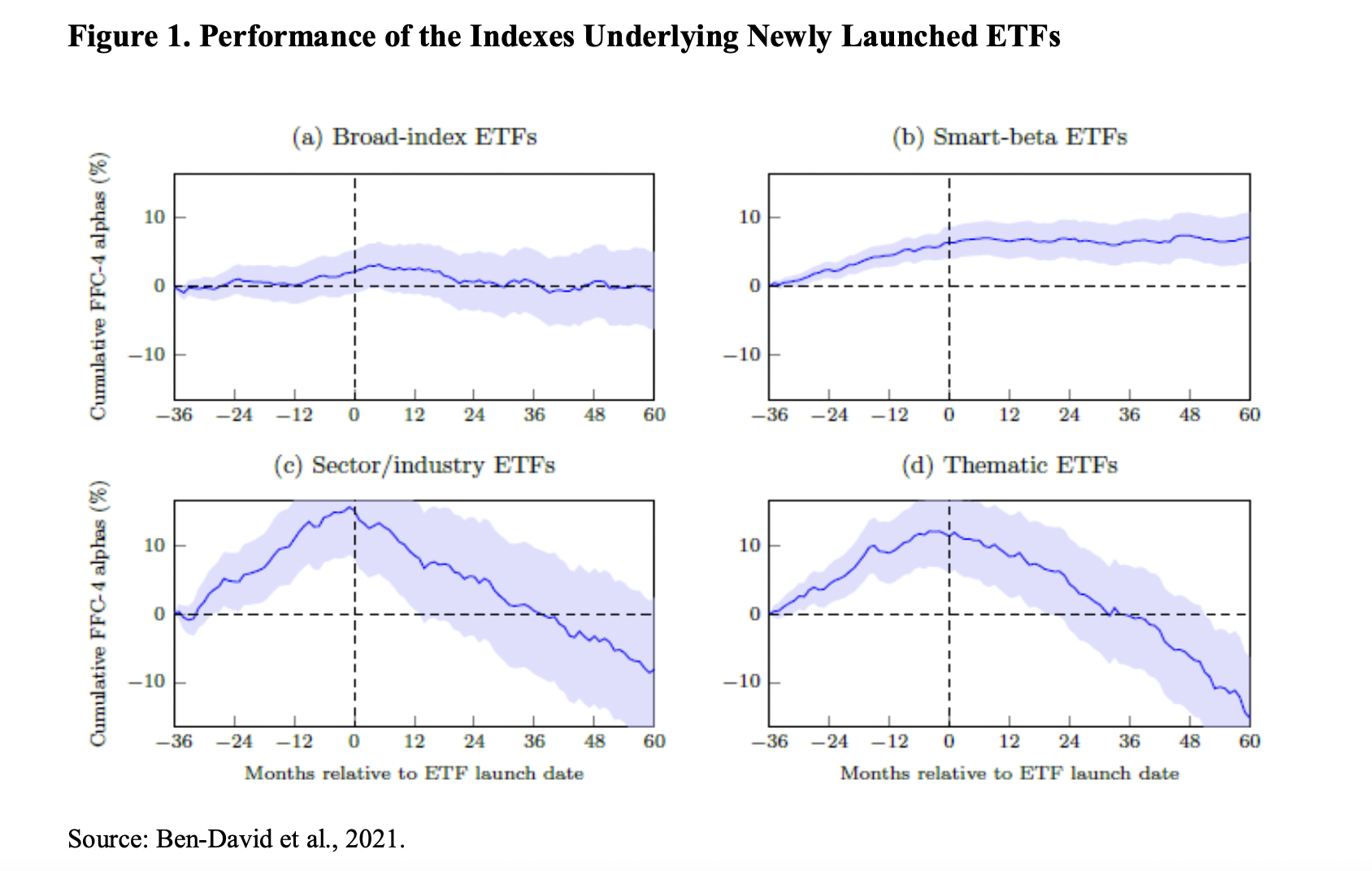

How did the model portfolios on which ETFs are built fare five years after launch when compared to three years before? measured relative to the benchmark selected by the managers themselves.

The results aren’t pretty.

Thematic strategies that added 3-5% a year pre-launch, lost 4-5% a year in the five years after.

