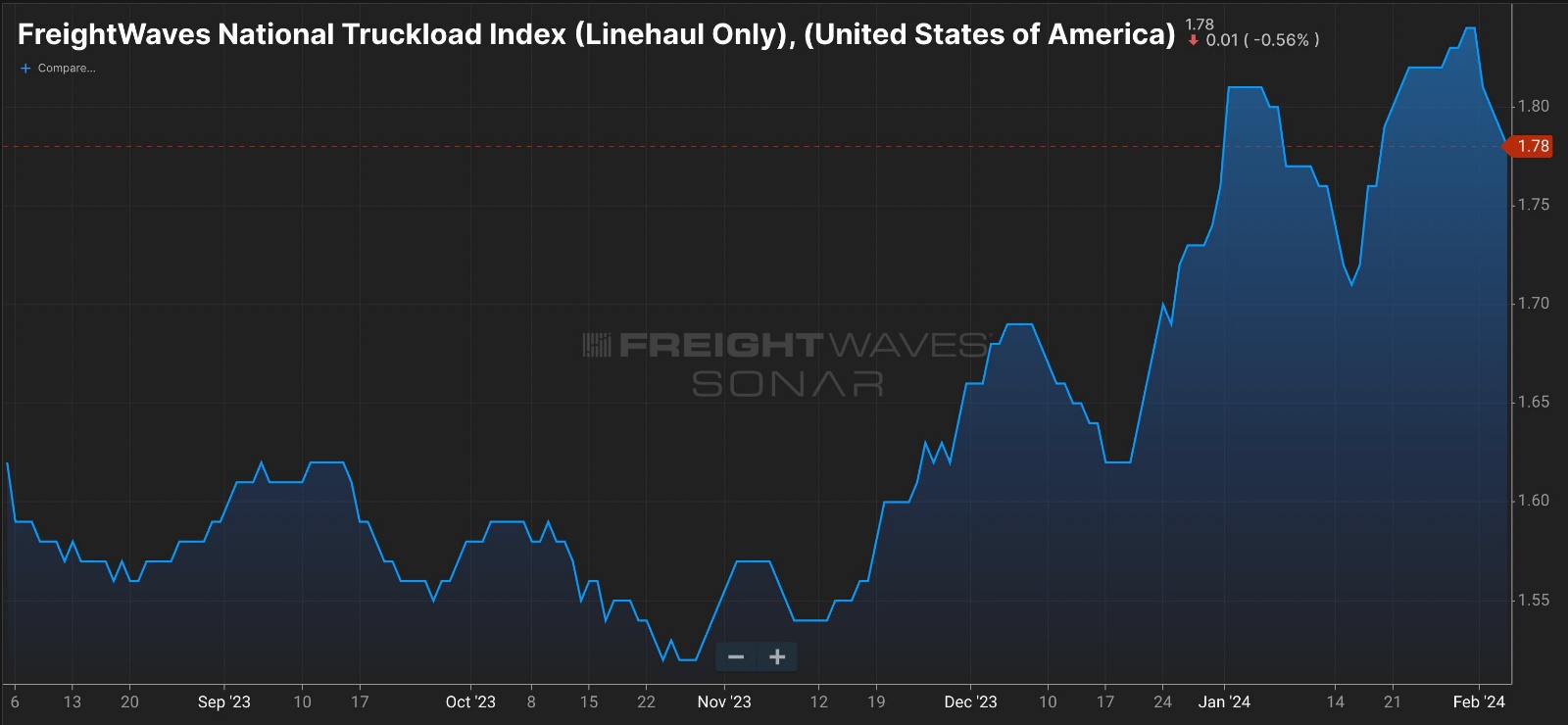

“By most metrics, freight markets are showing clear signs of a lasting recovery … In short, the early stages of this recovery are characterized by a rebalancing market, a return to normalcy after a four-year roller coaster of volatility.“

“The common trait of people who supposedly have vision is that they spend a lot of time reading and gathering information, and then they synthesize it until they come up with an idea.” — Fred Smith, Overnight Success: Federal Express and Frederick Smith, Its Renegade Creator

It was always hard and it isn’t getting any easier.

A nice article reflecting on the troubles of the Boeing 737 MAX – an update to a 50-year-old plane instead of a brand new model and why that decision was taken.

