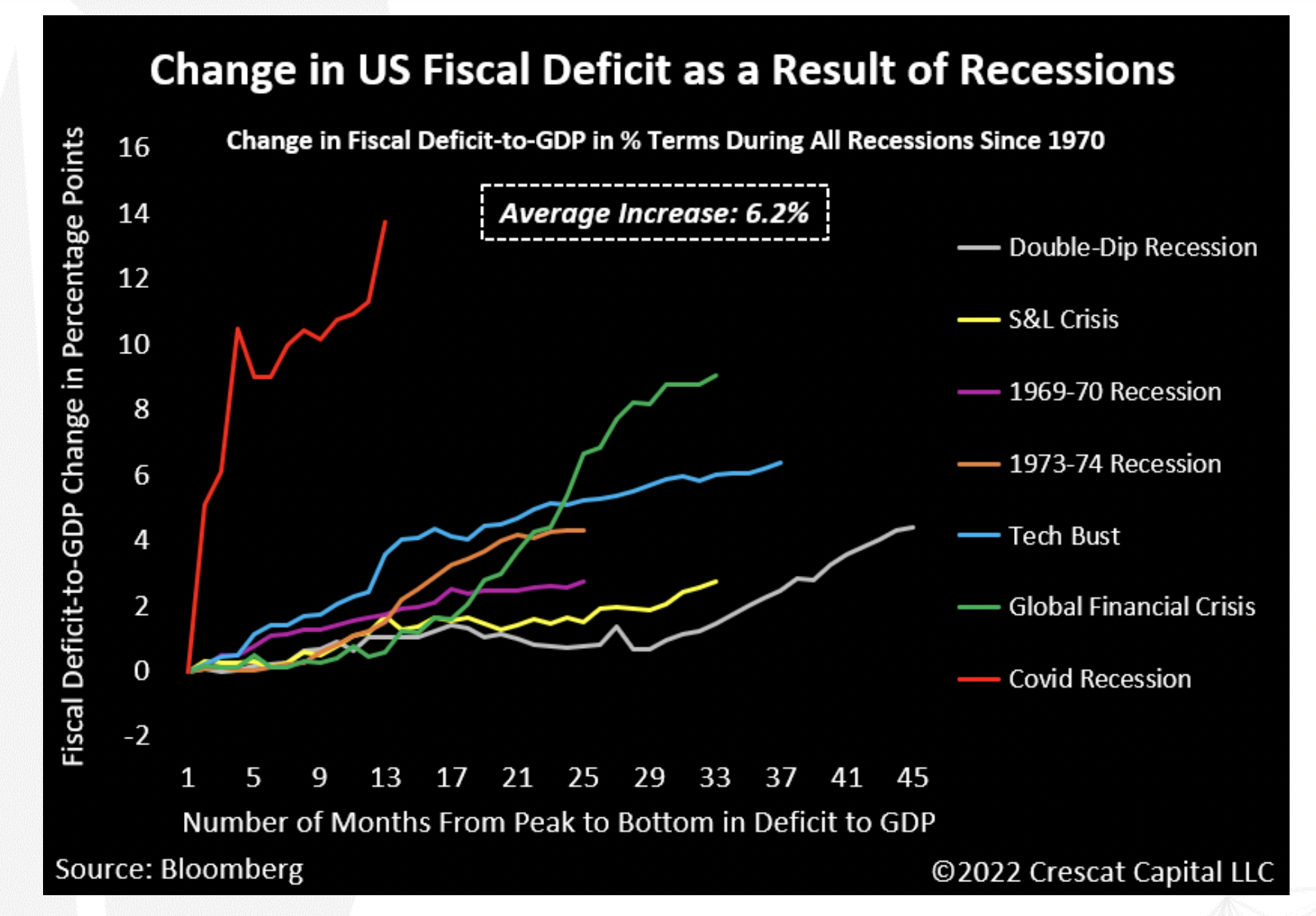

The first comprehensive economic analysis measuring the impact of sanctions on economic activity in Russia.

The team relies on “using private Russian language and unconventional data sources including high frequency consumer data, cross-channel checks, releases from Russia’s international trade partners, and data mining of complex shipping data”.

