These 16 companies dominate Google search results. Odds are you haven’t heard of any of them.

“Across 10,000 terms where affiliates are ranking, which cover products in every niche you can think of (home, beauty, tech, automotive, cooking, travel, sports, education and many more), these 16 companies ranked on the first page of 8,574 (or 85%) of them.“

Interesting analysis on staying competitive in semiconductor manufacturing.

“The dotted black lines toward the bottom show the estimated cost of building a leading edge fab (the lower line) and a line showing double that number (the upper line). Our thesis is that companies whose annual revenue fall between those two lines are at risk of falling off the Moore’s Law treadmill.“

TSMC came close once. Samsung looks close now (though this doesn’t include the rest of the group subsidising the fab). It also shows that Intel’s plans to offer fab services need to succeed.

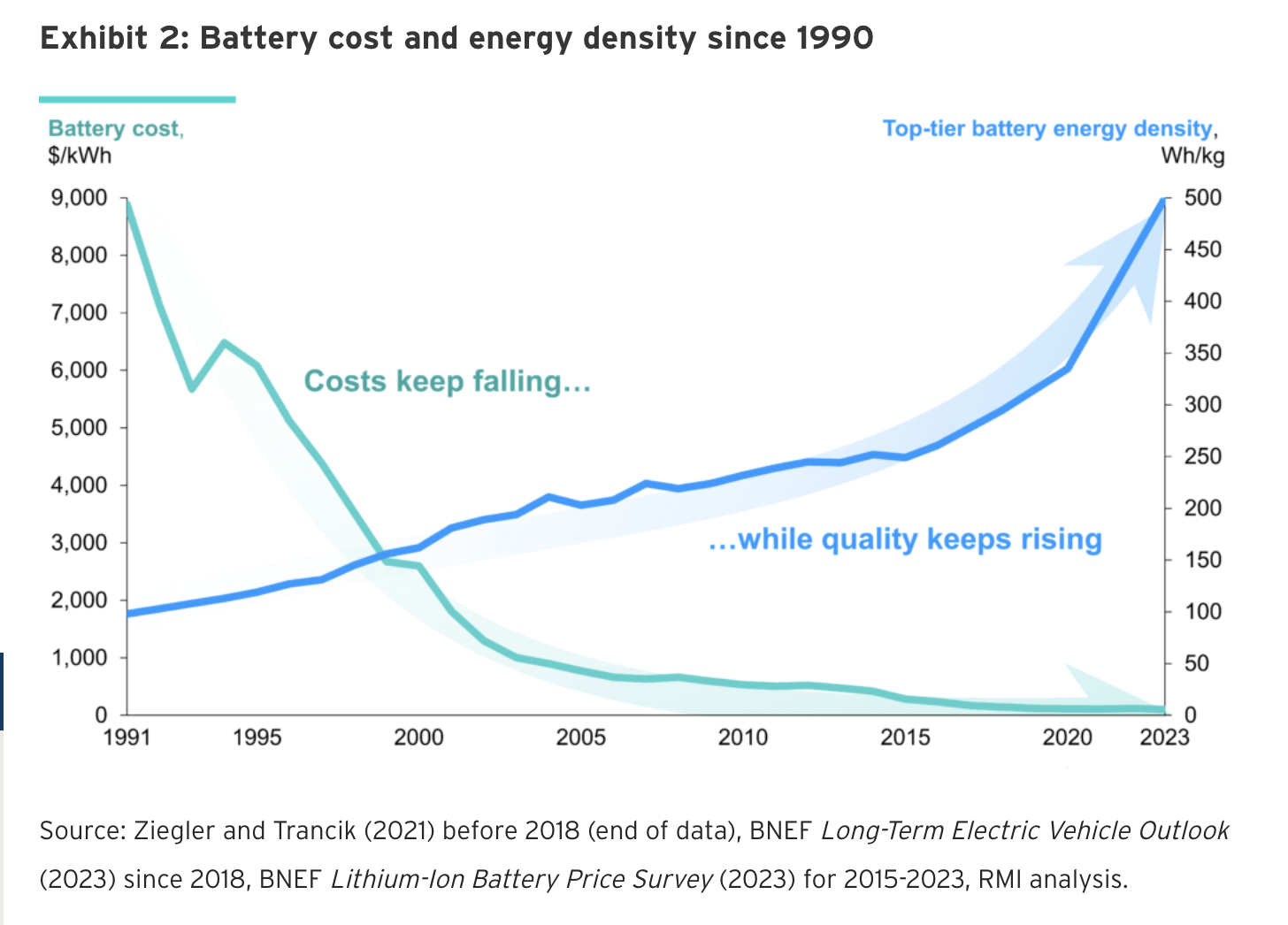

“Over the past 30 years, battery costs have fallen by a dramatic 99 percent; meanwhile, the density [a key measure of quality] of top-tier cells has risen fivefold.”

