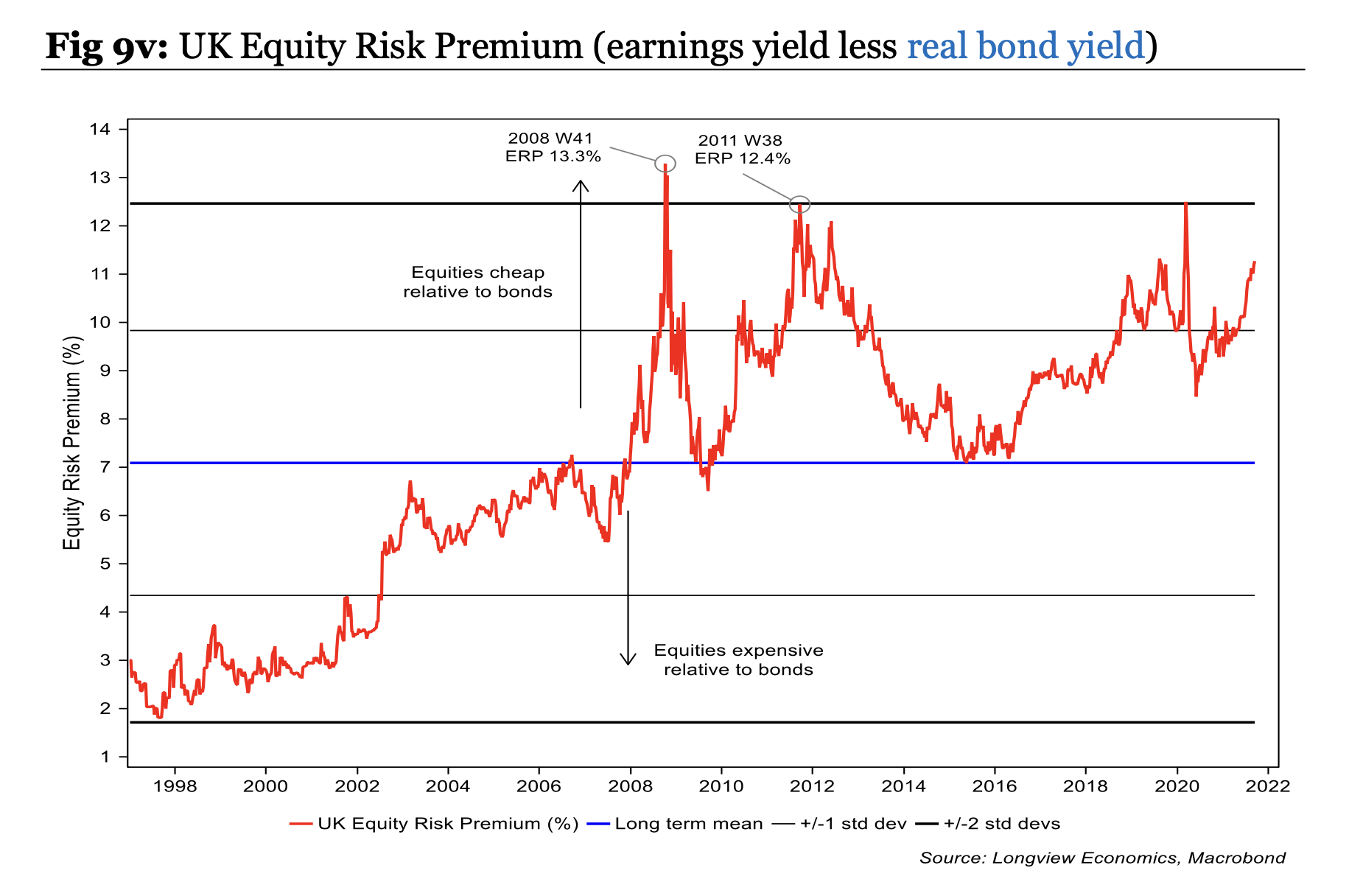

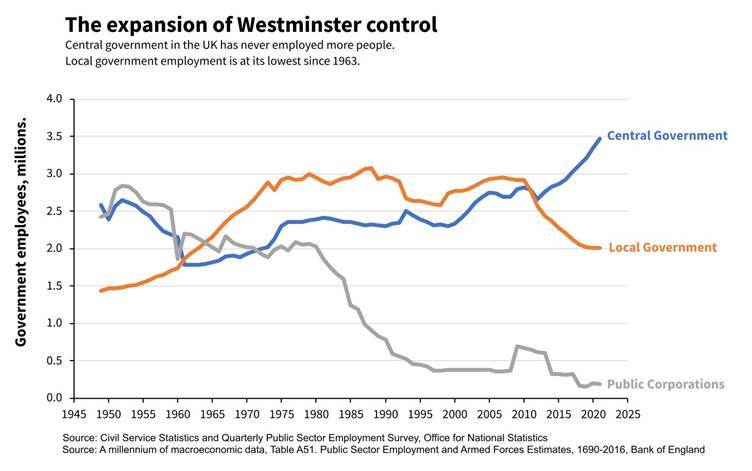

Since the financial crisis the number of people employed in local government in the UK has been declining and currently stands at the lowest level since 1963.