Results are grim – “From our analysis, it becomes clear: business retreats and sanctions are catastrophically crippling the Russian economy.”

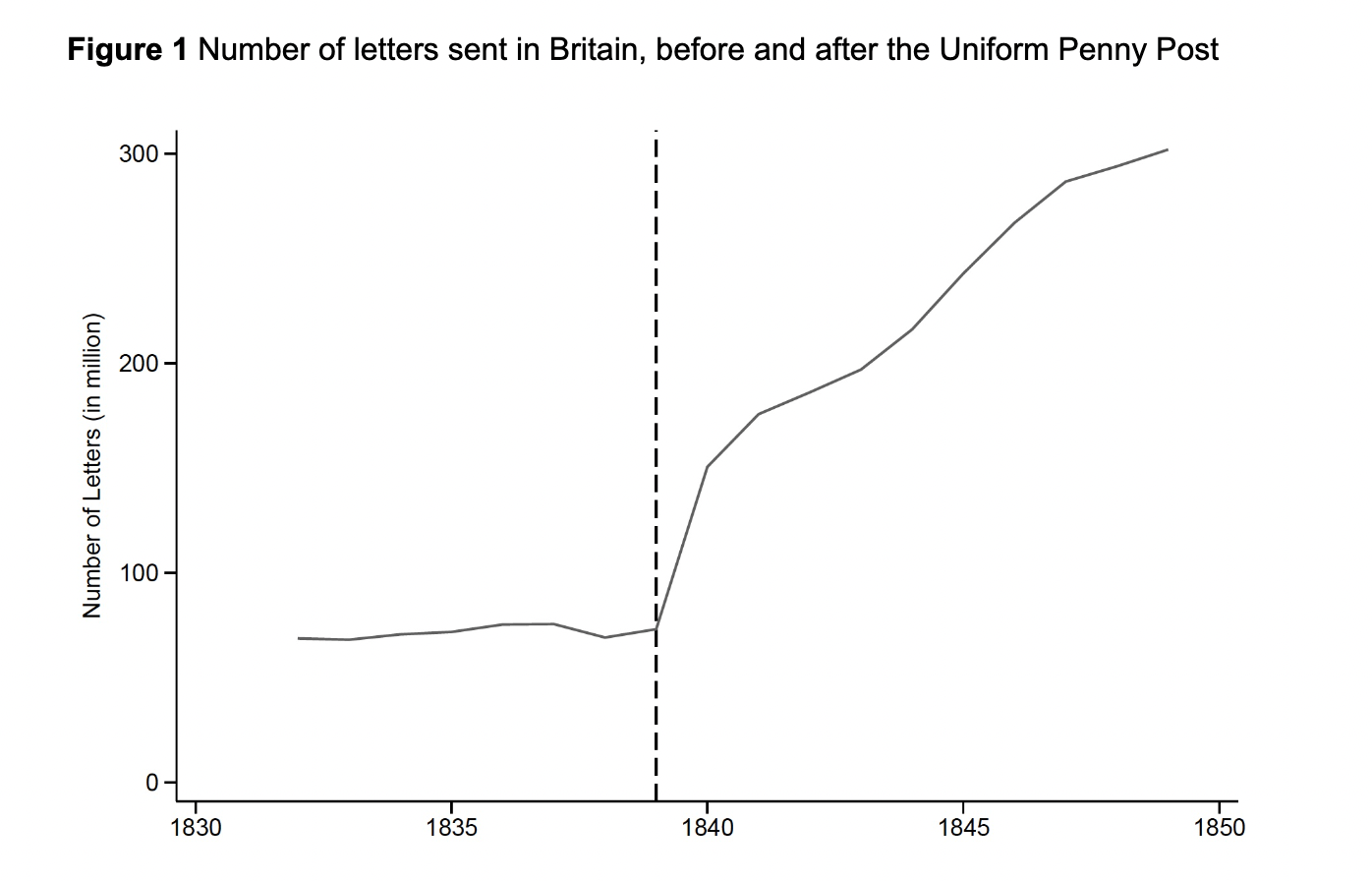

Meet one of the most dramatic changes in communication costs in history.

The introduction of the first modern postal system in Britain in 1840.