As we wrote before there really isn’t anything like this industry – “Aerospace is one of the deepest branches of humanity’s technological tree. It is a telling fact that more countries have produced a nuclear bomb than mass-produced a jet engine.“

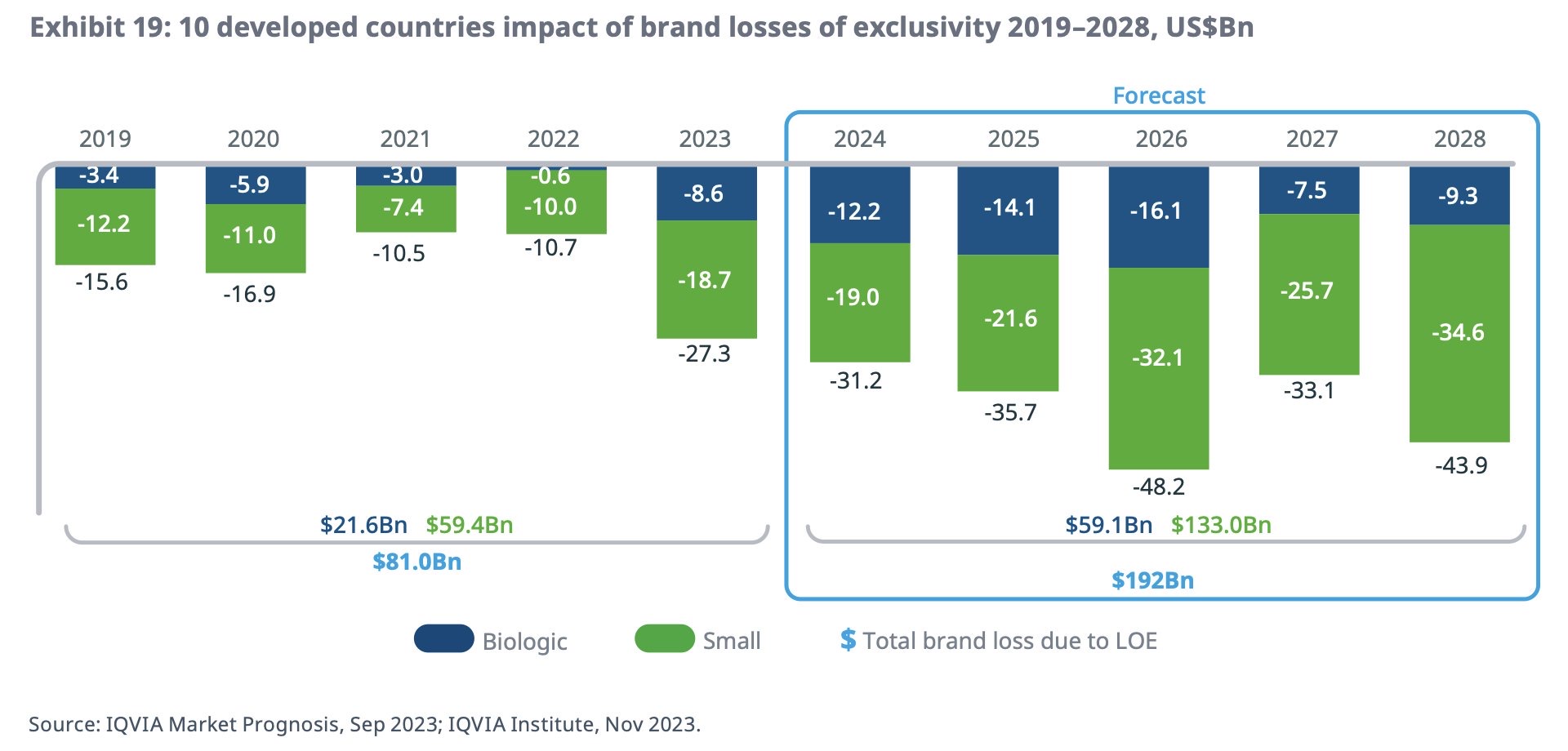

Surprisingly a flurry of deals at the end of the year means 2023 was a record in terms of the number of deals >$1bn in value (source: Centerview, h/t Tema).

One of the reasons is likely a looming patent cliff.

Tema estimates that large-cap pharma has $838bn of dry powder – enough, even after the rally, to buy almost 70% of the XBI (without a premium).