In contrast, central government employment is at a record high.

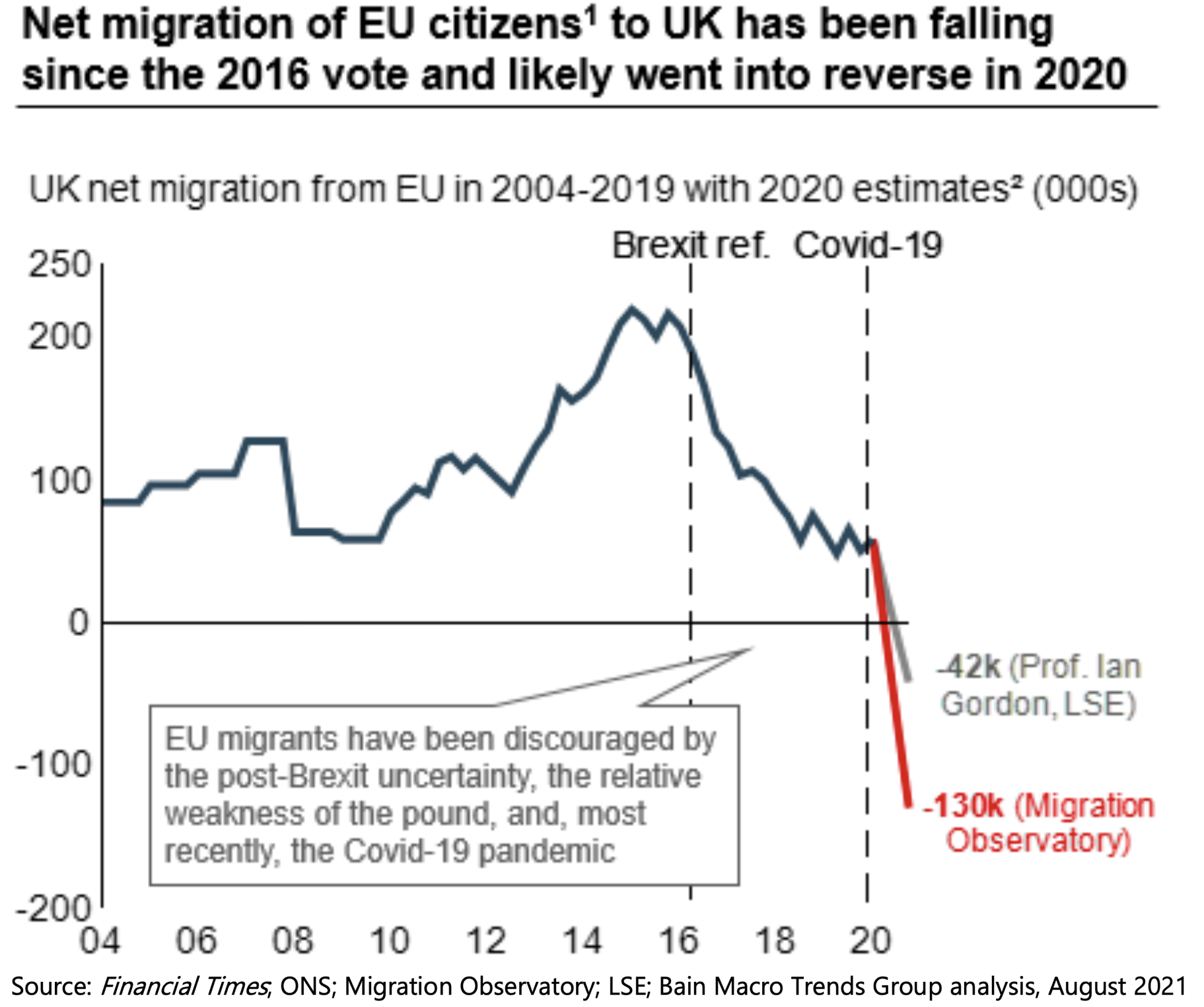

Since 2016 net migration from the EU to the UK has fallen.

The pandemic has likely pushed it into negative territory.

Certain sectors – like hospitality, transport, manufacturing, administration and construction – will be hit the hardest as they rely on EU labour for 10-15% of their work force.