A 1839 Act of Parliament created the Uniform Penny Post – a single low postage rate and the first adhesive postage stamp, replacing a complex distance based system.

The results were monumental and, as this paper finds, also improved innovation.

Today, 73% of people in the UK consider post as essential or fairly important.

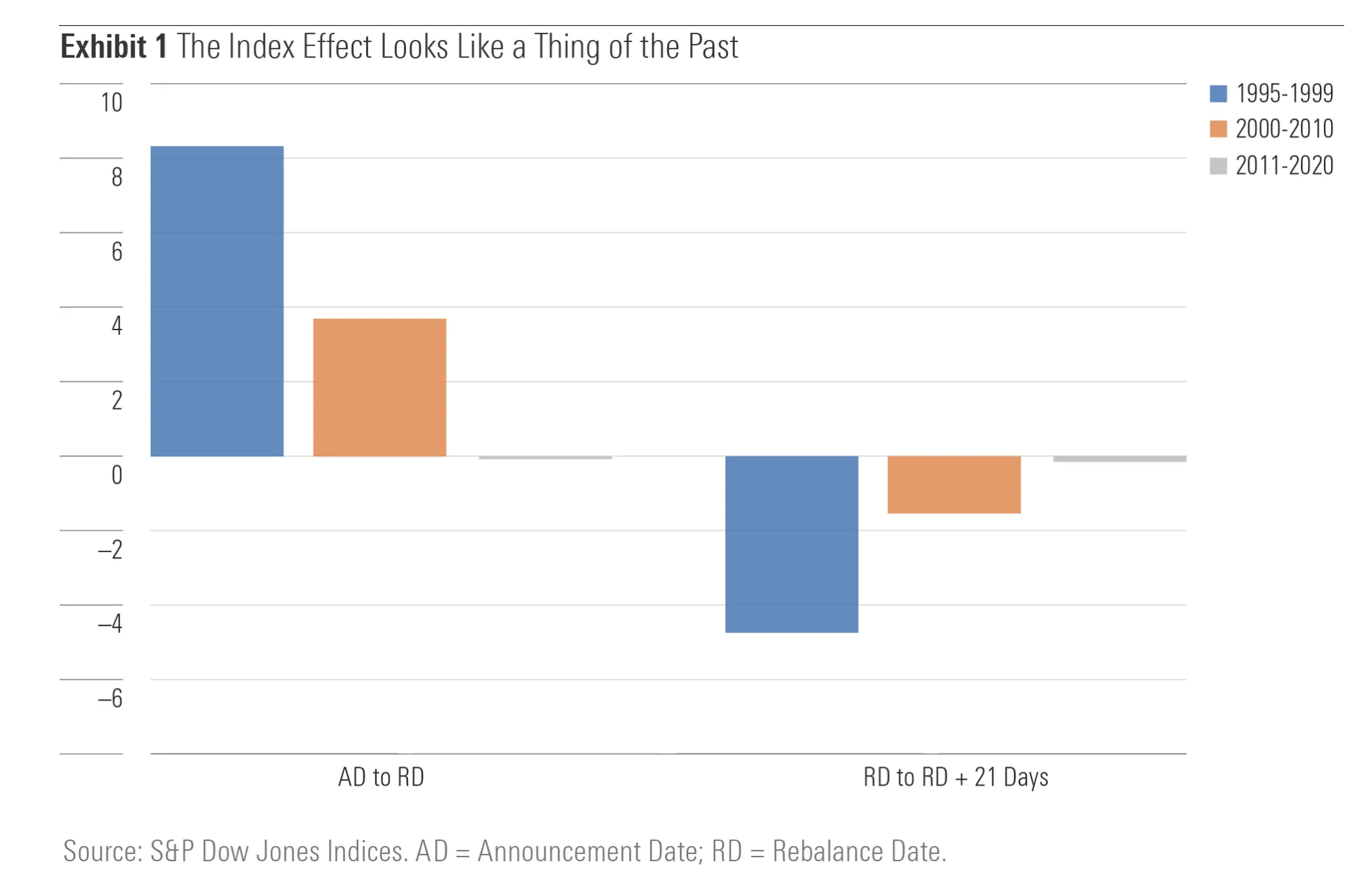

According to Morningstar data, inclusion into an index no longer attracts the usual rise (on announcement) and then fall in stock price.