It seems that hype in various areas, leads to a launch of ETFs which then don’t add any alpha.

So be careful when you invest in the next hot thing via ETF.

Note this is just the model portfolio performance (e.g. index) and NOT the ETF itself (though it should track very closely after costs).

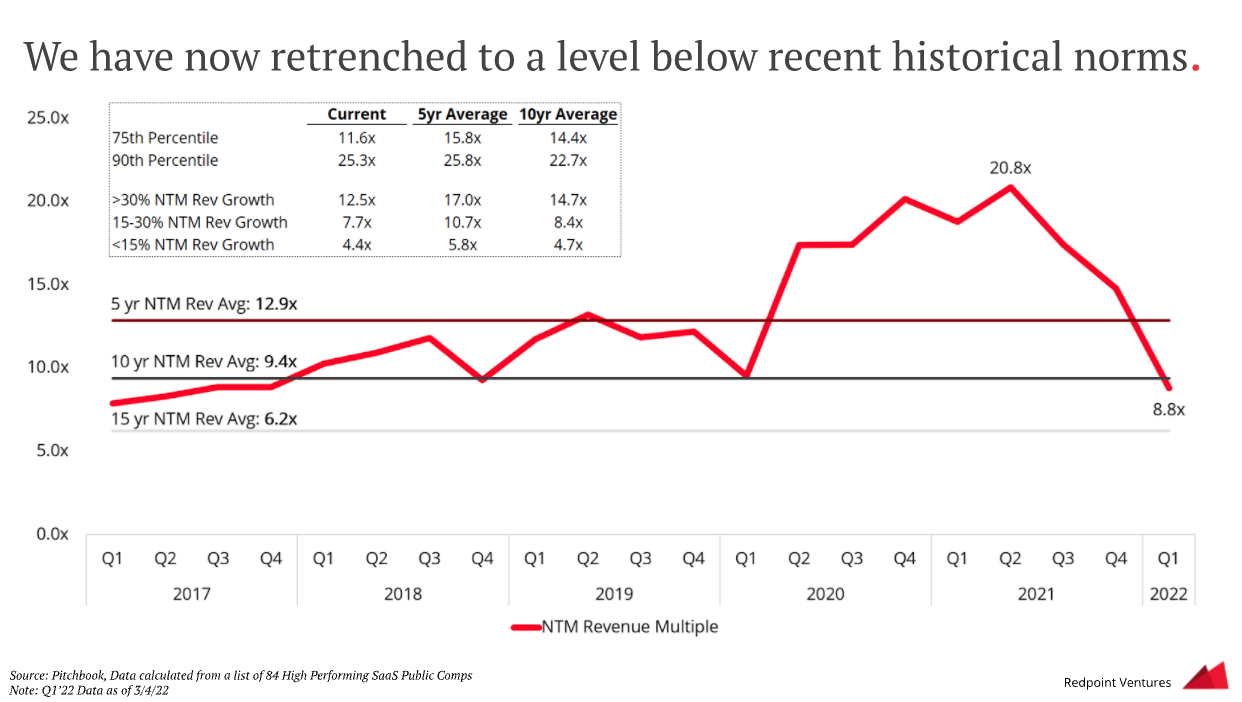

Thoughtful analysis of the venture landscape given the current state of public markets from Redpoint ventures.

The background is – public high performing SaaS firm valuations have fallen below their 10 year average now (see chart).

Past public market corrections led to 10 quarters of decline in venture dollars invested of varying severity. The great recession, for example, saw a 30% fall.

“Currently many companies in private markets (particularly at late stage) are in “price discover” mode in fundraises with everyone trying to figure out market price – rounds are taking longer to get done and “willingness to pay” spreads are wide“

