In the spirit of Feynman this superb blog post, by none other than Stephen Wolfram, gives a lucid explanation of what is going on under the hood of the latest tech phenomenon.

The short answer is “it’s maths”.

“But in the end, the remarkable thing is that all these operations—individually as simple as they are—can somehow together manage to do such a good “human-like” job of generating text. It has to be emphasized again that (at least so far as we know) there’s no “ultimate theoretical reason” why anything like this should work. And in fact, as we’ll discuss, I think we have to view this as a—potentially surprising—scientific discovery: that somehow in a neural net like ChatGPT’s it’s possible to capture the essence of what human brains manage to do in generating language.”

The argument that AI is unlikely to be a winner for the middle-ground companies.

Why? “was a feature not a product” – in other words value will either accrue to core AI platforms (e.g. Open AI) or to incumbent software tools with distribution who will just add AI features.

“Adobe will own the AI-based image editing market Office & Google Docs will own the AI-based writing market Salesforce will be the best AI-enabled CRM Shopify the best AI optimization and customer support Zoom the best AI meeting summaries … all with a few API calls“

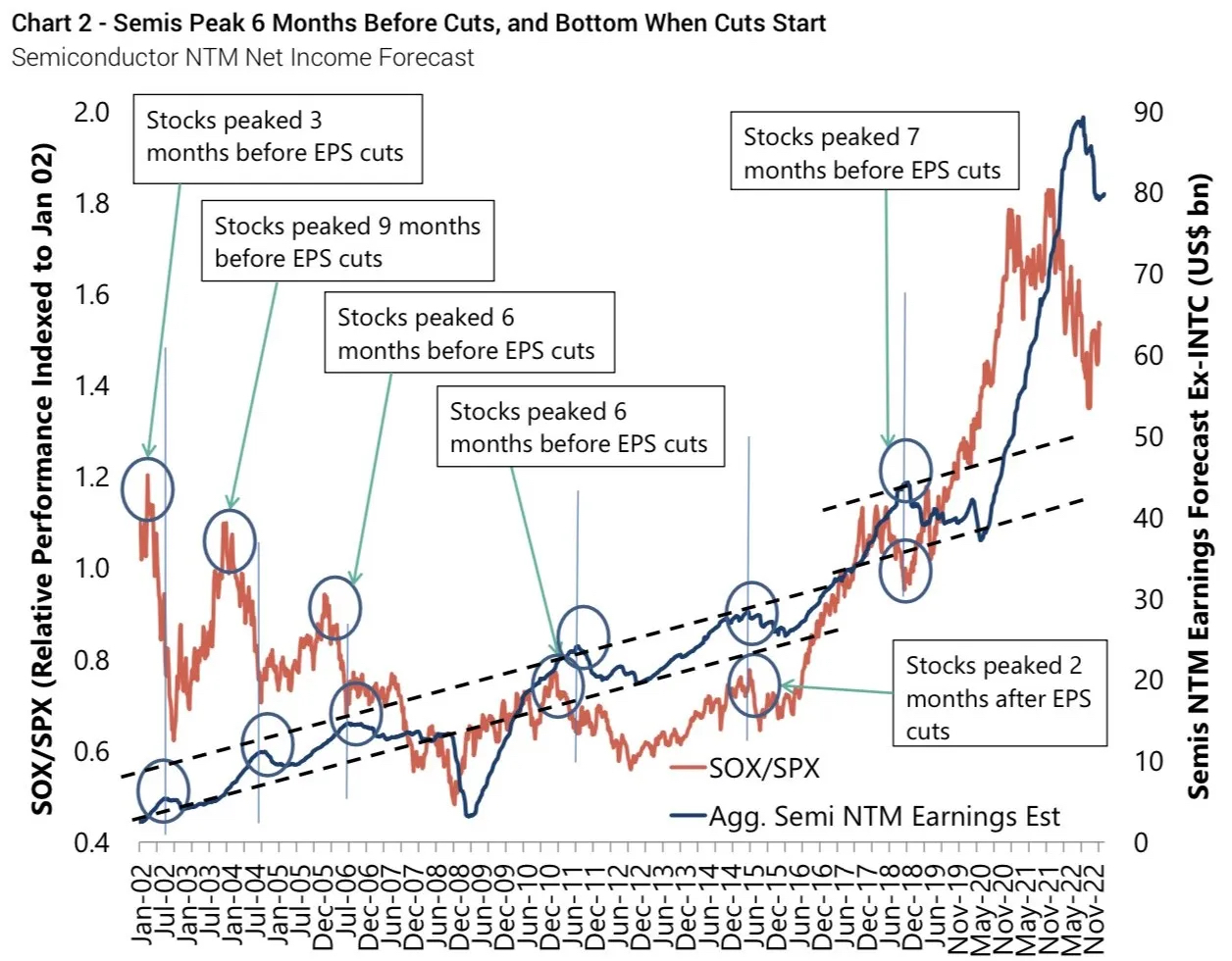

“The most intriguing aspect of Wall Street’s behavior is that if we examine every period of industry decline over the past several decades, we see that stock prices reach their lowest point when the industry only starts to experience a fall in earnings, well before the trough of earnings. The stocks were already recovering and surging by the time layoffs and consolidation occurred.“