“Indeed, the up-and-down trajectory that was once the fingerprint of the index inclusion effect now resembles a flat line that runs from announcement date through the weeks following inclusion in the S&P 500.“

This chart shows the performance of three groups of firms.

GAAP losers – firms where expenses exceed sales, but once an intangible investment adjustment is made they turn profitable. In other words they are investing.

Real losers – these are firms that even after the adjustment is made are still loss making.

Profitable firms – at the outset these firms are profitable i.e. sales exceed all expenses.

From 1980 – 2017, GAAP losers substantially outperformed

NB the outperformance vs. profitable firms really shows up post 1996. “The message is that the market ultimately recognizes and pays for intangible investments that create value, even if they create losses in the short term.“

This chart comes via Investment Talk, a brilliant curation of all manner of investment resources.

Footnote: Empirical Research Analysis, National Bureau of Economic Research. As of June 30, 2022. Cheapest quintile refers to the most undervalued 20% of stocks in an analysis of large-capitalization US stocks. Standard Deviation is a measure of dispersion of a data set from its mean. Prior to 1952, the spread is measured using the price-to-book data of the largest 1,500 stocks. Current Level refers to the valuation spread as of June 30, 2022 which is 0.4 standard deviations above the mean.

This chart “displays a strong cross-country correlation between men’s contributions to childcare and housework and the total fertility rate. In all countries with a fertility rate below 1.5 (blue dots), men do less than a third of the work in the home.“

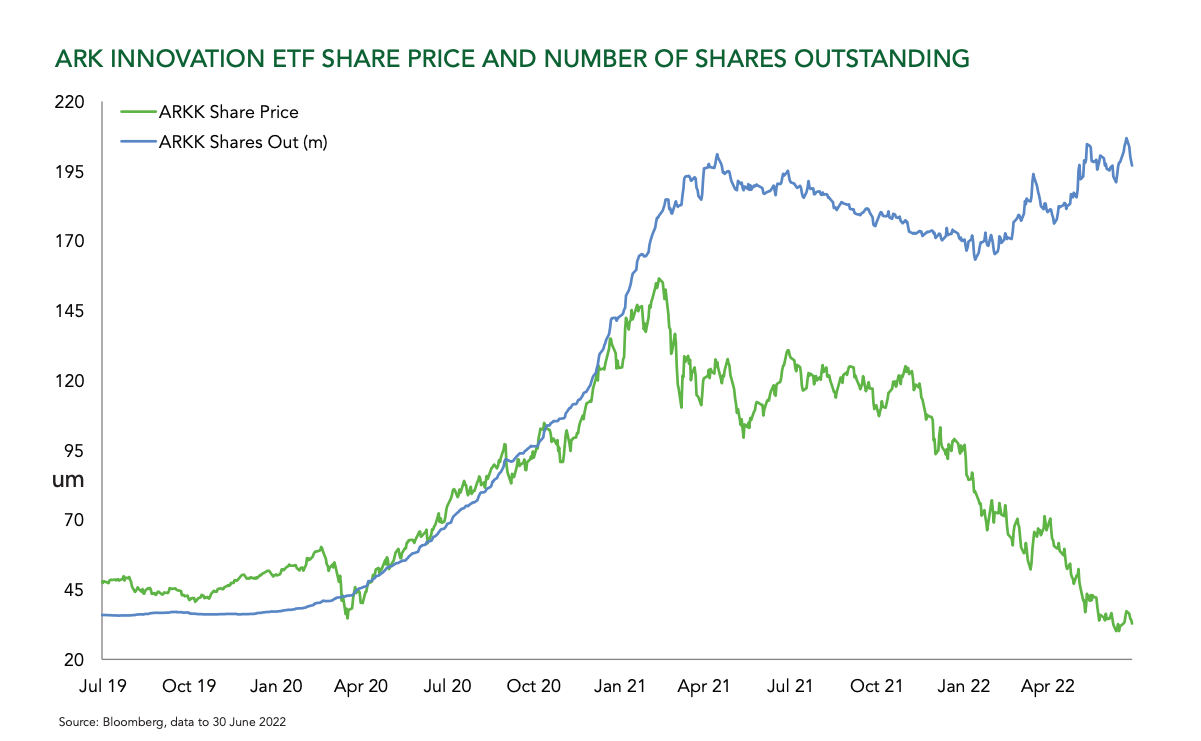

“In fact, flows have remained strongly positive into equities throughout the sell-off. As the chart shows, ARK Innovation ETF has suffered no net redemptions despite declining 71% in price since the peak. The ‘buy the dip’ mentality is alive and well.“

