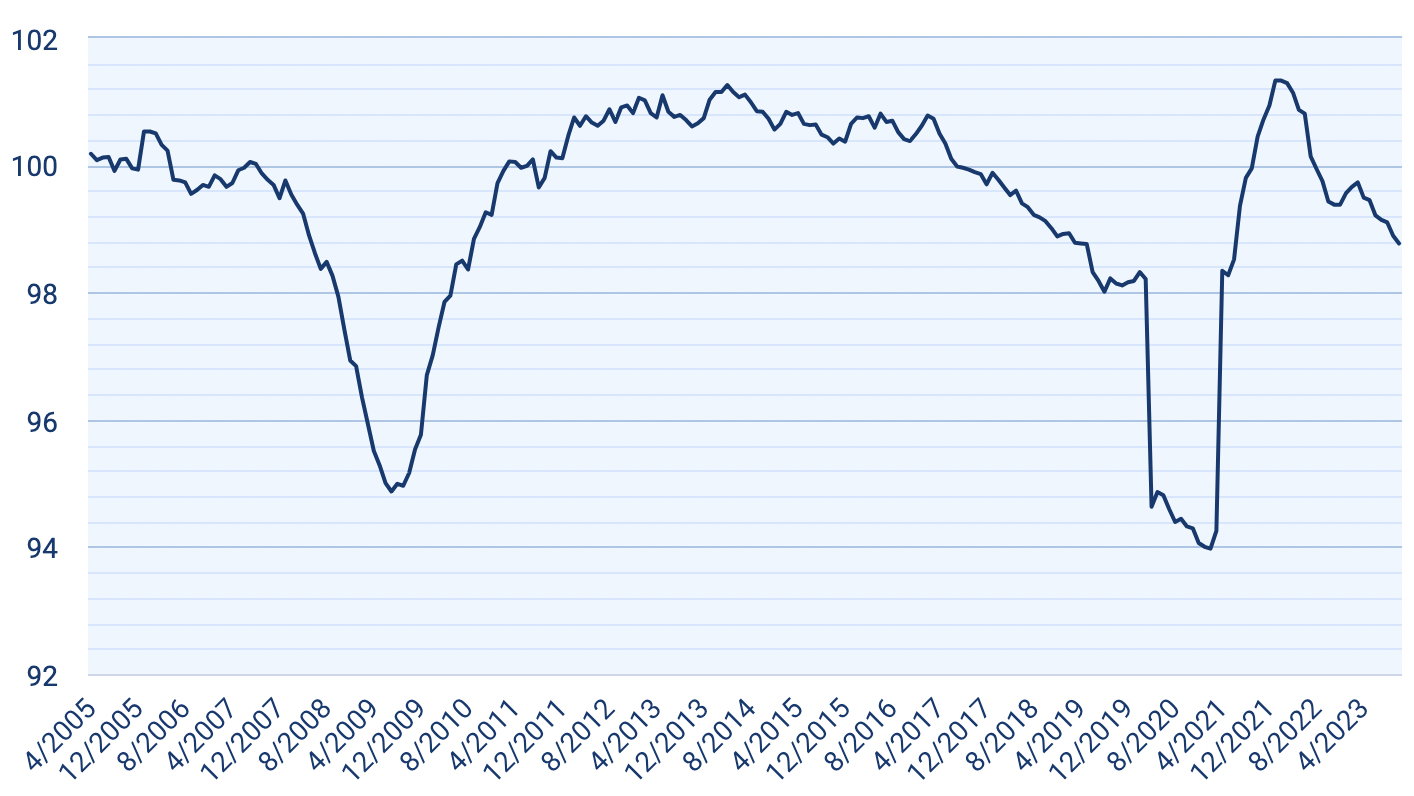

“The rate of small business job growth has slowed in 17 of the last 20 months, falling from the record high of 101.33 in February 2022 to 98.77 in October 2023.“