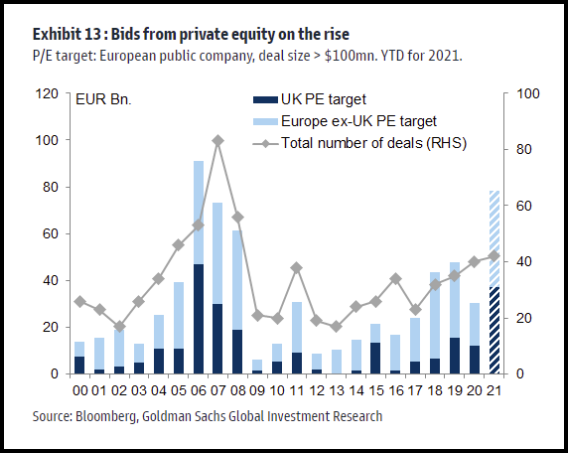

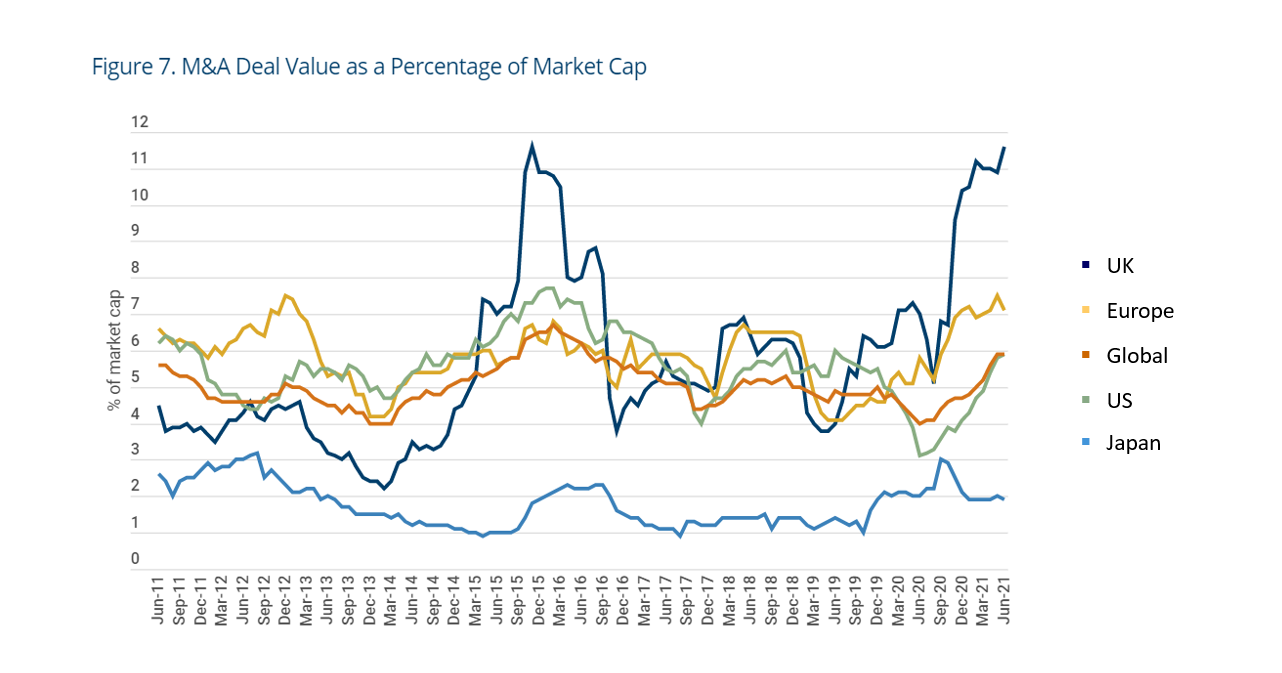

Mergers and acquisitions (M&A) activity has spiked to 12% of market cap in the UK, double the global average.

This is driven by cheapness of UK listed firms, stabilisation post Brexit, and record private equity dry powder.

Interestingly this spike is driven by a larger number of deals (25) when compared to the previous spike in 2015 (where mega deals for SAB Miller and BG Group dominated).

Comprehensive report with loads of stats on “whatpeople in the UK are doing online, how they are served by online content providers and platforms, and their experiences of using the internet, alongside business models and industry trends.“

71% of all online time is spent on mobiles now, yet half of over 75 year olds don’t use the internet at all.

39% of online time by adults was spent on Google or Facebook owned sites, and these two control 79% of UK online ad revenue.