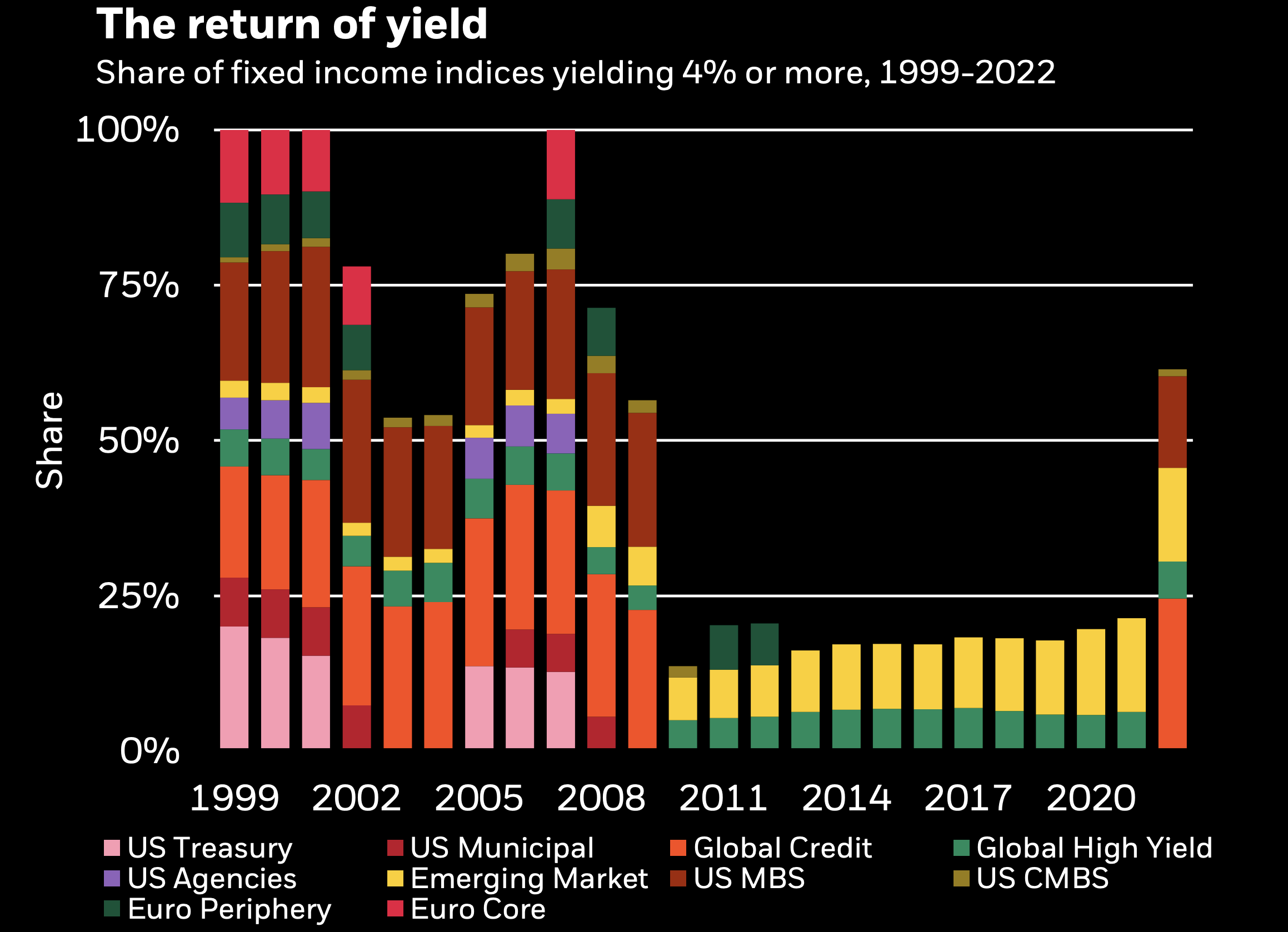

For the first time in a decade, the majority of fixed income assets yield 4% or above.