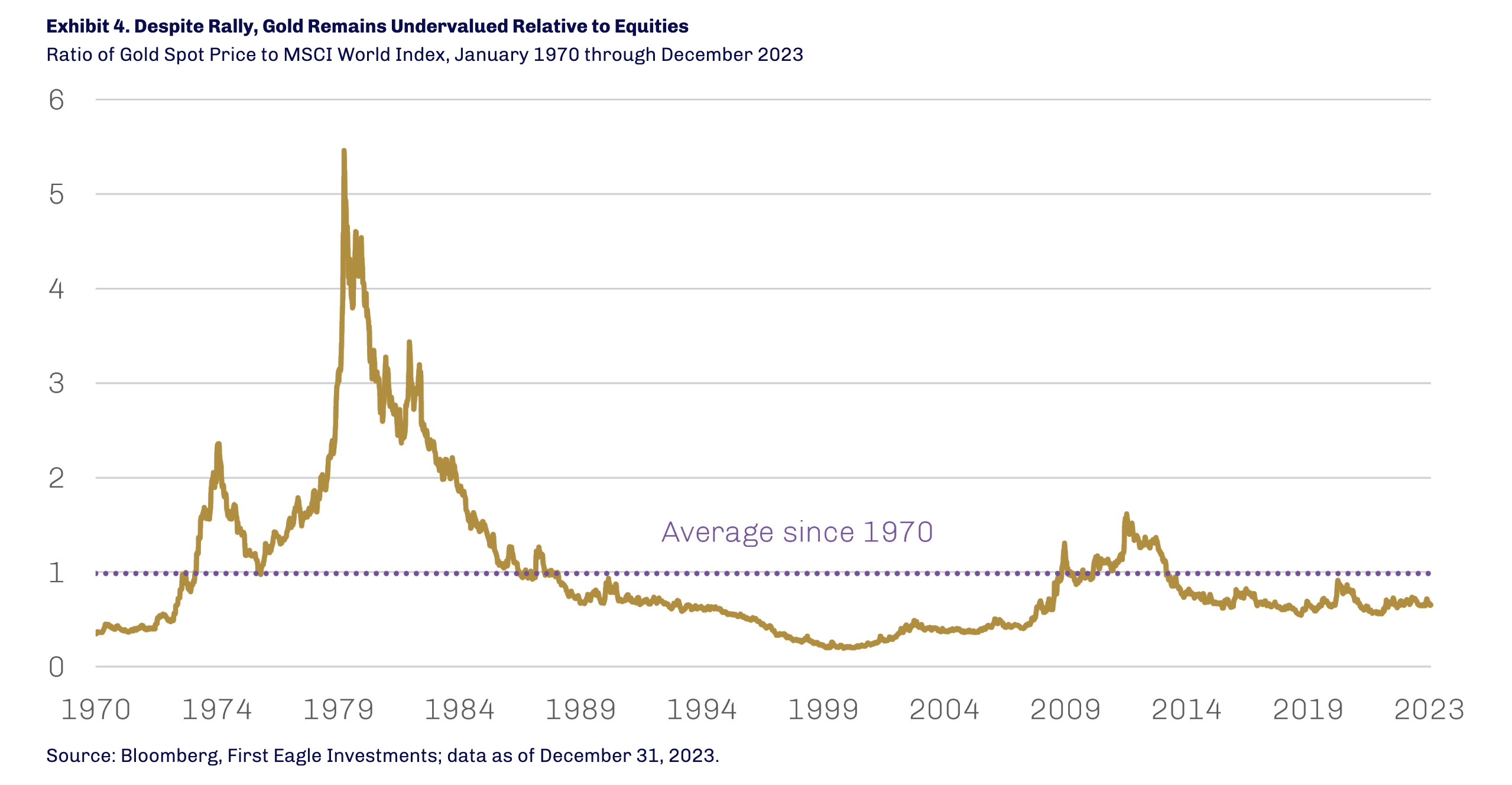

The below sticks out. It is something many UK investors have long ago had to become accustomed to.