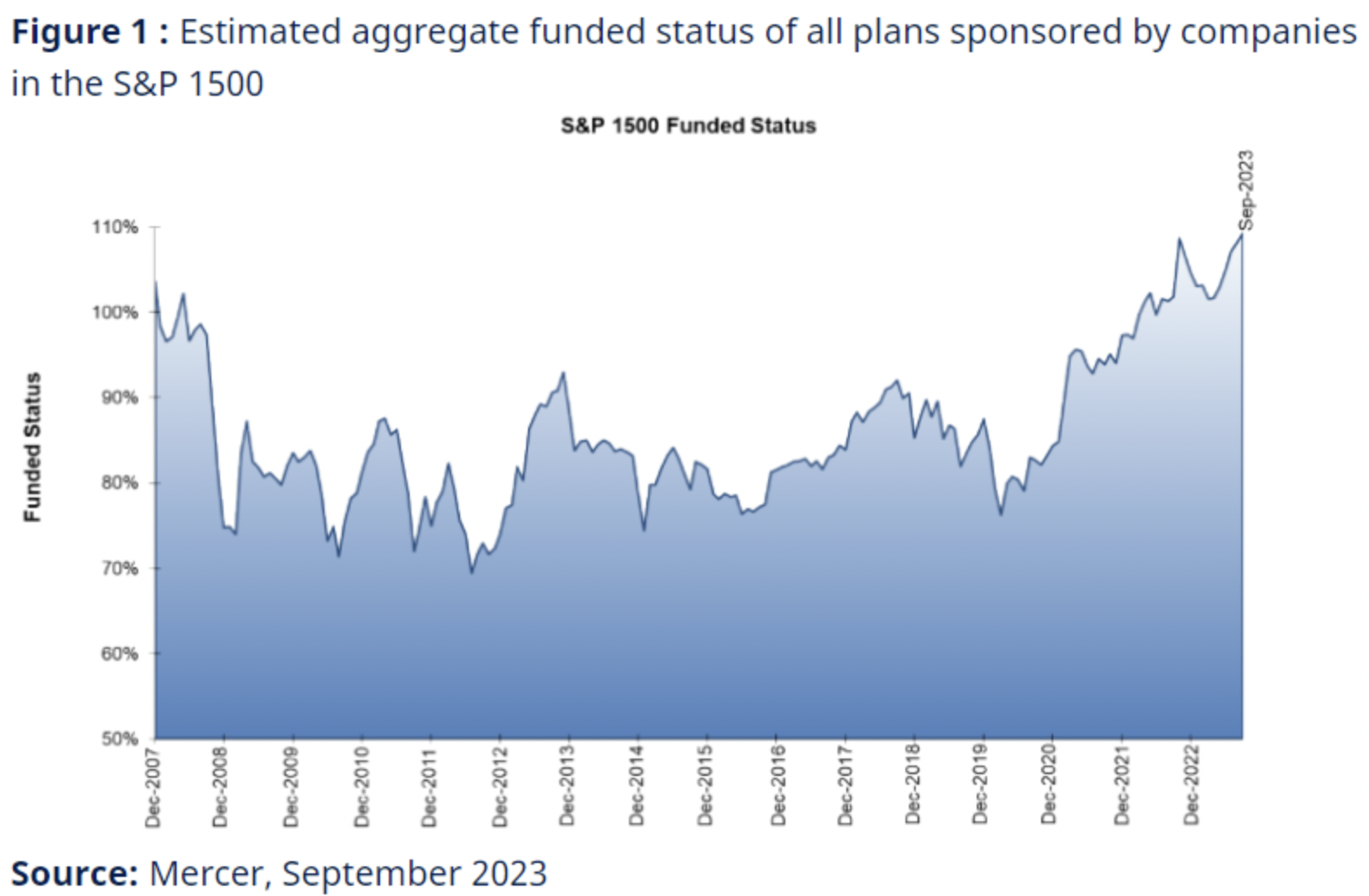

One upside of rising bond yields is pension plan liabilities. These are pricing downwards pushing many pension plans into surplus relieving the cash flow pressure on sponsor companies.

The full transcript of the testimony given by Lee Cain and, especially, Dominic Cummings for the inquiry into the government’s handling of the Covid emergency makes for long but utterly fascinating reading.