Interesting corollary from Ben Evan’s “the most interesting thing is a new Google feature called ‘circle to search’. You can use your finger to draw a circle around anything on your Android phone screen, in any app, and Google will do a text or image search. So, you can circle a hat in a Tiktok and Google will tell you where to buy it. It occurred to me a while ago that screenshots are the native file format of smartphones, but they lose context. But what if the OS knows what’s on the screen, in every app? Screen-scraping is the new API…”

A very good history of Y Combinator and how Paul Graham, through his essays and otherwise, had a huge part to play in building the cult of the founder.

This history is trapped inside a not-so-convincing argument of YC’s demise.

Excellent interview with Herbert Hovenkamp professor at Penn Law School specializing in US anti-trust on what he thinks of the big cases against Big Tech in the US.

Worth a read for any holders of AAPL, META, GOOG, AMZN.

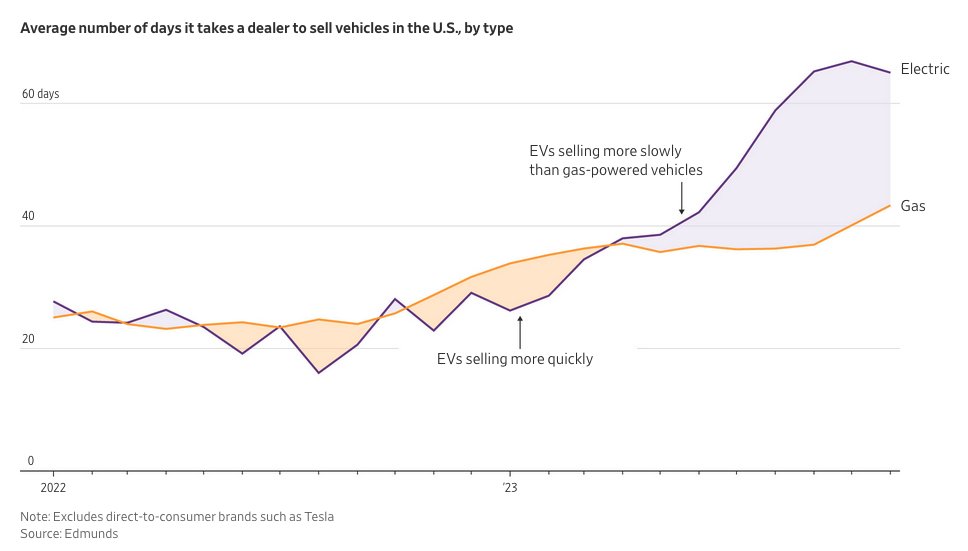

Something not so good is going on in EV land – and it isn’t aggressive Chinese competition.

Hertz for one has decided to dump 20,000 EVs citing hidden costs, especially of accidents.

“Expenses related to collision and damage, primarily associated with EVs, remained high in the quarter, thereby supporting the Company’s decision to initiate the material reduction in the EV fleet.“

Then there is this chart showing EVs are taking longer to sell.

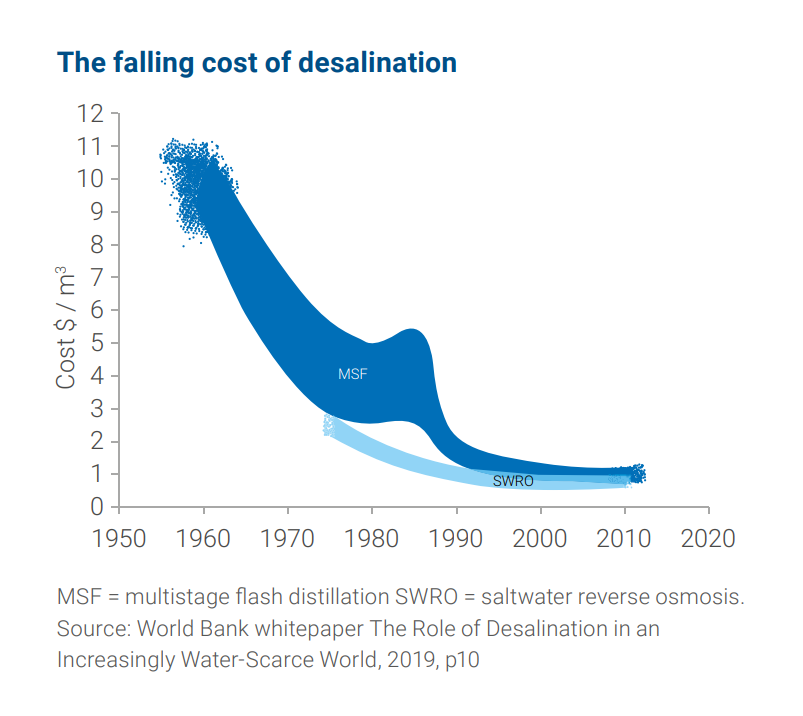

“The chart shows how the cost of desalination has fallen over the long term. This has been driven by technological advances, larger plants translating into greater economies of scale, and project development choices such as colocation of desalination plants with power plants.“