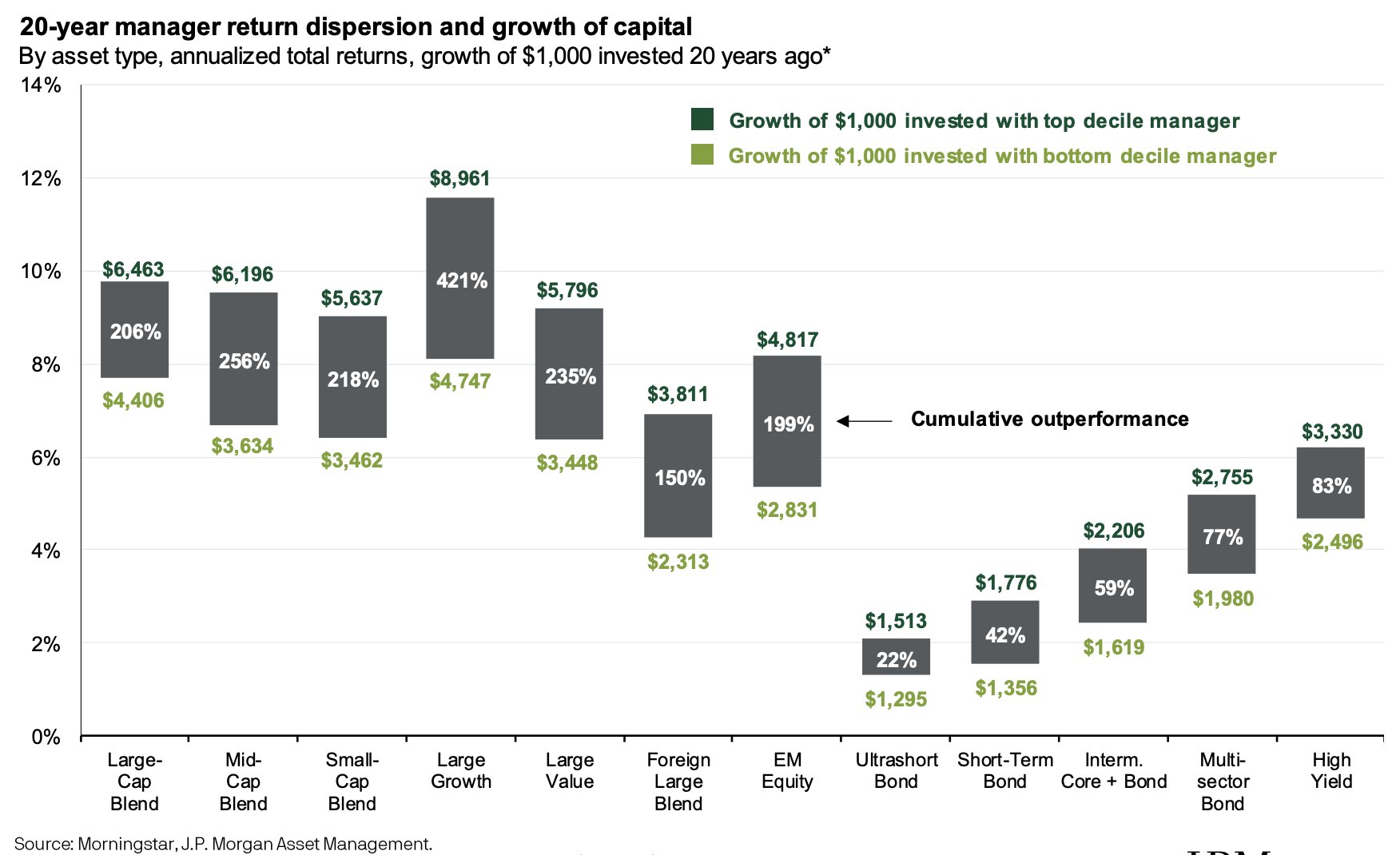

“We believe that the strong returns and alpha from the long book came from a successful adaptation of our style. We have become even more disciplined about price and emphasize investments where we get paid by the issuers, as opposed to relying on other investors to revalue the security. Payment can come to us in the form of buybacks, dividends, interest, or in some cases, a take-out from a buyer. With the decimation of the active fund management industry, we don’t believe we can reasonably expect securities to be re-rated by investors who are actively trying to figure out what they are truly worth.“

Interesting corollary from Ben Evan’s “the most interesting thing is a new Google feature called ‘circle to search’. You can use your finger to draw a circle around anything on your Android phone screen, in any app, and Google will do a text or image search. So, you can circle a hat in a Tiktok and Google will tell you where to buy it. It occurred to me a while ago that screenshots are the native file format of smartphones, but they lose context. But what if the OS knows what’s on the screen, in every app? Screen-scraping is the new API…”

A very good history of Y Combinator and how Paul Graham, through his essays and otherwise, had a huge part to play in building the cult of the founder.

This history is trapped inside a not-so-convincing argument of YC’s demise.

Excellent interview with Herbert Hovenkamp professor at Penn Law School specializing in US anti-trust on what he thinks of the big cases against Big Tech in the US.