Semiconductor index (SOX) is up strongly since October lows and earnings cuts have only just started i.e. a typical pattern with the expected bottom of the cycle is Q2 2023.

Yet, as argued here, this cycle appears different – (1) days of inventory at record high which will take, despite a desire for supply chain resilience, more than two quarters to clear (2) there is an oversupply of certain process tech (3) channel stuffing has been a big feature.

A harsh, almost damning, write-up of Intel, pre-dating the dividend cut.

“In reality, Intel is not the giant of the industry. Intel’s total share of industry capacity is around 10%, they are not a giant who has stumbled, they are a niche player and have been for years.“

RISC-V, the royalty-free open-source instruction set architecture, is worth keeping an eye on especially as Arm convulses its way back to the stock market.

The December 2022 summit (and this great write-up) offered a deep feel of the status of RISC-V.

Bold statements abounded – “It’s really important that you get this. RISC-V is inevitable. RISC-V is going to have the best processors. And RISC-V is going to have the best ecosystem.”

“Direct-to-consumer brands moved 20–30% of their marketing dollars in Q4 2022 from Meta to Amazon due to the former’s declining performance metrics for ads. The shift occurred despite a recent reluctance from DTC brand to sell products on Amazon because of limited access to and ownership of sales and customer data—but now that brands are receiving only $2 back for every $1 spent on Meta ads (they used to get $8 back), they are more willing to work with the e-commerce giant. According to Advantage Unified Commerce, an estimated 75% of brands report customer acquisition is cheaper on Amazon than other media channels.”

