“This enormous land parcel is also unique in that it’s a kind of self-governing municipality, with its own fire department and emergency services. The district—officially known as the Reedy Creek Improvement District—is governed by a five-person Board of Supervisors elected by the landowners in the district. As a result, high-level Disney employees essentially run the entire region encompassing WDW.“

The area is so vast that “The Magic Kingdom parking lot, for example, is actually larger than the theme park itself.”

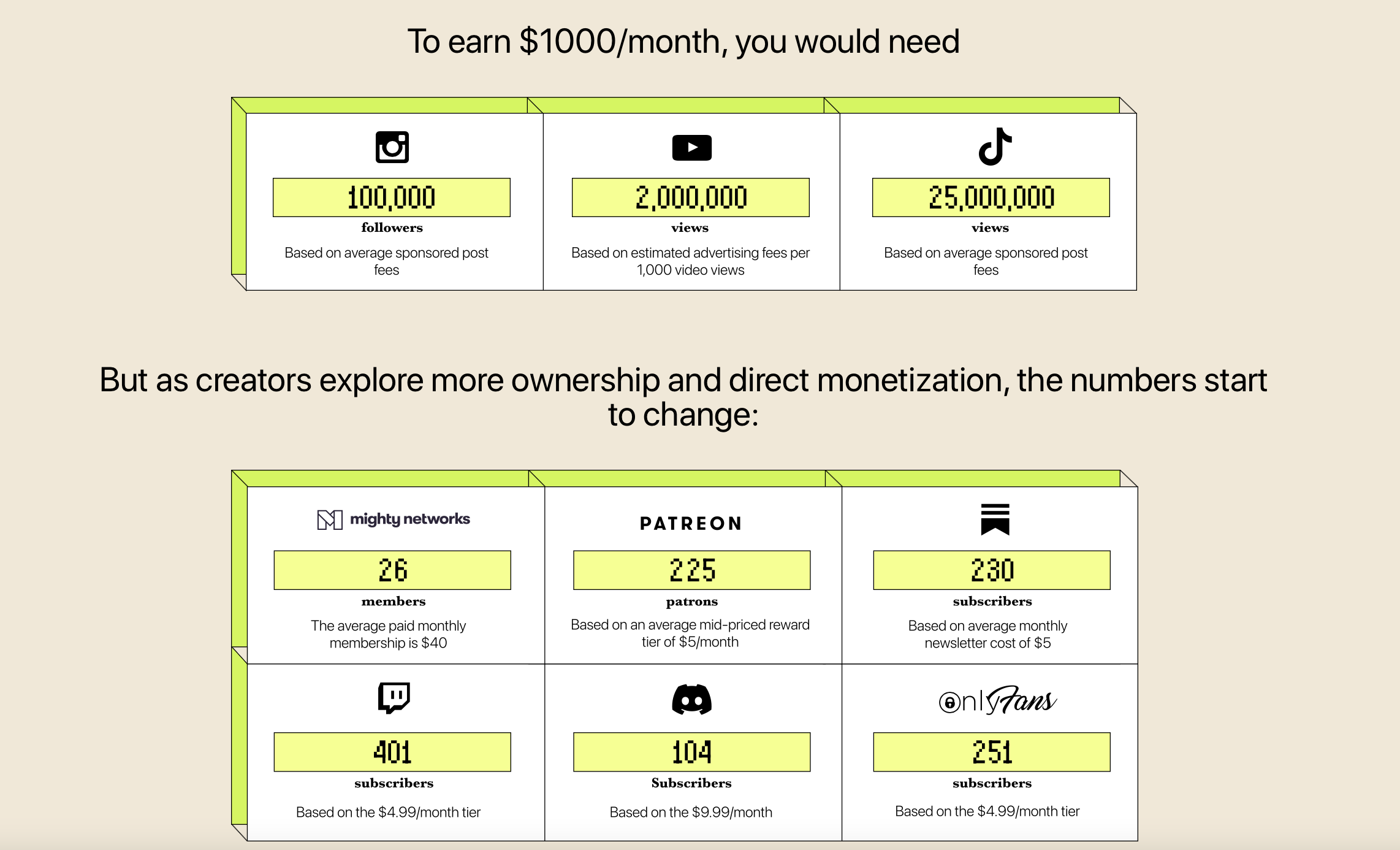

“In aggregating monetization across these 50 platforms, we’ve found that creators will soon pass more than $10 billion in aggregate earnings. While 2020 saw a jump in new creators, it wasn’t a one-time spike. A year later, creators are still coming online at a record clip: the number of creators is up a whopping 48% year-over-year. In total, these platforms have onboarded 668,000 creators.“

Substack just announced they have hit 1 million paid subscribers.