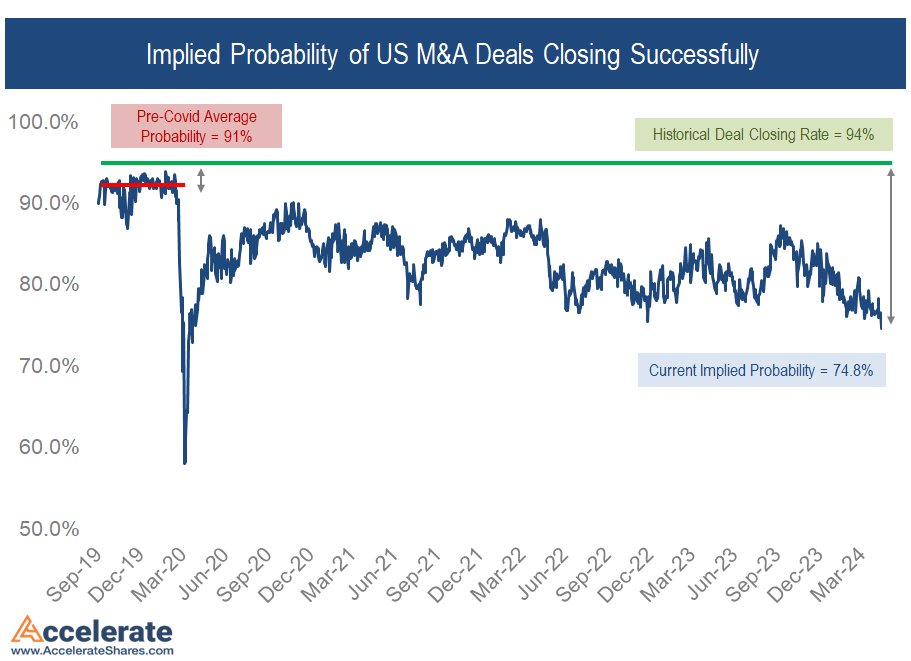

The probability of deal success is currently very low. In a small part, this is due to interest rates but also an aggressive DOJ/FTC (see JetBlue/Spirit).

Everything you wanted to know about the publishing business from that time Random House tried to buy Simon & Schuster and the DOJ sued making “the head of every major publishing house and literary agency got up on the stand to speak about the publishing industry and give numbers …”.

“I think I can sum up what I’ve learned like this: The Big Five publishing houses spend most of their money on book advances for big celebrities like Britney Spears and franchise authors like James Patterson and this is the bulk of their business. They also sell a lot of Bibles, repeat best sellers like Lord of the Rings, and children’s books like The Very Hungry Caterpillar. These two market categories (celebrity books and repeat bestsellers from the backlist) make up the entirety of the publishing industry and even fund their vanity project: publishing all the rest of the books we think about when we think about book publishing (which make no money at all and typically sell less than 1,000 copies).“

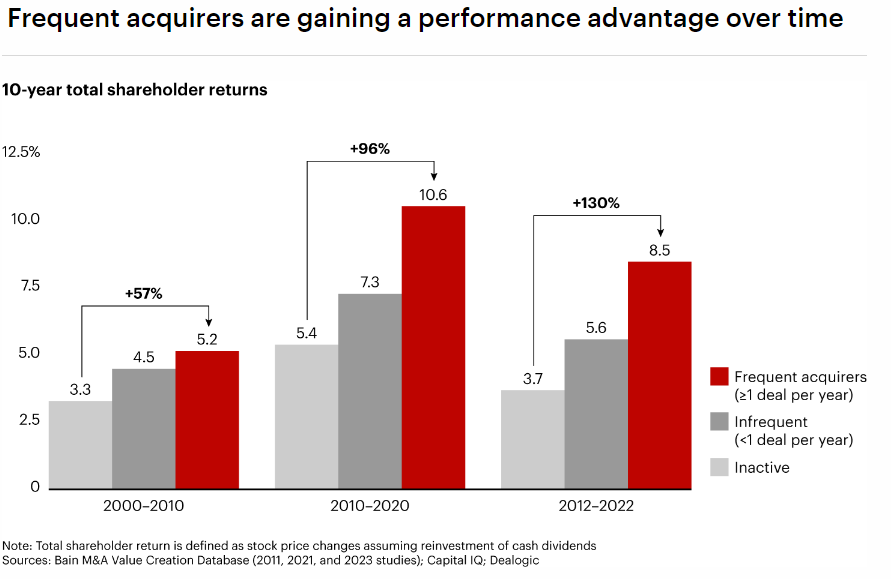

Bain study shows that frequent acquirers outperform.

