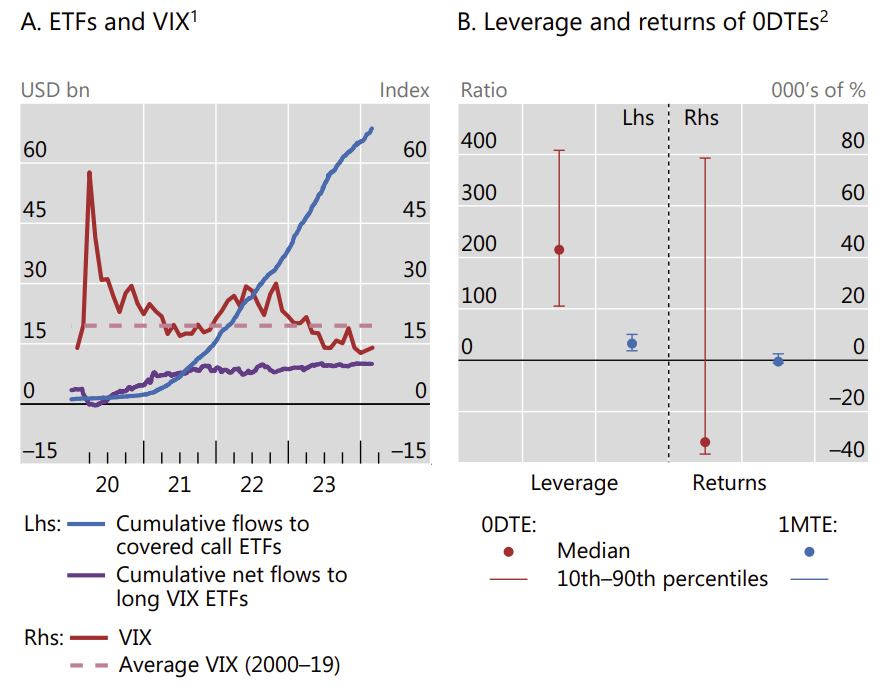

Latest BIS quarterly thinks it is not because of the rise of 0DTE options (those that expire the same day). This week these hit a new record volume share at 57%.

Rather the rise of yield-enhancing ETFs that sell options (in various forms) is the real culprit – see lhs of chart. JPM has some further analysis via FT.

While on the topic of 0DTE the rhs chart shows their truly lottery-like payoff structure.

“Investing in 0DTE options loses money on average, with annualised returns of -32,000%, but on rare occasions generates extremely high returns of up to 79,000%. These returns are much more volatile than the returns on one-month options, which have an average return of -550% annualised and a maximum of 2,500%.”