“Consumers of all age groups are using around four different fragrances regularly, which is a significant change from a decade ago when they had one signature scent.“

“Some people talk about the ‘Deep Seek Syndrome,’ saying, ‘You’re overspending, you’re spending $500 billion, you’re overspending! You can save so much more by spending less.’ But I think they are looking at it the wrong way. How much percent of GDP will be replaced by a billion-dollar smart system? I would say at least 5% within 10 years. That 5% is $9 trillion—or if it’s 10%, it’s $18 trillion. So, somewhere between 5% to 10% of today’s GDP will be replaced by this superintelligence. Well, if that’s the amount of return, you shouldn’t be scared of spending a few trillion dollars. If the return is $9 to $18 trillion per year, why should you save? Why should you try to be efficient? For what? I don’t get it. Just a little difference makes a huge return on your market share.” – Softbank CEO Masayoshi Son

Source: A good smorgasbord of quotes from recent transcripts.

Fascinating paper on how fast humans throughput information, 10 bits/second, and how this is in stark contrast to our sensory system which does 10^9 bits/second.

Why this is and how is still not well understood.

“Based on the research reviewed here regarding the rate of human cognition, we predict that Musk’s brain will communicate with the computer at about 10 bits/s. Instead of the bundle of Neuralink electrodes, Musk could just use a telephone, whose data rate has been designed to match human language, which in turn is matched to the speed of perception and cognition.”