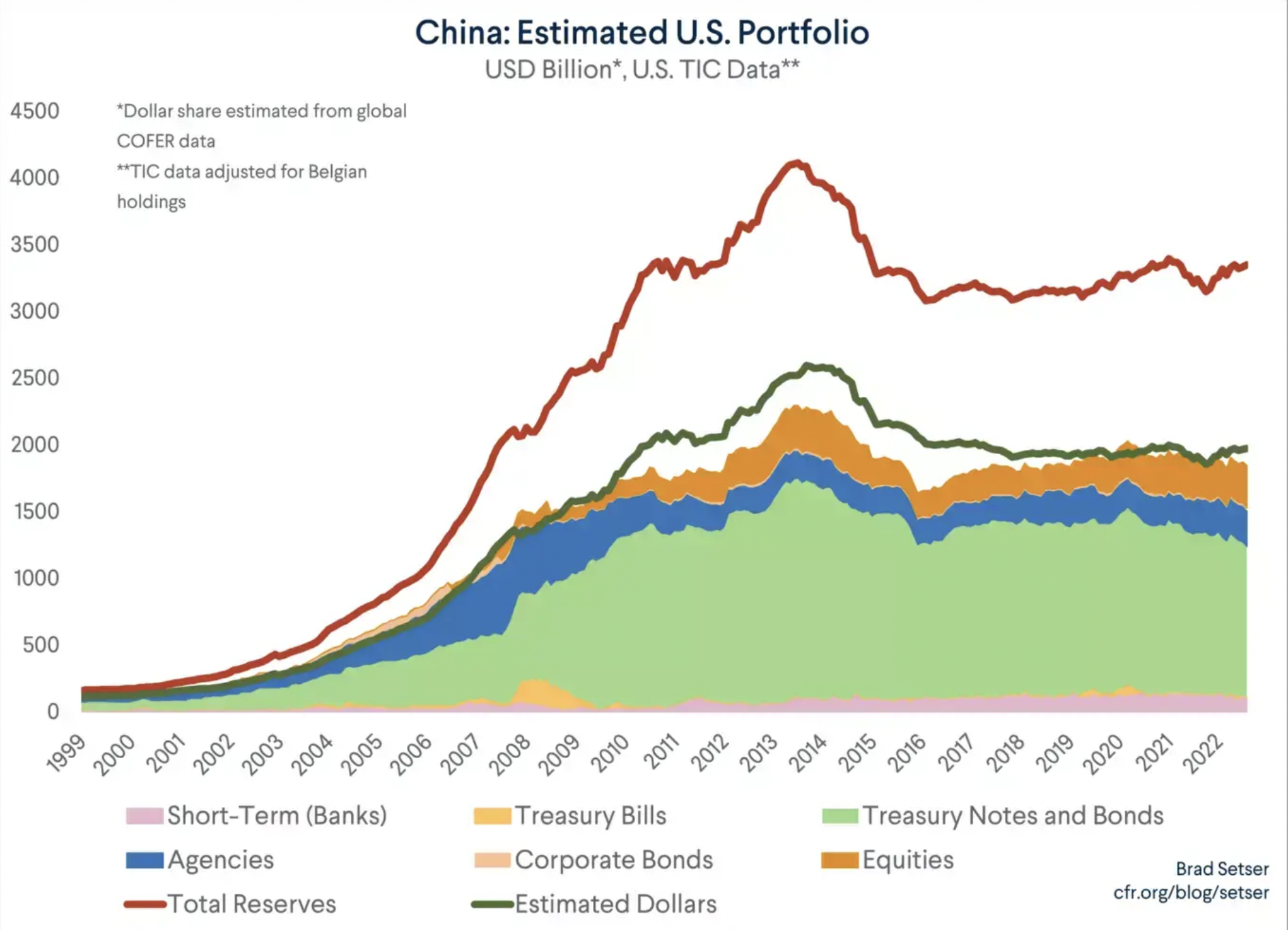

The world of foreign exchange reserves is full of false narratives and complex data.

Here, Brad Setser, uses international banking sleuthing to show that China has not switched its reserves away from dollars.

“Bottom line: the only interesting evolution in China’s reserves in the past six years has been the shift into Agencies. That has resulted in a small reduction in China’s Treasury holdings – but it also shows that it is a mistake to equate a reduction in China’s Treasury holdings with a reduction in the share of China’s reserves held in U.S. bonds or the U.S. dollar.“

Healthcare is one area where the application of AI, in its LLM and other forms, could be enormous.

This nice article from AlphaSense Expert Insights explores the topic, mirroring the huge rise in expert calls in the sector mentioning the term.

It is not all areas that can be bent to the will of ML. As this piece argues, academic literature and the correspondent knowledge graph is both difficult and not that useful to program.

If you want to read some of these transcripts, you can grab a two-week free trial.