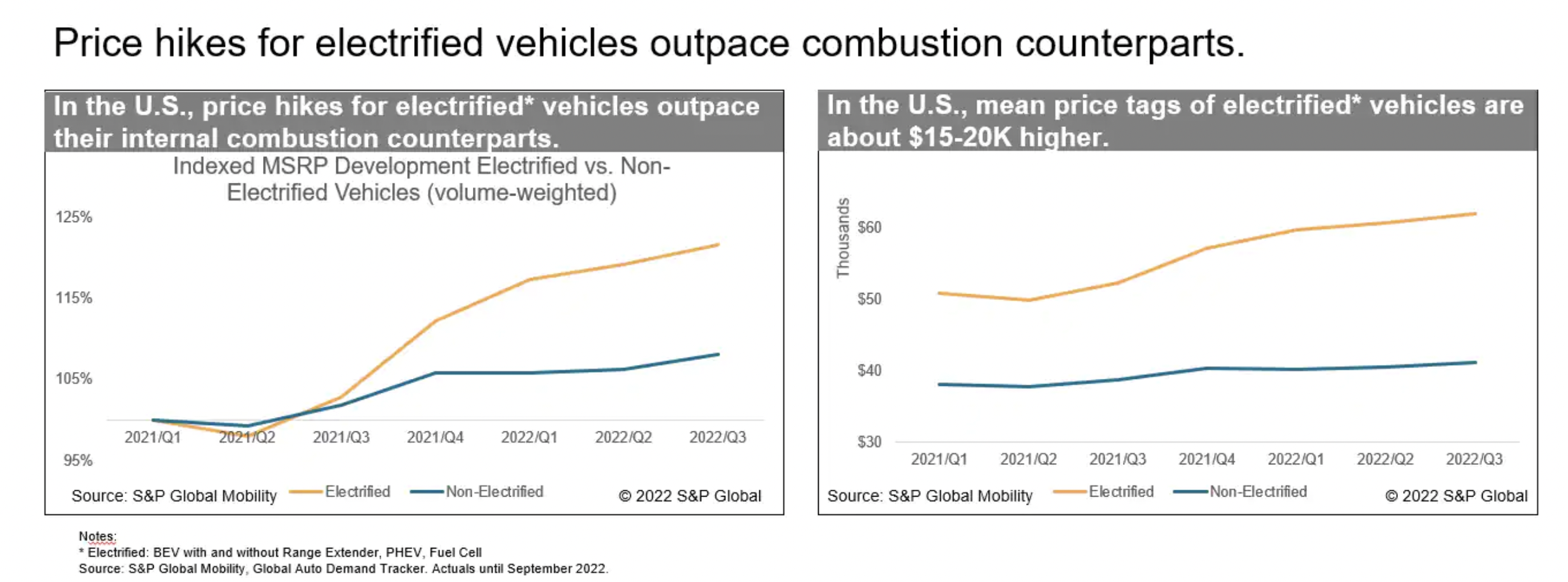

“Since about 2021-Q4, prices for electrified vehicles significantly outpaced their internal combustion counterparts, largely owing to battery material prices.“

These vehicles are “on average about $15-20K higher than their internal combustion counterparts.“

This is probably the opposite of what one expects to see for a new technology – but TCO considerations still drive most purchase decisions.