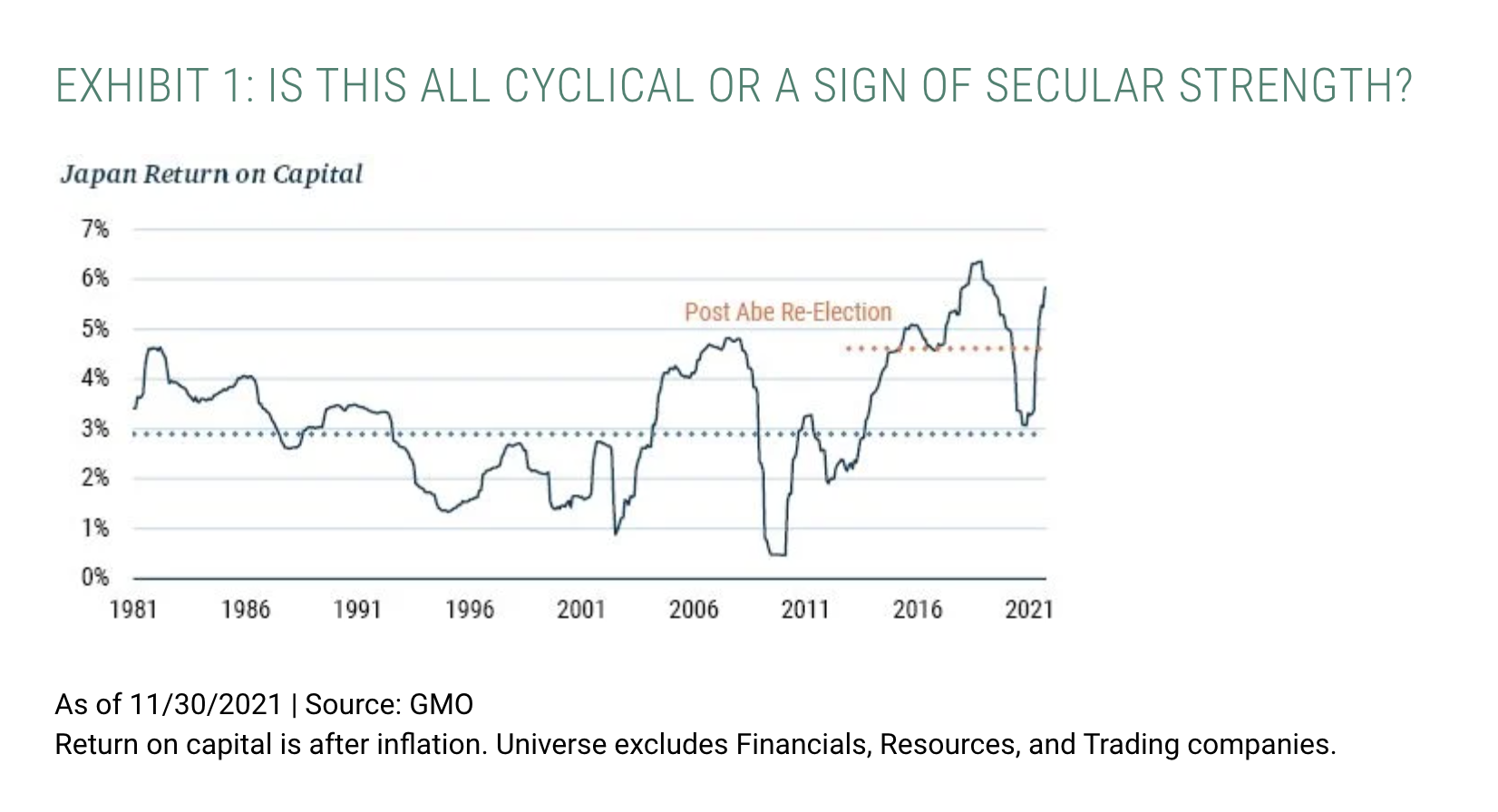

Japanese companies bloated their balance sheets with low-yielding cash and unproductive assets. This has meant that companies delivered just 3% return on capital compared to 6% fo the developed world for the majority of the past four decades.

Returns look to be improving according to GMO, the change is structural and not cyclical, and the result of improving margins and not improvement in inefficient balance sheets.

One of the coolest tools I have come across is Composer.

Composer is an automated trading platform that allows savvy investors, like readers of Snippet Finance, to easily build a portfolio of hedge fund-like strategies.

Instead of struggling to implement strategies yourself, Composer breaks the strategy creation process into building blocks that can be infinitely combined using a no-code visual editor.

Once you create a strategy and invest in it, Composer will automatically execute trades on your behalf based on the strategy’s logic.

If you’re not ready to create a strategy from scratch, you can choose from a collection of vetted ready-made strategies.