“In over 3.8 million miles driven without a human being behind the steering wheel in rider-only mode, the Waymo Driver (Waymo’s fully autonomous driving technology) incurred zero bodily injury claims in comparison with the human driver baseline of 1.11 claims per million miles. The Waymo Driver also significantly reduced property damage claims to 0.78 claims per million miles in comparison with the human driver baseline of 3.26 claims per million miles.“

The latest 2023 report is worth a flick (all 160 slides).

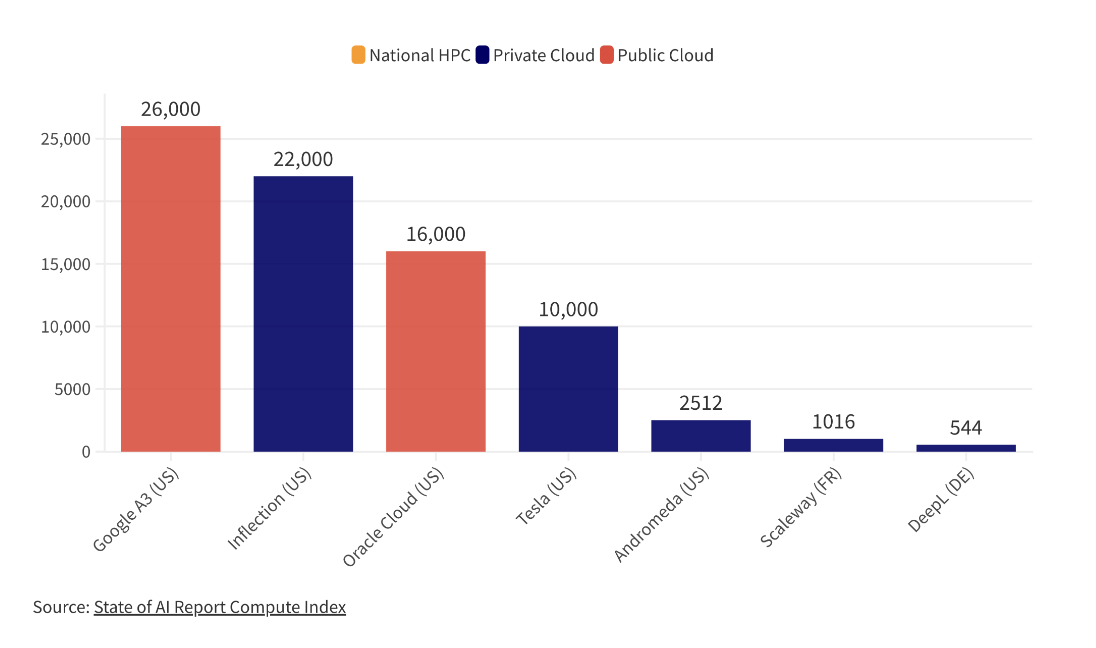

This graph, for example, shows the largest Nvidia H100 chip clusters – interesting to see TSLA there, who also run the 4th largest A100 cluster in the world.

Or see Slide 76 which suggests that Nvidia’s advantage (the use of its chips in academic papers) continues to increase.

Fascinating history of how we all ended up doing PowerPoint slides all the time.

The creator of PowerPoint also has a colourful story – “It’s hard now to imagine deafening applause for a PowerPoint—almost as hard as it is to imagine anyone but Bob Gaskins standing at this particular lectern, ushering in the PowerPoint age. Presentations are in his blood. His father ran an A/V company, and family vacations usually included a trip to the Eastman Kodak factory. During his graduate studies at Berkeley, he tinkered with machine translation and coded computer-generated haiku. He ran away to Silicon Valley to find his fortune before he could finalize his triple PhDs in English, linguistics, and computer science, but he brought with him a deep appreciation for the humanities, staffing his team with like-minded polyglots, including a disproportionately large number of women in technical roles. Because Gaskins ensured that his offices—the only Microsoft division, at the time, in Silicon Valley—housed a museum-worthy art collection, PowerPoint’s architects spent their days among works by Frank Stella, Richard Diebenkorn, and Robert Motherwell.”