

The real problem is lack of experts – “It’s not about the device, but about the person who is attached to it. You have to be able to evaluate the person’s state and know how to precisely adjust the device to first save the person’s life and then ensure that they quickly grow healthy again. This requires years of experience.”