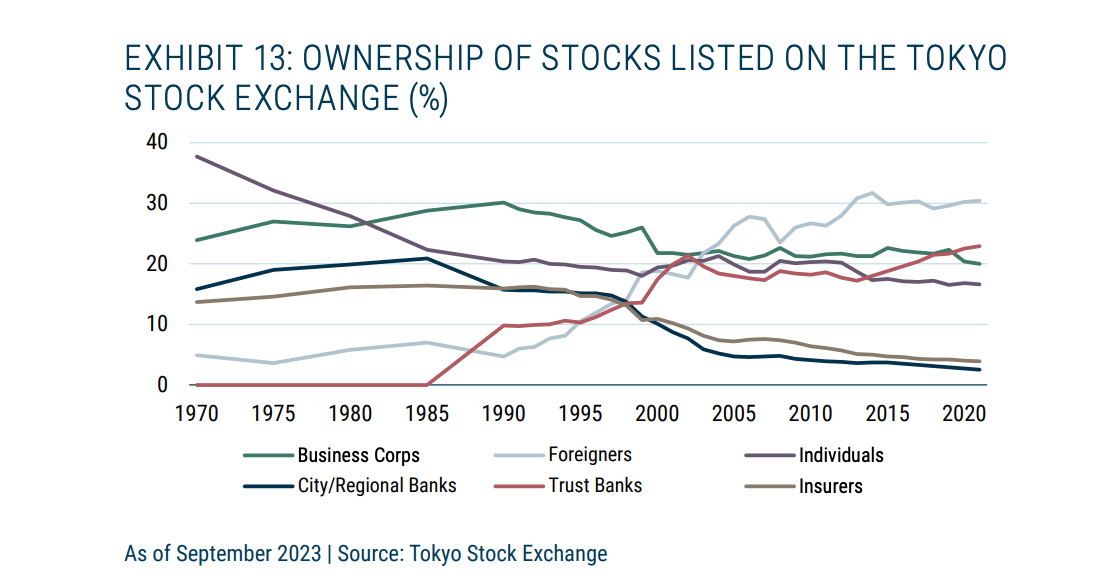

If you split it up into insiders (financial/corporate) and outsiders (everyone else), the former ownership peaked at 70% during the bubble years and has come down to 20%.