“To put some data behind this assertion, from 2000 to 2010 companies that were frequent acquirers earned 57% higher shareholder returns vs. those that stayed out of the market. Now that advantage is about 130% (see Figure 1).“

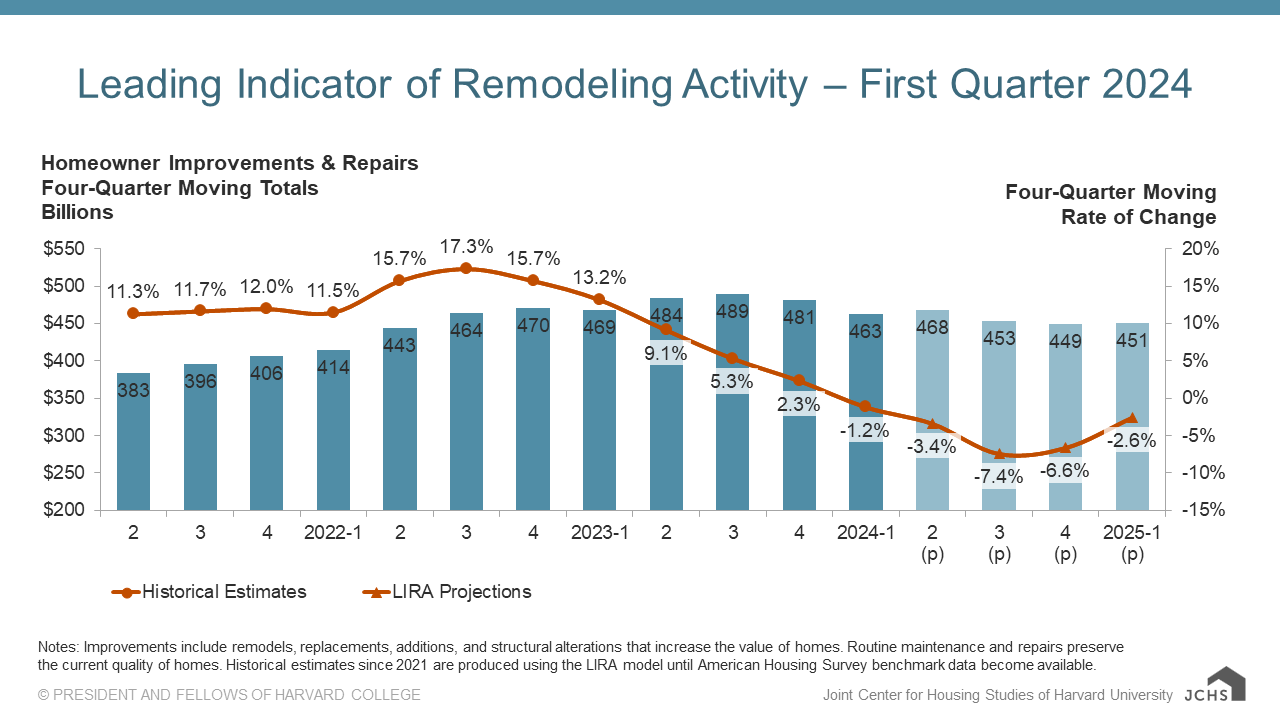

Harvard tracks the short-term outlook for home improvement spend.

“The indicator, measured as an annual rate-of-change of its components, is designed to project the annual rate of change in spending for the current quarter and subsequent four quarters, and is intended to help identify future turning points in the business cycle of the home improvement and repair industry.“

Right now a bottom is seen in Q3 2024. The trajectory is a big upgrade on their previous outlook.