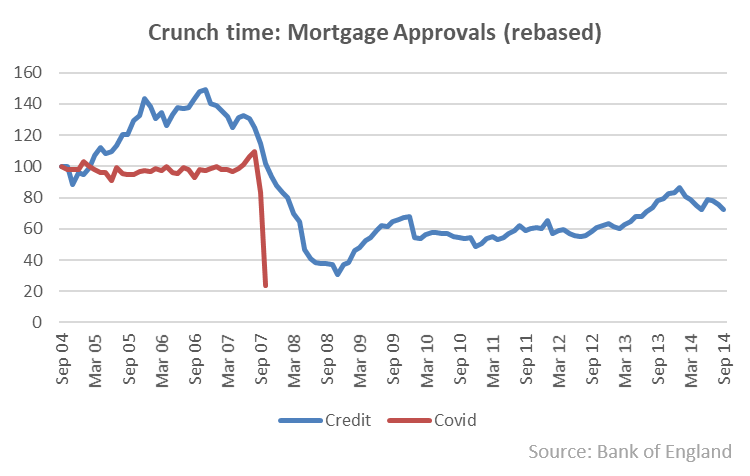

A data rich post about UK housing with some gloomy predictions.

Pictured is a chart of mortgage approvals – in blue since the three years leading up to the financial crisis and red since the three years before lockdown.

Mortgage approvals are “the leading indicator” for housing transactions and it does not bode well.

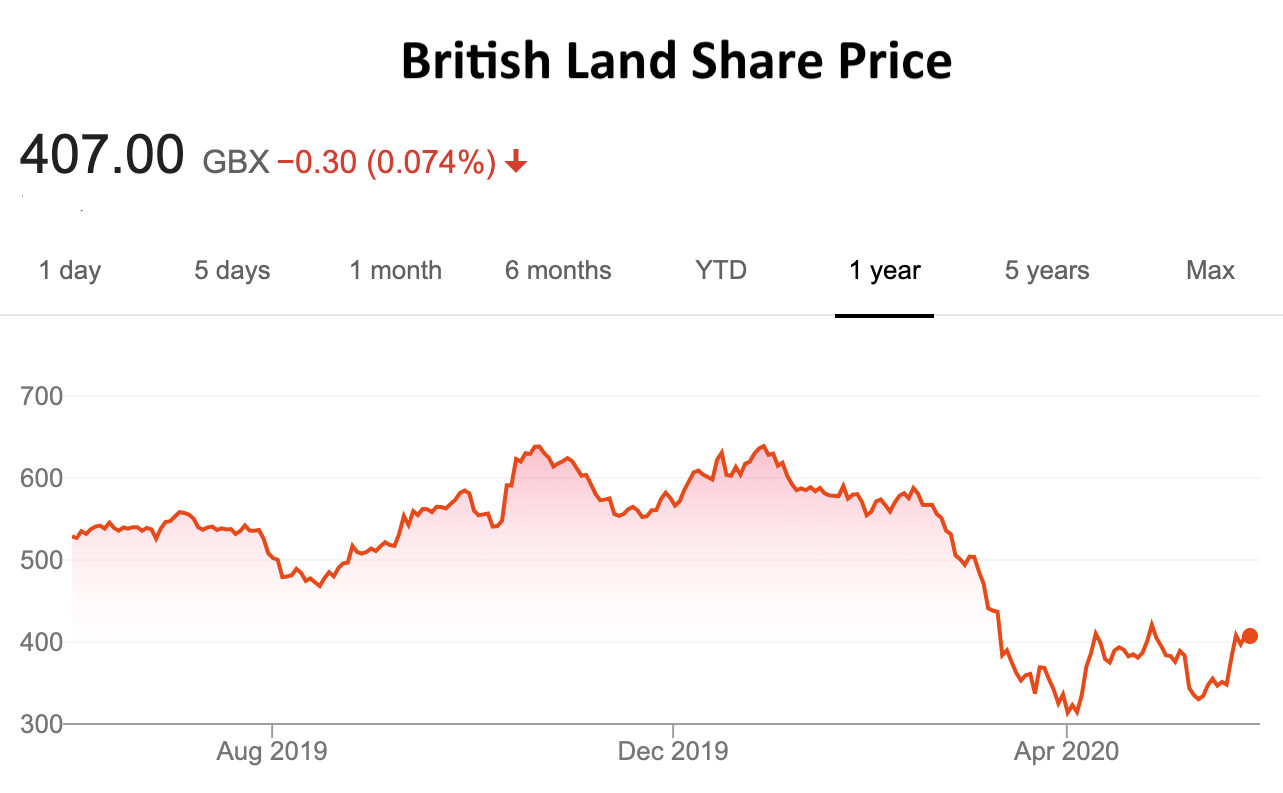

Brookfield have declared a 7.3% stake in British Land (BLND) – the UK property company.

This is interesting as Brookfield in the early 2000s bought a stake in Canary Wharf Group eventually, in 2014, taking it over (together with QIA via Songbird).