Composer makes the kinds of strategies that are used by top hedge funds as easy to access as individual stocks.

Investing in securities involves risks, including the risk of loss. Borrowing on margin can add to these risks. Composer Technologies Inc., SEC Registered RIA.Snippet Disclaimer.

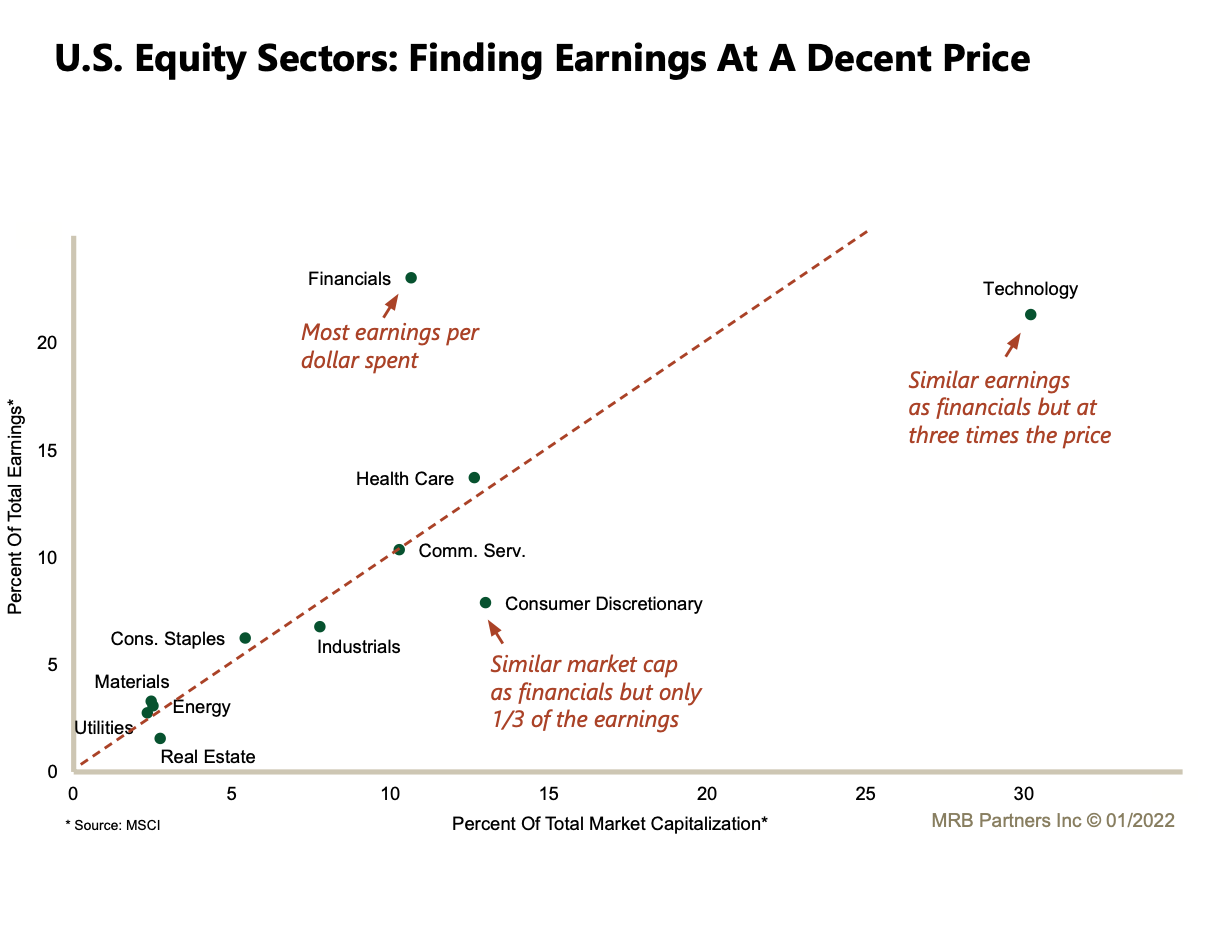

Useful chart from MRB plotting a sector’s percent share of total US market capitalisation on the x-axis and percent share of total market earnings on the y-axis.

It of course misses a lot of elements (e.g. growth of earnings, returns etc) but is still worth thinking about.