It is interesting because it goes against a lot of consensus views.

(1) The demand boost is largely temporary (fiscal stimulus) and will start to subside e.g. consumer discretionary was actually up last year.

(2) Supply will eventually catch up (lumber production +20%, booming semiconductor exports Taiwan/Korea, lots of full container ships at US ports).

Inflation depends largely on the labour market and that still has considerable slack (U-6 rate is 11% vs. 8% pre-Covid, slide 79 Atlanta Fed Wage Tracker is benign).

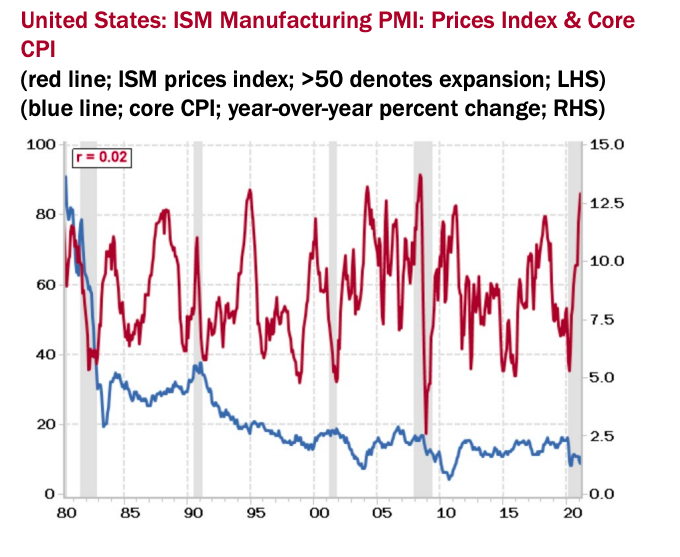

Things like commodities (China is delevering anyway) and ISM diffusion indices (see chart) don’t drive inflation.