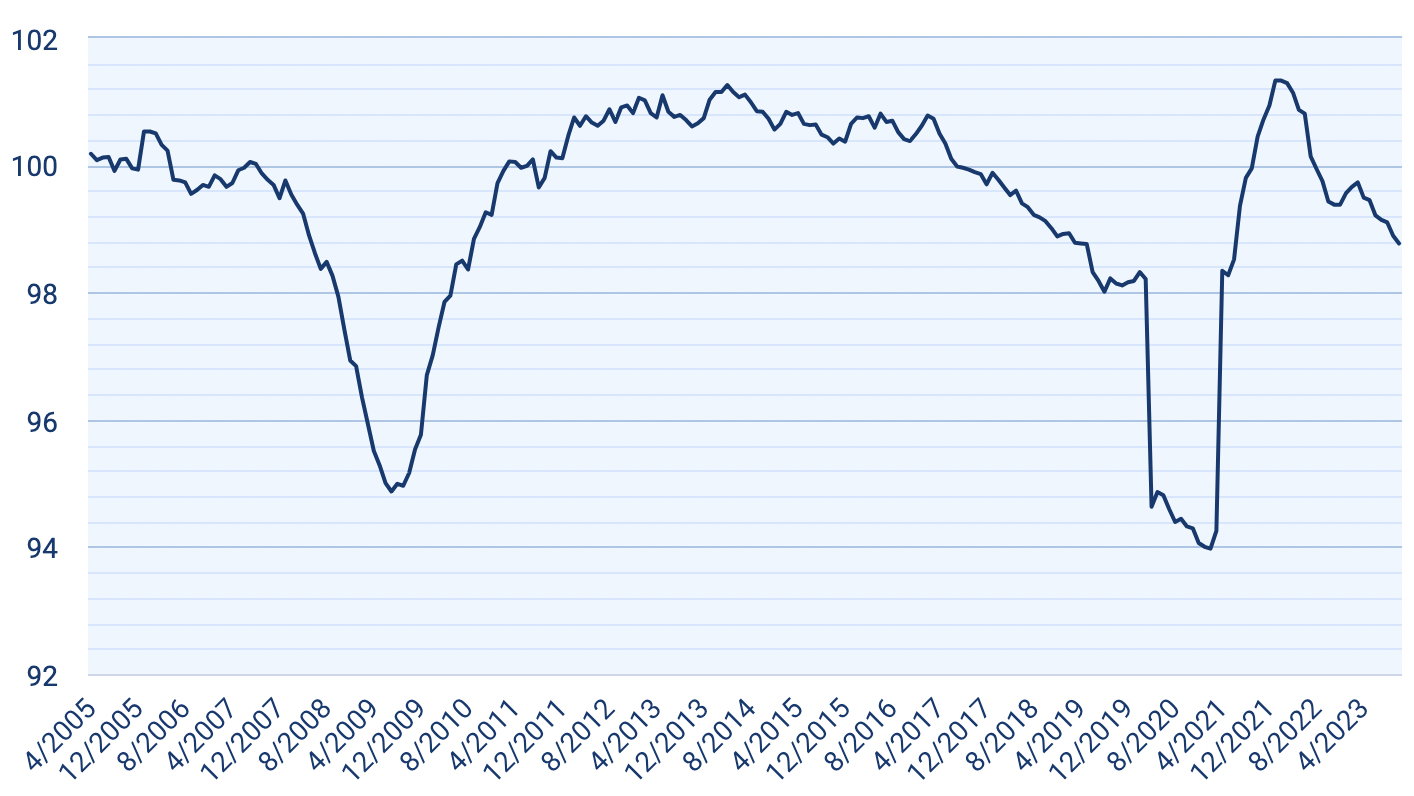

“The rate of small business job growth has slowed in 17 of the last 20 months, falling from the record high of 101.33 in February 2022 to 98.77 in October 2023.“

Bill Gurley’s September 2023 talk “2,851 Miles.” is a very interesting read on this very important topic in economics and investing.

As a rule, regulation is acquired by the industry and is designed and operated primarily for its benefit.” I like to say, “Regulation is the friend of the incumbent.”

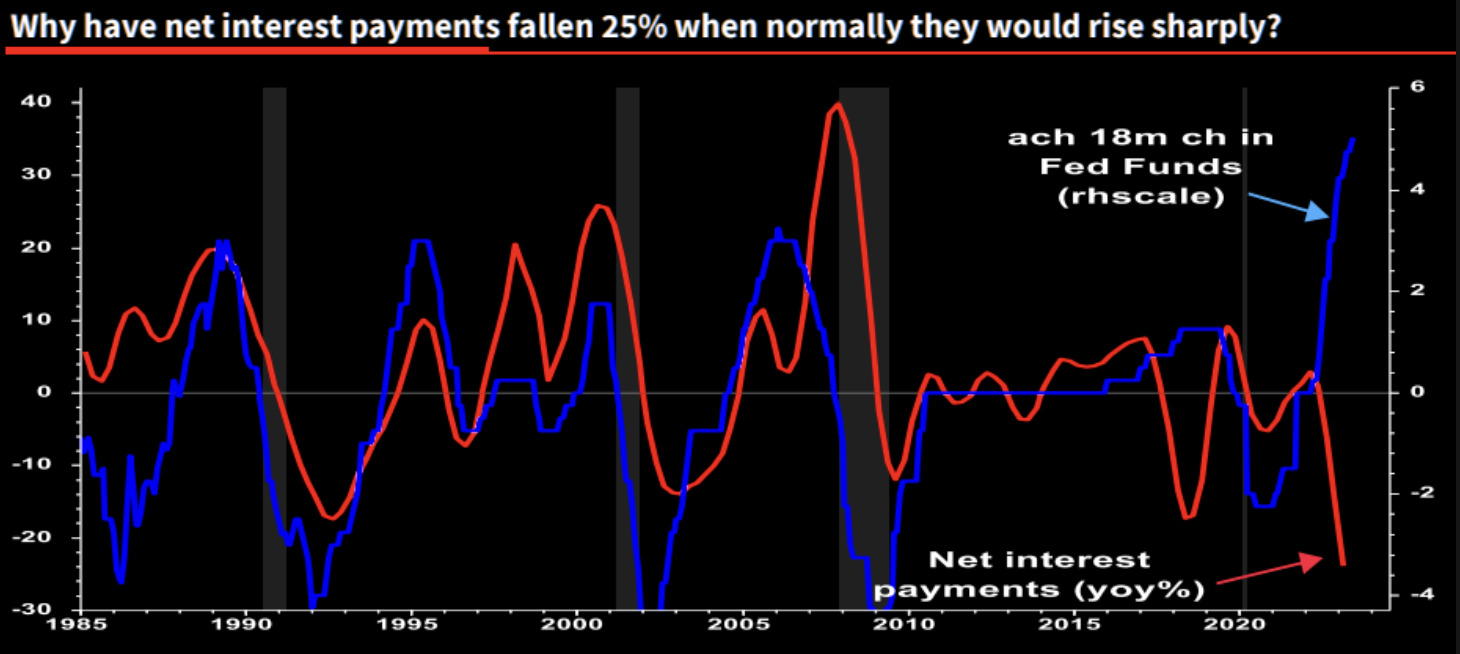

Despite the sharp rise in Fed Funds rate, company net interest payments have actually fallen.

“We have concluded that a sizeable proportion of huge, fixed-rate borrowings during 2020/21 still survives on company balance sheets in variable rate deposits. Companies have effectively played the yield curve in reverse and become net beneficiaries of higher rates, adding 5% to profits over the last year instead of deducting 10%+ from profits as usual.”