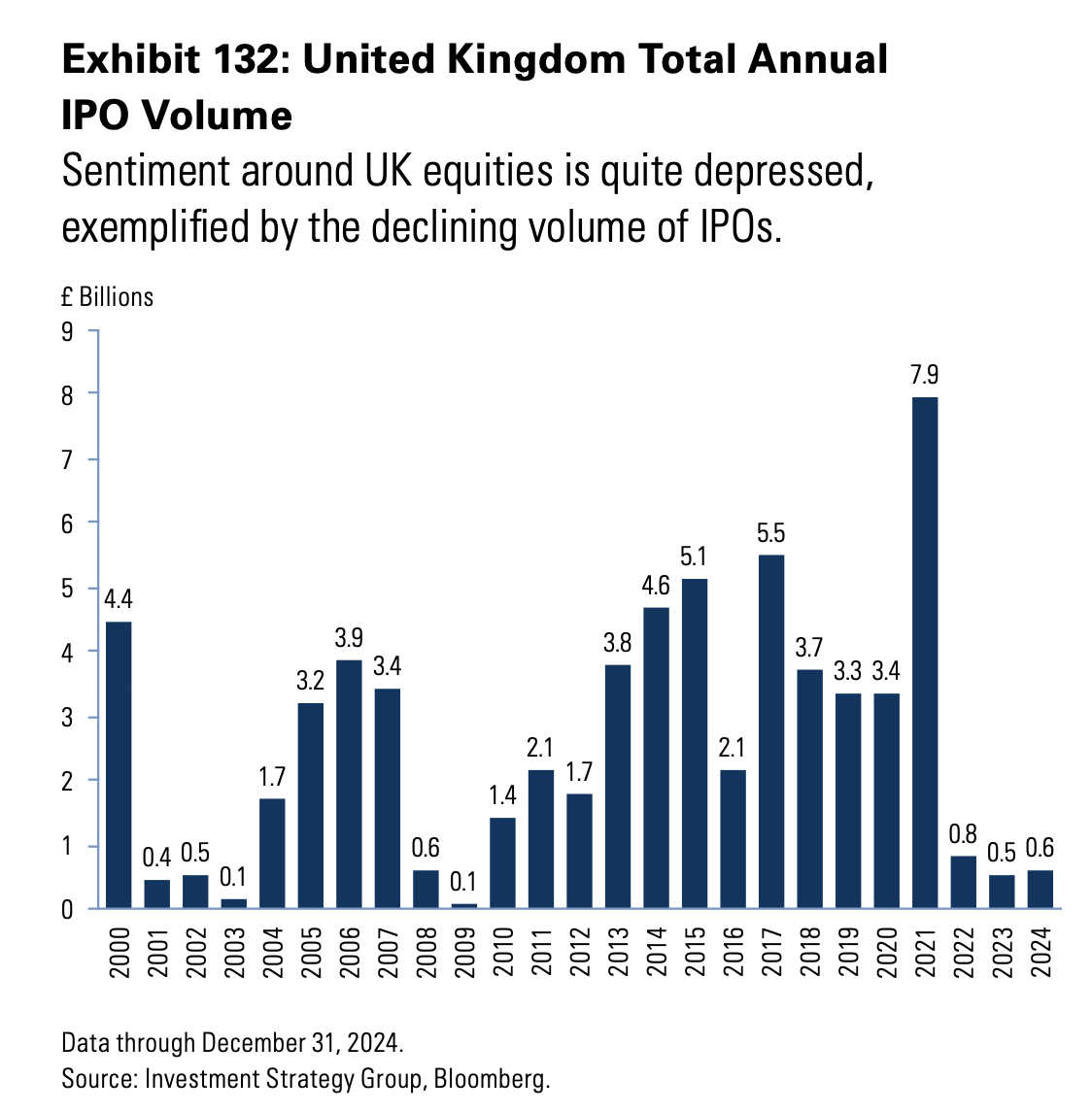

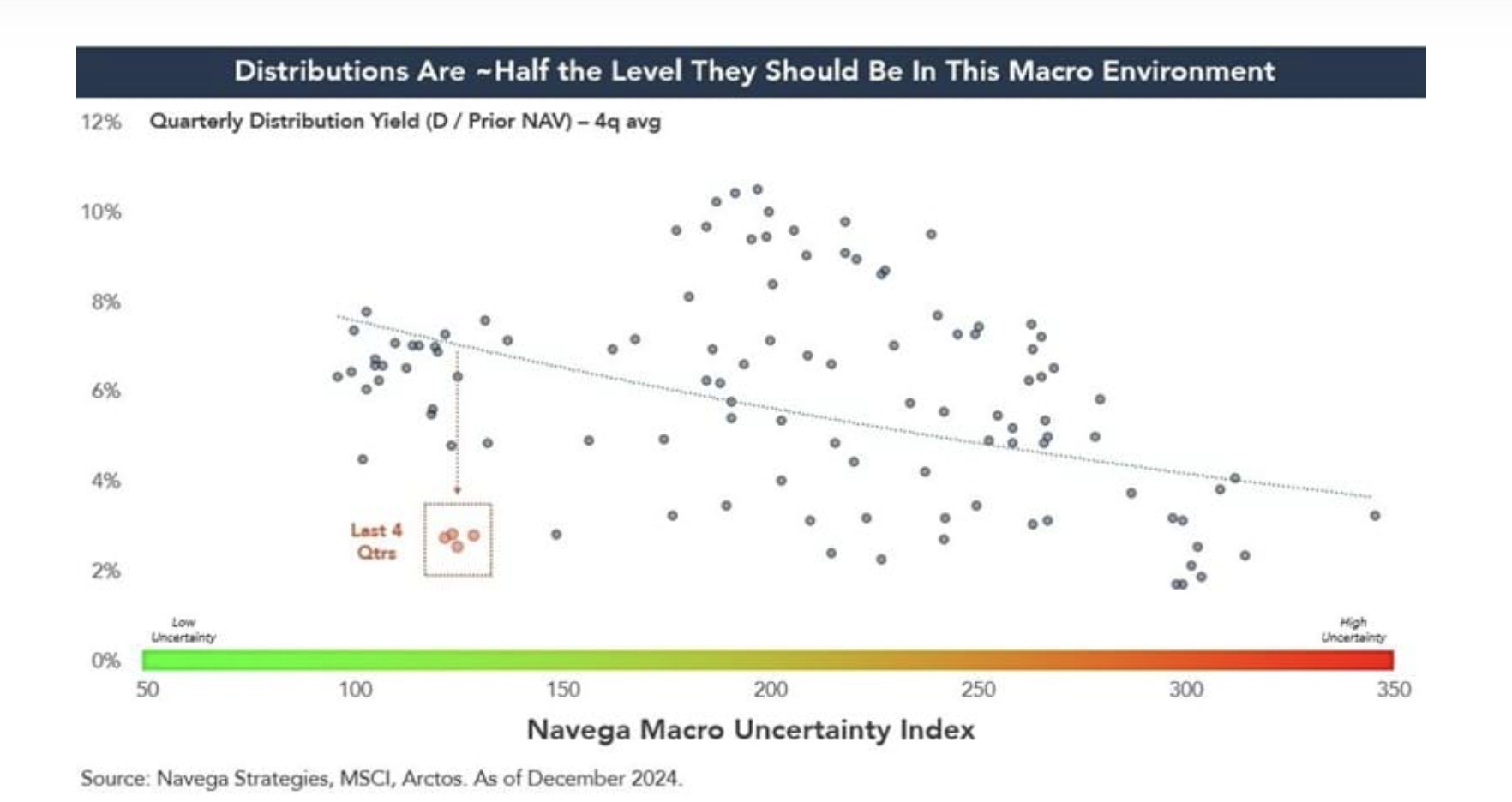

“The exit environment overall is governed by both cyclical and secular factors. Cyclical factors get a lot of airtime. Often mentioned are supportive macro, LP allocations right-sizing, and “animal spirits”. But the incentives facing sponsors get a vote. And sponsors today seeking to maximize their probability of survival face an environment that incentivizes retaining assets, lengthening their liabilities, and avoiding replacement/origination costs. This is the New Exit Game.”