Worth a read for any holders of AAPL, META, GOOG, AMZN.

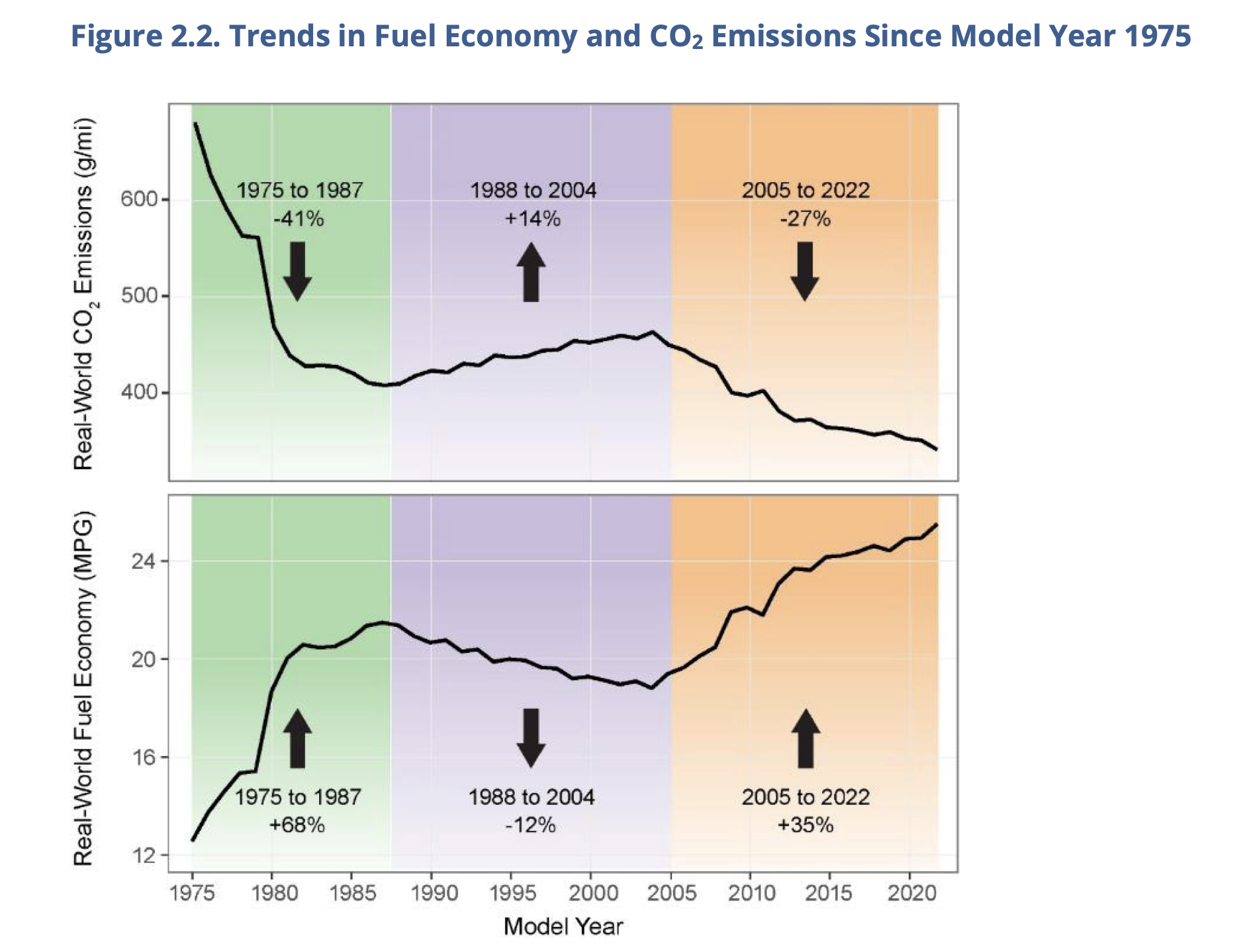

“In model year 2022, the average estimated real-world CO2 emission rate for all new vehicles fell by 10 g/mi to 337 g/mi, the lowest ever measured. Real-world fuel economy increased by 0.6 mpg, to a record high 26.0 mpg.1 This is the largest single year improvement in CO2 emission rates and fuel economy in nine years.“

2023 model year is already showing improvement on this.

The long-term trend is encouraging (see chart) all while horsepower is up 88% since 1975 (see page 27).