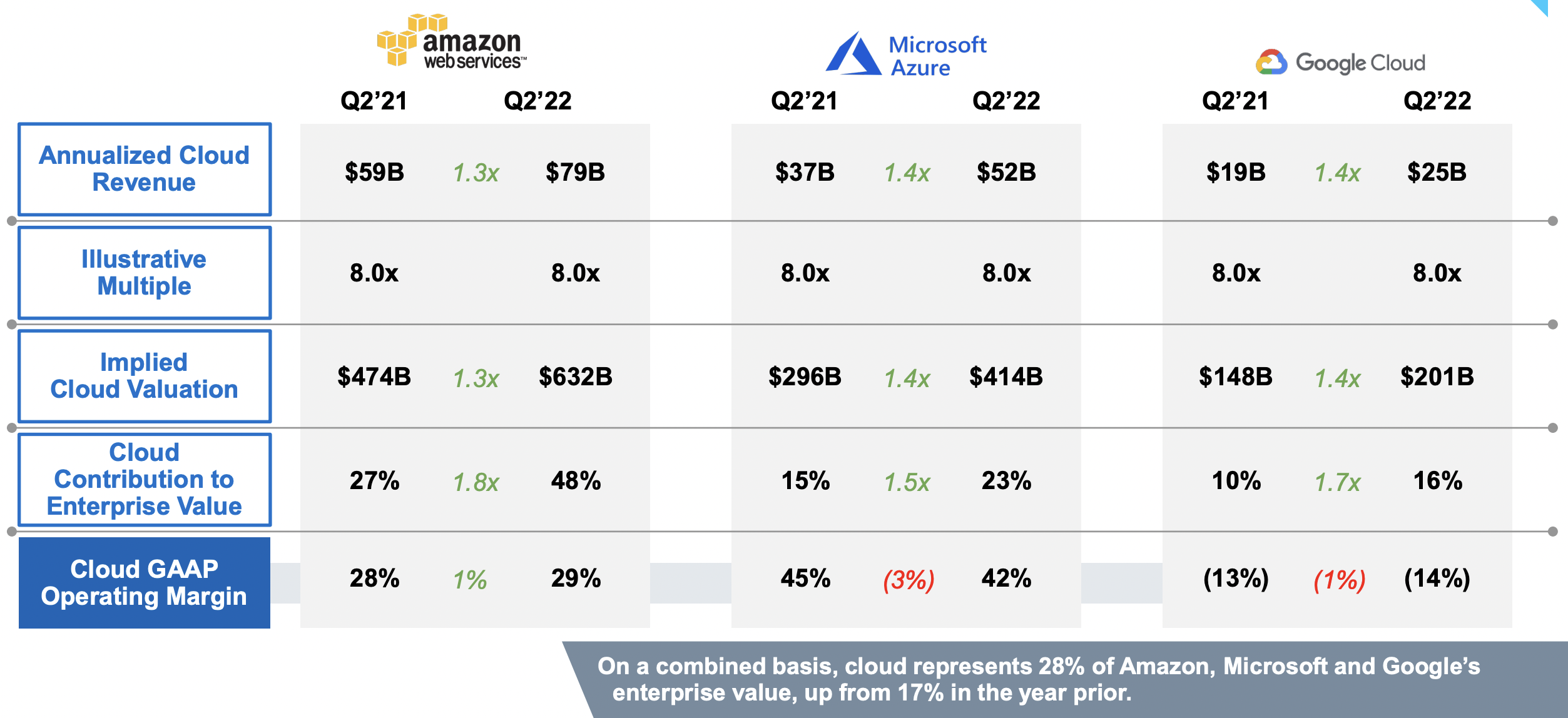

Cloud Vendor market was $159bn annual run-rate market in Q2, still growing 37% (though slowing).

This growth has actually come with pretty good economics. (From this Battery VC deck).

One very interesting feature of these vendors is they also happen to run huge cloud based products (think Xbox for example) which means they are customers of their own infrastructure – utilising it and making it better.