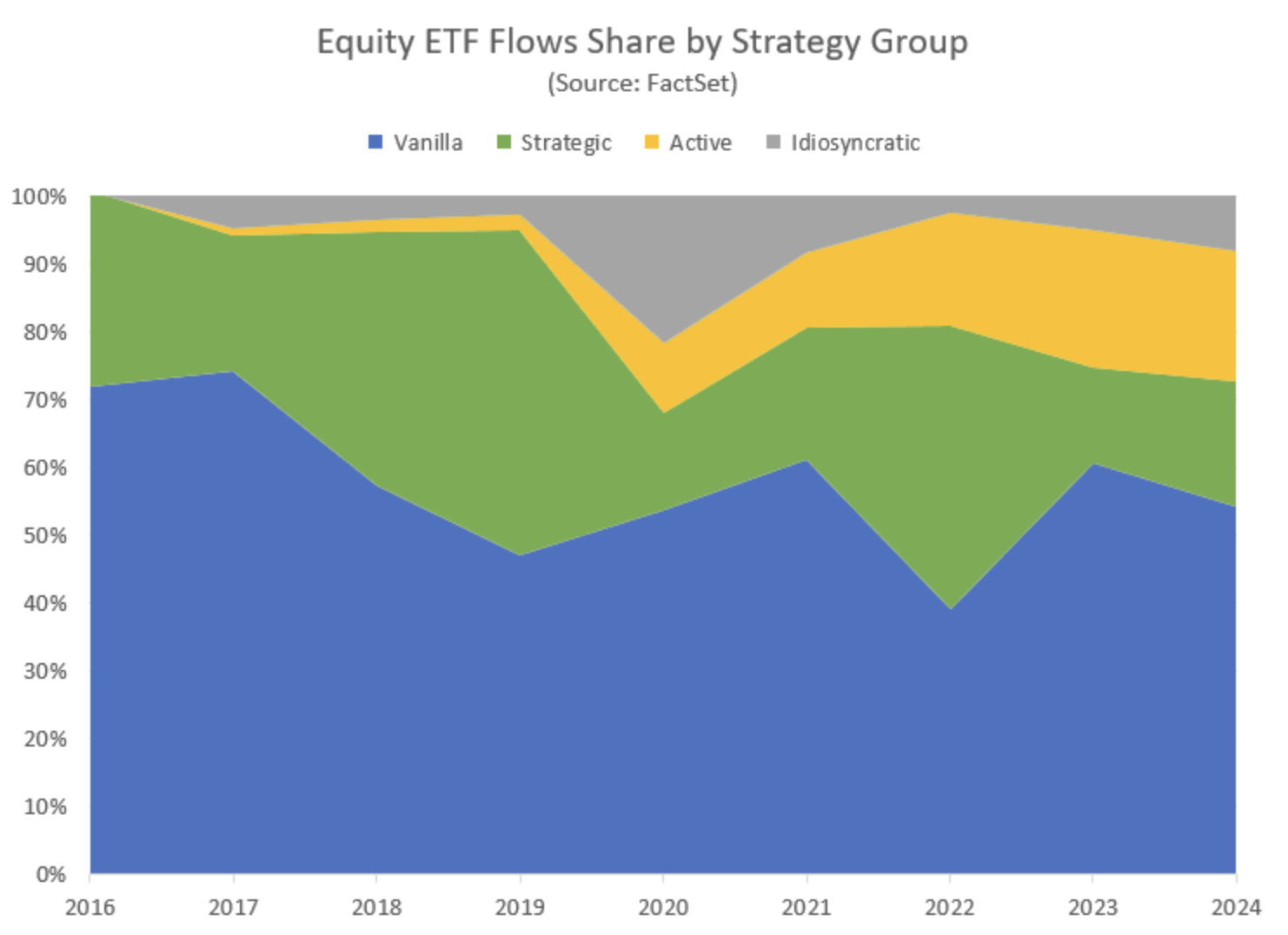

Once S&P 500 return is decomposed into factors 2024 really stands out.

“… What is particularly interesting about 2024 is how much of the S&P 500 return came from non-systematic (i.e., idiosyncratic) returns, driven by the significant appreciation of the “Magnificent Seven” (Mag-7), which now account for 35% of the S&P 500. Idiosyncratic returns are company specific and by definition should be uncorrelated and random.“

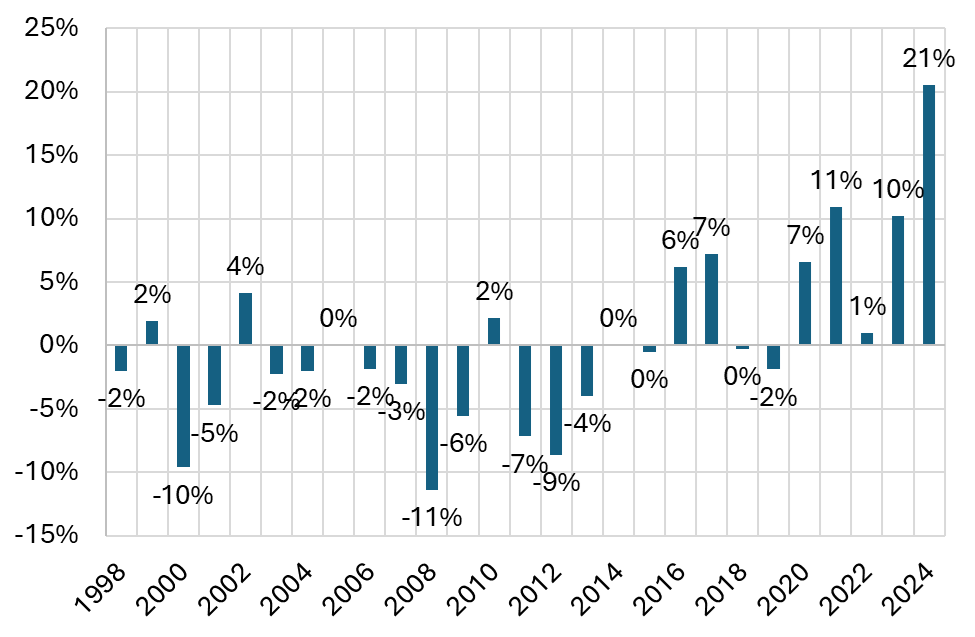

“In fact, idiosyncratic return has never contributed as significantly to the overall S&P 500 return as it has recently. Over the trailing 24 month period, idiosyncratic returns have accounted for 21% of the 51% return of the S&P 500.“