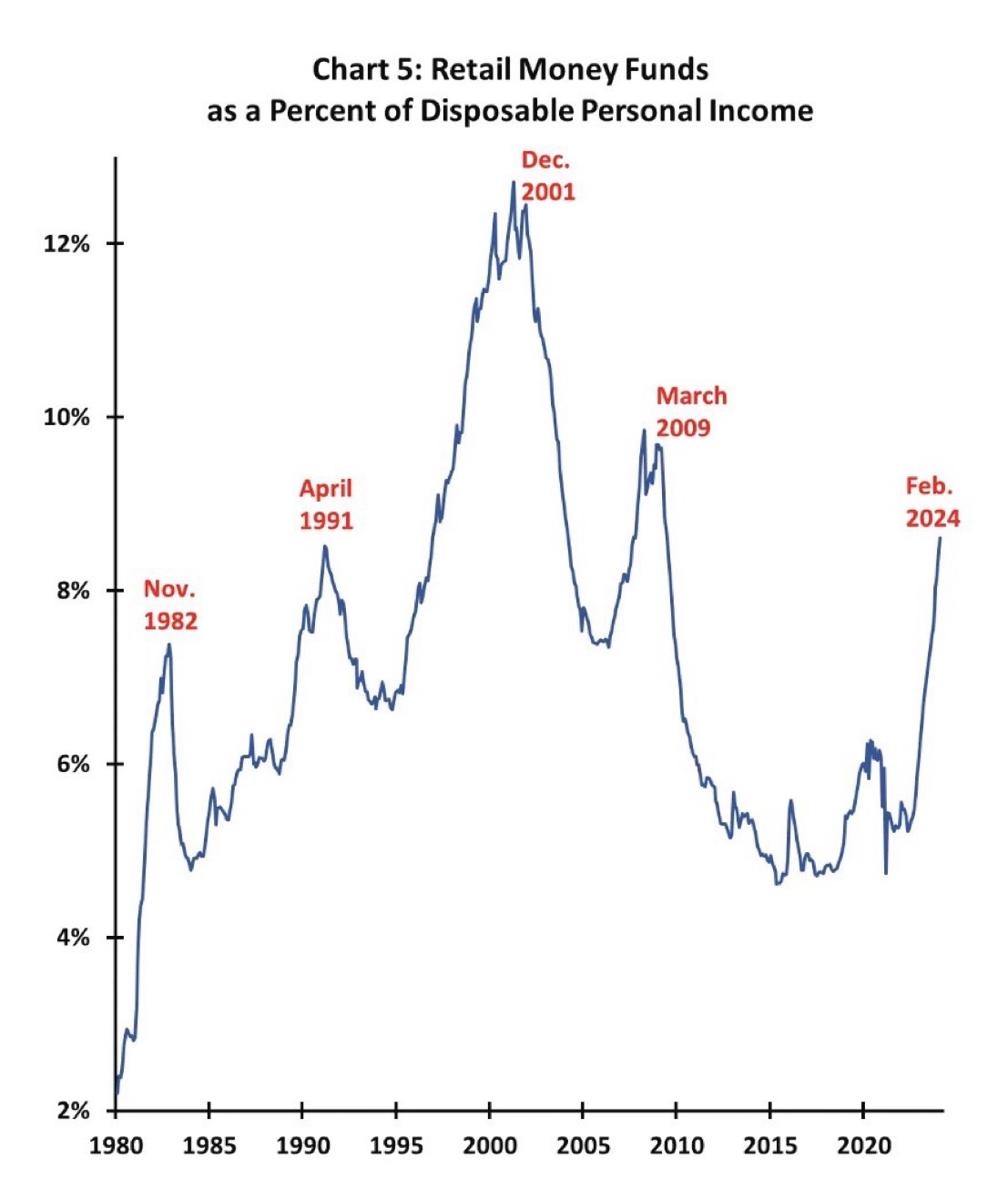

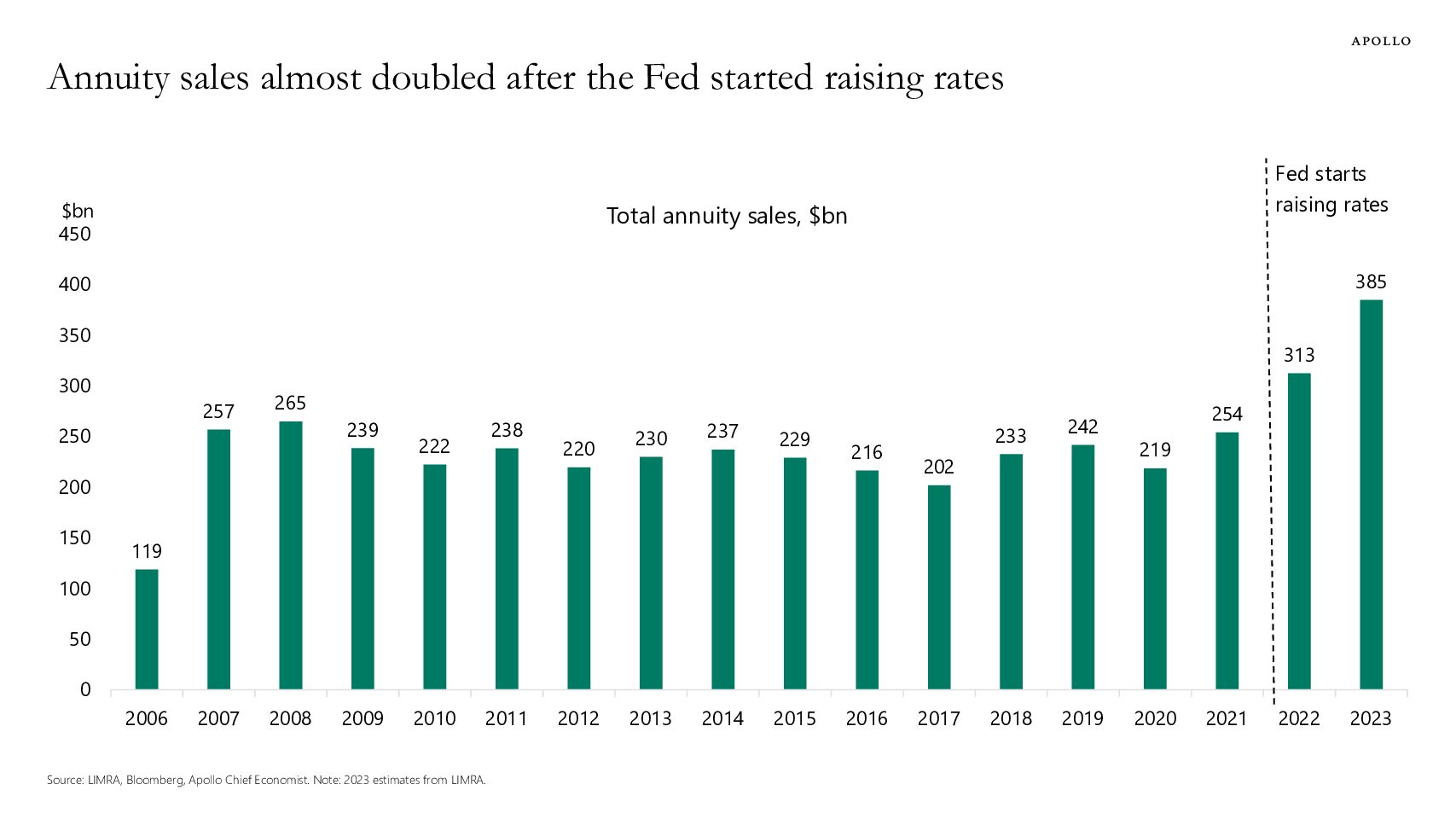

“Annuity sales are almost double their pre-pandemic levels because of higher interest rates. And strong annuity sales create strong demand for credit, see chart below.“

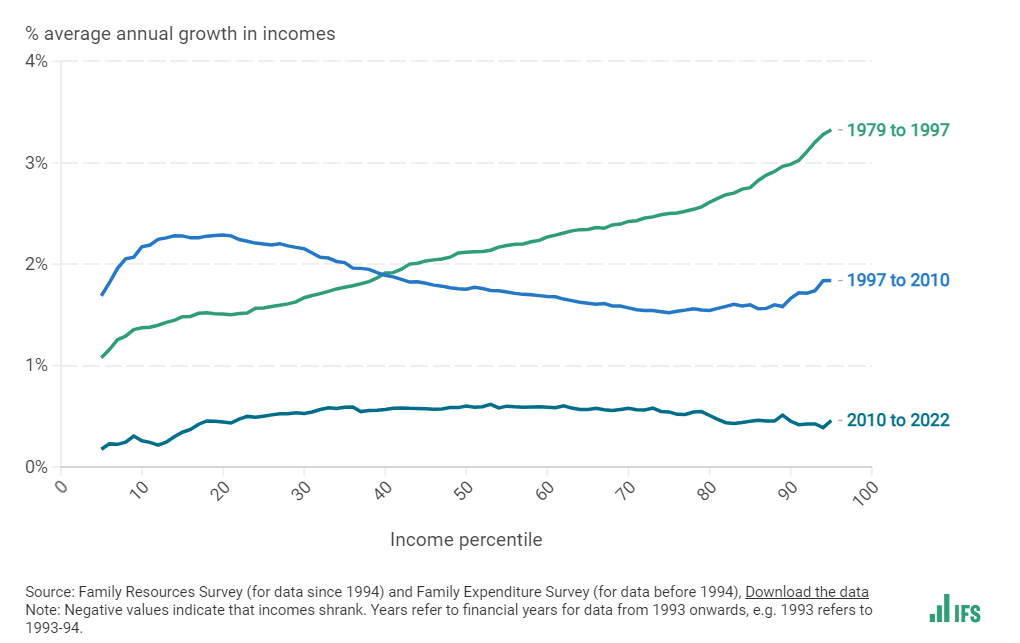

Nice page from IFS on how income inequality, living standards and poverty are evolving.

This one, in particular, is interesting – “Another way to see how income inequality has changed over time is the following chart – known as a ‘growth incidence curve’. This shows the average annual percentage growth in incomes at each percentile of the income distribution, for selected time periods.“

Tolerability looks to be important long-term followed closely by supply, the key constraint currently as GLP-1 molecules are peptides, which could be solved instantly if a non-peptide white pill is developed.