NB “The bars show market capitalization weights of assets with an average annual yield over 4% in a select universe that represents about 70% of the Bloomberg Mulitiverse Bond Index.”

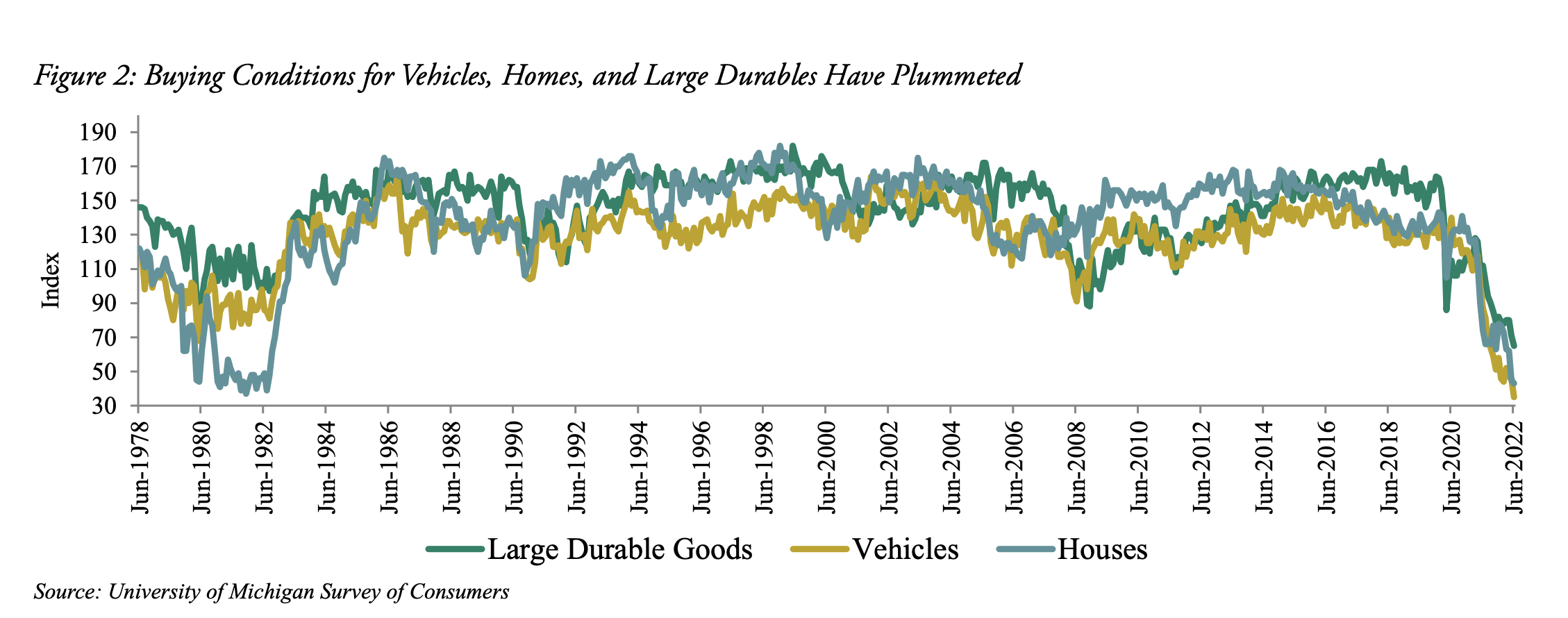

“Buying conditions for cars, houses, and large durable goods fell to multi-decade lows in June, according to the University of Michigan survey, meaning the vast majority of respondents believe it’s a bad time to buy the above“.

Consumer sentiment about the economy is also at a 40-year low. Interestingly, Oaktree make the point that the magnitude of decline could be skewed by political bias.

“For context, in June 1980, the difference between sentiment figures for self-identified Democrats and Republicans was 4.1 points. The gap is currently 31.5 points. This is another reminder of how people can interpret the same fundamentals very differently.“