He makes an interesting point that since the financial crisis (2009) certain industries have faced very high costs of equity (low valuations), and shareholder demands to return capital and limit or stop fully capacity expansion.

This is still the case, but against high current and pent up demand (savings, though there are mitigating factors here and here), under investment will lead to higher pricing and profits.

He gives examples of housing, air freight, copper, Titanium dioxide, cement, thermal coal/natural gas, and paperboard.

The latter is perhaps the only one that has ESG credentials in this list.

GlaxoSmithKline has been the subject of an activist attack by Elliott, who built up a significant stake in the company in April.

GSK then hosted their long awaited investor day in June – laying out a plan for a future after spinning off their consumer health division.

Elliott then released a letter which was quickly rebutted by the board of GSK who called for the usual “stability”.

This was a good write up of the whole interaction.

One interesting element that has not entered the discussion is the balance sheet.

NewGSK will have 2x ND/EBITDA, even after gearing up consumer health to 4x and paying a dividend back. It also has a pension (£2bn deficit) and minority payments to ViiV partner Shionogi. All of this constrains the firm.

“It is not just Asia which is seeing renewed weakness of manufacturing performance, however, with output in Russia coming close to stagnation again in June as rising virus numbers disrupted the economy, and a further steep fall in output was recorded in Mexico.

As a result, while developed world production continued to grow at a rate close to decade-highs in June, emerging market output growth came close to stalling, its lowest since June 2020.“

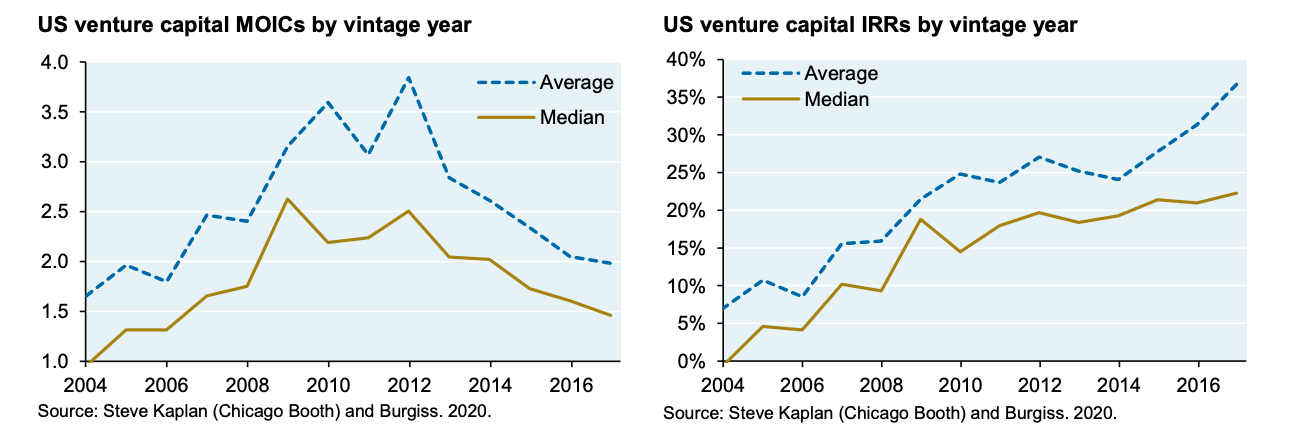

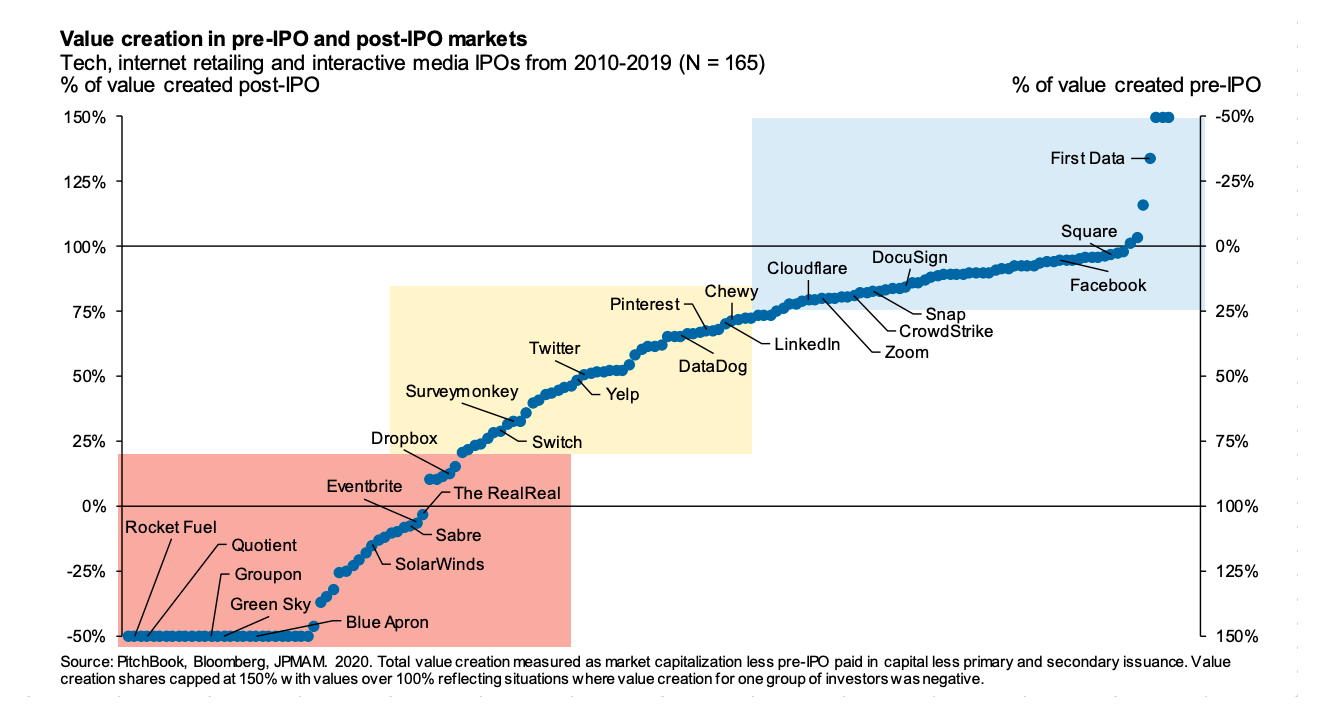

Who reaps the majority of the rewards from venture backed companies – VC or public markets?

“Over the last decade when measured in terms of total dollars of value creation accruing to pre- and post-IPO investors: post-IPO investor gains have often been substantial.“

Of the 165 IPOs analysed – the vast majority had a large share of value accrue to public markets (blue region).

There are some exceptions (red region), and some shared (yellow region).

A lot has been written about this remarkable company and its even more remarkable founders.

This was a really great, long piece covering everything from history to strategy.

“In 2006, using an SAT score from a test he’d taken at the age of 13 (an infuriating anecdote), Patrick matriculated to Lisp’s birthplace: the Massachusetts Institute of Technology. He’d sped through the final two years of his high school curriculum in just twenty days.”