“Cancelling HS2, and rolling back on net zero, are two vivid examples of a long-term UK problem that has become acute since 2010. The government does not invest enough, and partly as a result the private sector does not invest enough. As this excellent report from the Resolution Foundation’s Felicia Odamtten & James Smith shows, public and private sector investment are complements; the former encourages the latter. This chart from the report shows that UK public investment is consistently below the international average, and that average includes many countries that have underinvested over the last two decades like Germany and the US.“

High-Speed 2 (HS2), the flagship rail line, as the blog points out, is not about faster transit time between the North and London, but rather helping create more capacity around major northern cities to improve their development. As the chart in the blog shows, outside of London, major UK cities are woefully behind other comparable cities in Europe in terms of productivity. This is something we covered before.

An extremely useful site (h/t) for tracking job postings by industry or company.

Here for example is what Walmart hiring looks like.

Shockingly the retail giant said they won’t be doing any seasonal hiring this year. In contrast, they hired 40,000 seasonal workers last year, and 150,000 in 2021.

Bill Gurley’s September 2023 talk “2,851 Miles.” is a very interesting read on this very important topic in economics and investing.

As a rule, regulation is acquired by the industry and is designed and operated primarily for its benefit.” I like to say, “Regulation is the friend of the incumbent.”

As markets look to peak policy rates and beyond, this newsletter has been a really useful one-stop shop to get a detailed overview of central bank action and markets.

For example the declining Clevland Fed nowcast of inflation (source).

The latest 2023 report is worth a flick (all 160 slides).

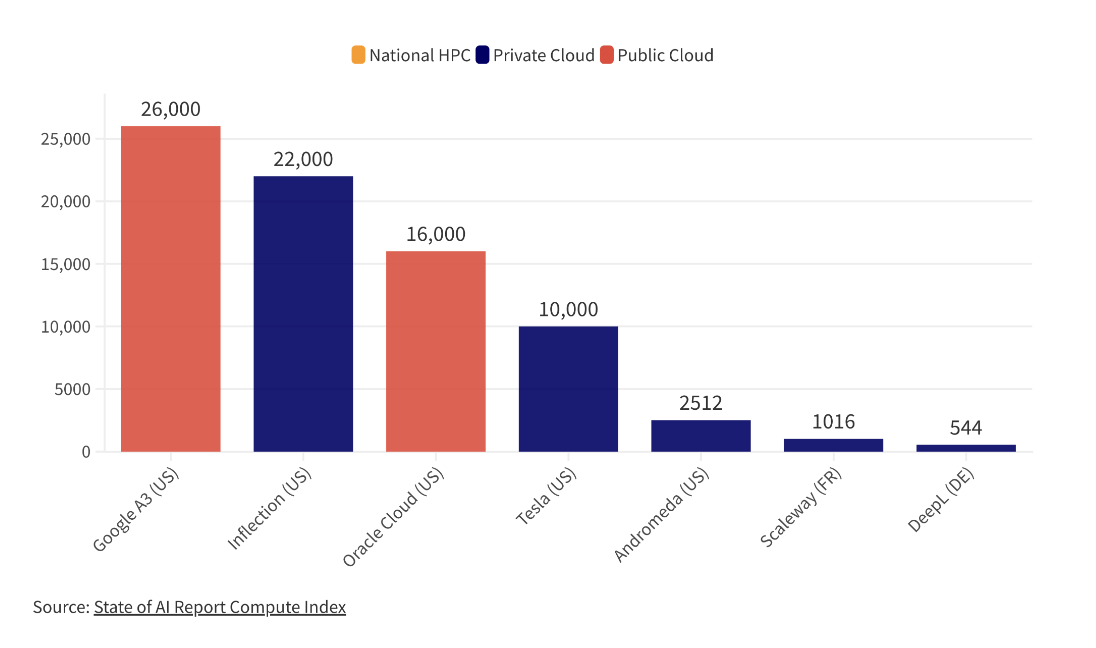

This graph, for example, shows the largest Nvidia H100 chip clusters – interesting to see TSLA there, who also run the 4th largest A100 cluster in the world.

Or see Slide 76 which suggests that Nvidia’s advantage (the use of its chips in academic papers) continues to increase.

Investment managers that carry large short positions in equity securities will be required, within two weeks after each month, to report those positions and related short sale activity to the Commission. The threshold for reporting will be met when an investment manager’s short position in a particular equity security of a reporting issuer is at least $10 million or the equivalent of 2.5 percent or more of the total shares outstanding on average during a month.

Based upon the filings to the Commission, the Commission will make public, within four weeks after the end of each month, aggregated, anonymized data about the gross, end-of-month large short positions. The Commission also will publish the net aggregated daily activity data for each settlement day.

The UK (and EU) have good disclosures on shorts >0.5% of shares outstanding.