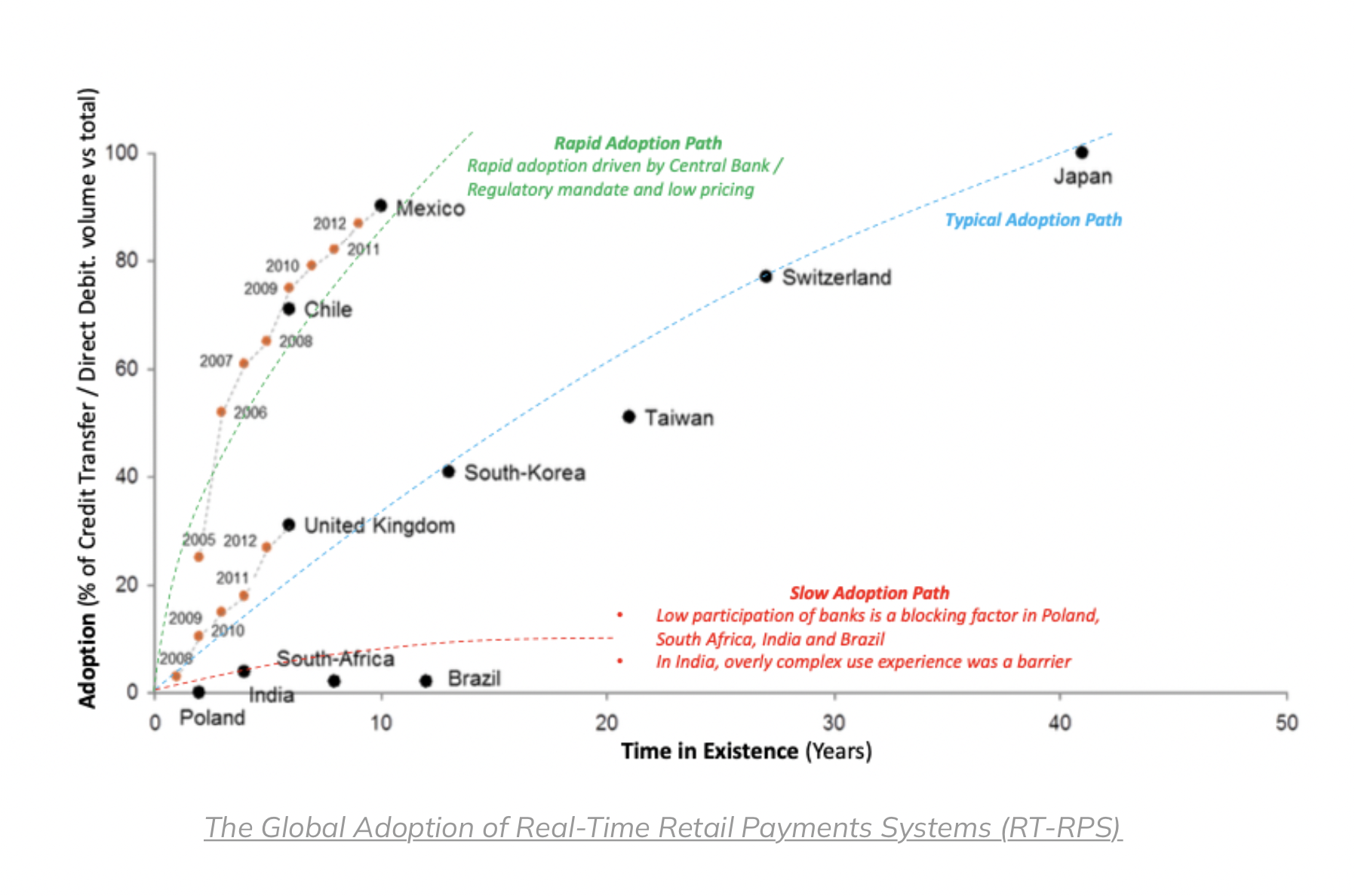

FedNow, a faster payments network designed by the Federal Reserve, is nearing launch in 2023 and this is a great explainer/history post.

The US lags far behind the rest of the world in faster payments.

FedNow could change that (or not) – it for one is cheaper than existing competitors.

There is also this chart, showing adoption rates of faster payment systems around the world – those that launched recently had faster adoption (especially if helped along by regulators).

One answer is funding – “The reason we don’t have fusion already is because we, as a civilization, never decided that it was a priority. Fusion funding is literally peanuts: In 2016, the US spent twice as much on peanut subsidies as on fusion research.“

“The future of semis will be designing ever more specific chips for ever more specific uses. This change will take many years to play out, but the transition has already begun. This is going to upend the semis industry to the same degree that consolidation over the past 20 years has.“

Few contrarian buyers out there, and for many startups there is plenty of cash in the bank.

“In 2021, there were more than 3,000 M&A deals globally involving a VC-backed company getting bought, according to Crunchbase. Halfway through the third quarter of this year, just under 1,600 startups have found a mate in the market.“

