Always worth a flick through the latest presentation – titled Superman – from Jeffery Gundlach.

This is an interesting slide showing that twin deficits (current account and budget) lead the US Dollar exchange rate by 2 years – suggesting downward pressure on the latter.

Whereas Einhorn thinks that inflation is coming, Hoisington think this couldn’t be further from the truth (and hence think the yield curve will be anchored at zero).

“Recent articles have suggested that the Federal Reserve and the Department of the Treasury are engaged in Modern Monetary Theory (MMT) or some form of “helicopter money”, the famous Milton Friedman phrase also referred to by Ben Bernanke. The inference is that once the virus is contained, these new efforts will yield different and more powerful economic and inflation results than did the Quantitative Easing periods following the 2008-09 Global Financial Crisis (GFC). Further, the suggestion is that the fiscal policy actions taken this year totaling $2.7 trillion will be far more effective than the $2 trillion stimulus package of 2009. Are these assertions that MMT is in place and monetary and fiscal actions will spur economic and inflation rates higher true? The short answer is no.”

What follows is a rather technical economic theoretic description of what is going on.

It is worth getting one’s head around this. Especially understanding how quantitative easing leads to increased excess deposits by banks at the Fed and not borrowing (a decision that is independent) and hence economic impact.

Overall they are predicting deflation – grim reading indeed.

“One of the most influential things he [Buffet] said to me was if you want to be successful, all you need to do is look around the room and think about the classmate or classmates you most admire and what qualities they have and just decide to adopt those qualities. If you do that, your chances of being successful go up enormously.”

“I actually think that people will be that much more desperate for human connection after this experience than they were before.”

He is probably right on the last point – long human connection?

The fund is -21.5% in Q1 and down a futher -1.1% in April (despite the market rebound).

Interesting discussion of how, despite taking net from 74% to 15%, they still struggled with performance against a falling market.

Eninhorn’s value style is struggling in recent years and these markets. Despite this Greenlight is starting to market the fund again.

Letter includes interesting debate on inflation post-crisis, what to buy in that environment, his current holdings and shorts (incl TSLA), new positions. Always worth a read.

“On March 3, 2020, we disclosed that we had acquired large notional hedges …

“On March 23rd, we completed the exit of our hedges generating proceeds of $2.6 billion for the Pershing Square funds ($2.1 billion for PSH), compared with premiums paid and commissions totaling $27 million, which offset the mark-to-market losses in our equity portfolio. Our hedges were in the form of purchases of credit protection on various global investment grade and high yield credit indices. Because we were able to purchase these instruments at near-all-time tight levels of credit spreads, the risk of loss from this investment was minimal at the time of purchase.”

“We have redeployed substantially all of the net proceeds from our hedges by adding to our investments in Agilent, Berkshire Hathaway, Hilton, Lowe’s, and Restaurant Brands. We have also purchased several new investments including reestablishing our investment in Starbucks which we sold in January. The proceeds of the hedges have enabled us to become a substantially larger shareholder of a number of our portfolio companies, and to add some new investments, all at deeply discounted prices. Even after these additional investments, we maintain a cash position of about 17% of the portfolio. “

A bit off topic for Snippet but these guiding principles from Jim Simons, the founder of one of the most successful funds ever – Renaissance Technologies, are worth a quick absorb.

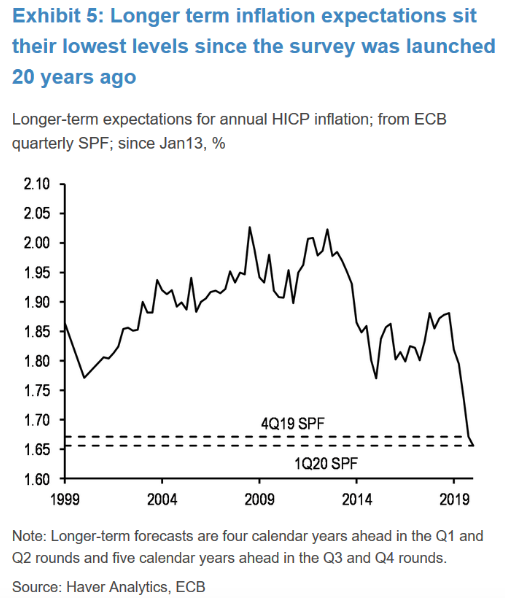

Chart from Haver Analytics supports their arguments on subdued inflation.

These five factors – loss of momentum, monetary restraint, high debt levels, flat profits and excess capacity – will bring about slower growth and continue to subdue core inflation.

Over the past 65 years, yields on long dated risk-free U.S. treasury securities moved in the same direction as core inflation on an annual basis roughly 80% of the time. We believe that there is a high probability that this relationship will hold in 2020 as inflationary pressures continue to subside.