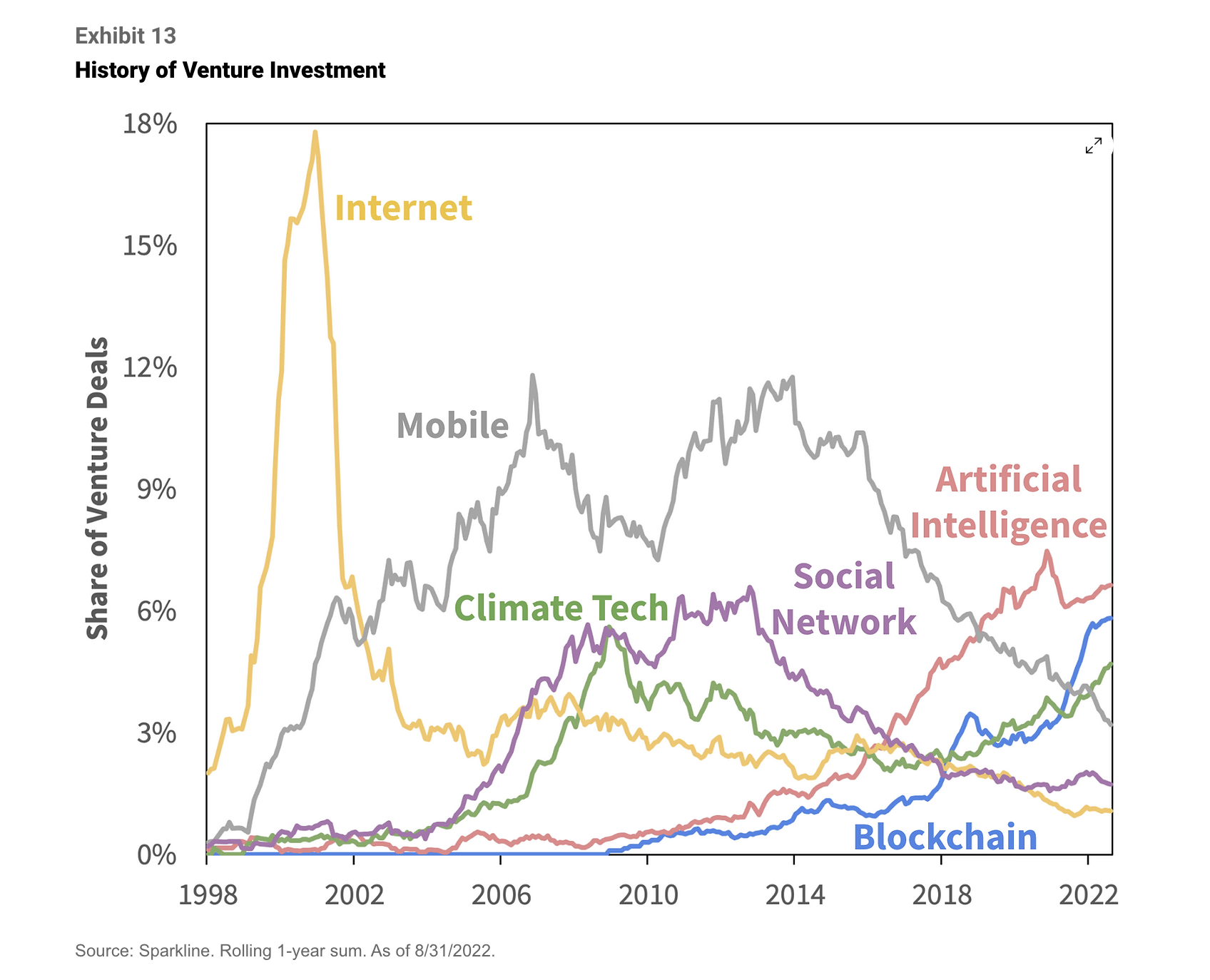

Using a machine learning model Sparkline Capital were able to cluster firms in similar technologies and then look at how venture investment in these tech clusters evolved over time.

This leads to the following chart of cycles.

“In the dot-com bubble, venture capital firms threw money at internet companies. Next, Blackberry and iPhone ushered in the mobile age. Then, Facebook’s success sparked a wave of investment into social networks. Artificial intelligence grew steadily over the past decade, while blockchain burst on the scene a few years ago. Climate tech investment faded after an initial burst but is now seeing a resurgence.“

Interesting first hand account of how Monzo grew from nothing to 1 million users in three short years.

Tom credits – a great product (compared to competition) that was a delight to use, a brightly coloured card, and network effects – “if you had 3+ friends on Monzo when you joined, you had a 70% chance of being a WAU [weekly active user] by day 90, versus only a 50% chance if you didn’t have any friends on the platform.“

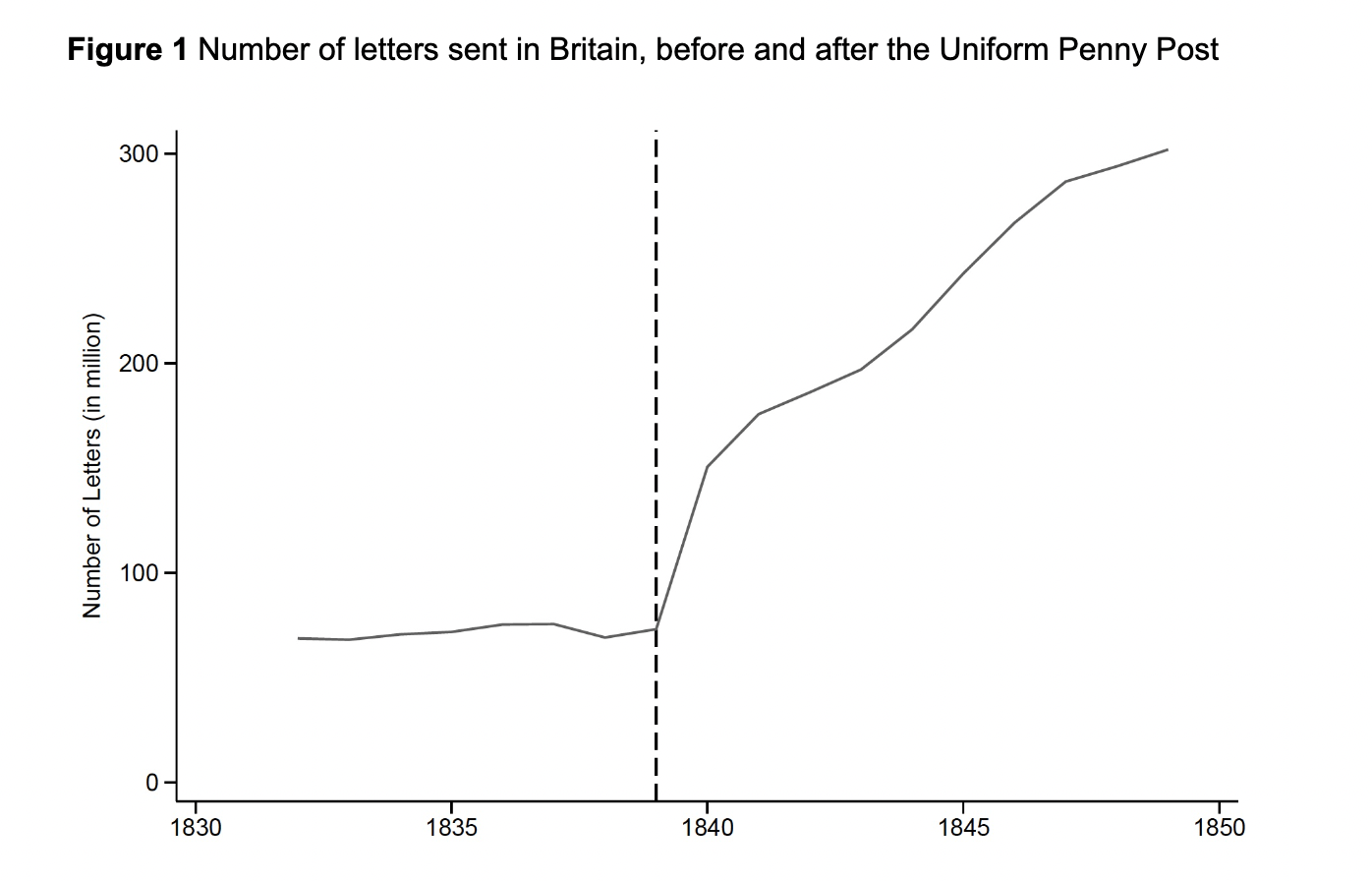

Meet one of the most dramatic changes in communication costs in history.

The introduction of the first modern postal system in Britain in 1840.

A 1839 Act of Parliament created the Uniform Penny Post – a single low postage rate and the first adhesive postage stamp, replacing a complex distance based system.

The results were monumental and, as this paper finds, also improved innovation.

Today, 73% of people in the UK consider post as essential or fairly important.