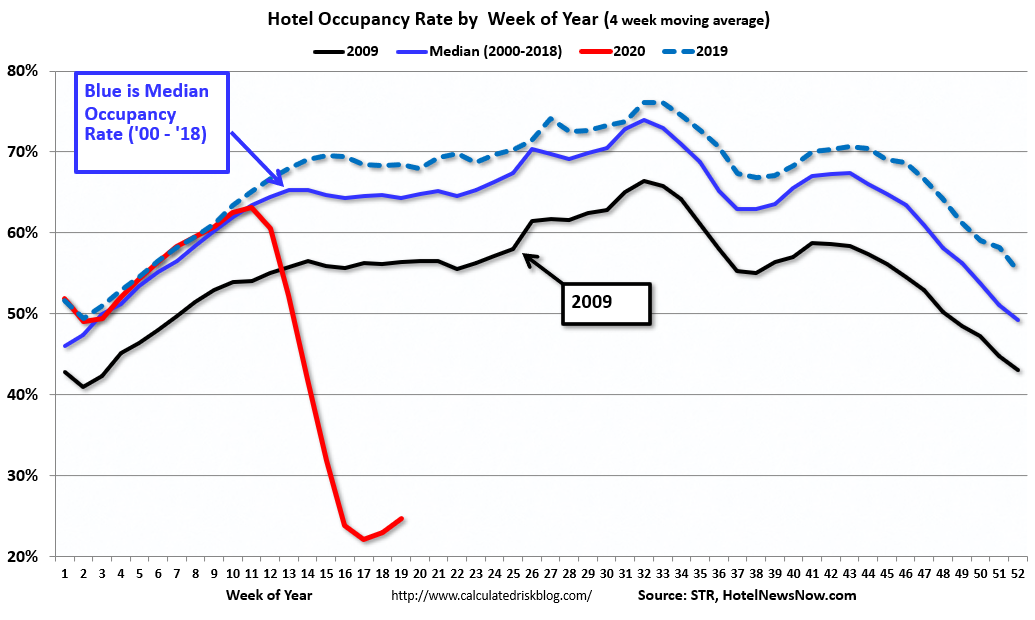

STR data for 26 April through 2 May 2020 showed slightly higher U.S. hotel occupancy compared with previous weeks.

The black line in the chart is 2009 – the worst year for hotels since the Great Depression.

“Week-to-week comparisons showed a third consecutive increase in room demand, which provides further hope that early-April was the performance bottom,”

TSA (Transport Security Administration) numbers have indeed ticked up and are at the highest level since March 30th.

“At the same time, this past week was the first to show solid evidence of leisure demand as weekend occupancy grew in states that have significantly eased mitigation efforts.”

A lot of traffic is starting to return to normal – fast food, gasoline stations and auto shops have all come back.

Indeed fuel demand has started to tick up as well.

Spending is also picking up (likely helped by government support).

Peaks have normalised in grocery stores and big box retail.

One interesting point here is that some food companies have pointed out that buying big multi-packs for stocking vs. single serve has hurt margins (page 6 here).

Home improvement stores and outdoor trails are still seeing traffic much higher than February.

Bars, restaurants, offices, clothing stores, furniture stores, movie theatres and gyms are still at lows.

“Rule of 3 in conversation. To get to the real reason, ask a person to go deeper than what they just said. Then again, and once more. The third time’s answer is close to the truth.”

“Separate the processes of creation from improving. You can’t write and edit, or sculpt and polish, or make and analyze at the same time. If you do, the editor stops the creator. While you invent, don’t select. While you sketch, don’t inspect. While you write the first draft, don’t reflect. At the start, the creator mind must be unleashed from judgement.”

They comb company transcripts for interesting quotes.

A few from the latest one.

“I’ve been so impressed with the Disney+ execution. Over 20 years of watching different businesses, incumbents, like Blockbuster and Walmart and all these companies, I’ve never seen such a good execution of the incumbent learning the new way and mastering it. And then to have them achieve over 50 million in six months, it’s stunning. So to see both the execution and the numbers line up, my hats off to them.” Netflix CEO Reed Hastings

“Thus far through April, our in-patient admissions are running about 30% below the prior year. Our emergency room visits are running about 50% below prior year as our in-patient surgeries. Our hospital based outpatient surgeries are running about 70% below our prior year as most elective procedures have been deferred. We have started to see these volume declines stabilize over the past week.” HCA CFO Bill Rutherford

“There hasn’t been enough debate about ability to make billions of doses. And for the record, we have 10,000 people producing over a billion doses right now of our own vaccine portfolio. This is not easy to do.“ Sanofi CEO Paul Hudson

A survey in 2019 of nearly 5000 people showed that 49% of product searches start on Amazon. For Prime members who are frequent users this figure is closer to 80%.

Google is notching up the competition.

Shopify, which Ben points out is a key member of this anti-amazon alliance, is also launching an app of their own to showcase the nearly 1m merchants using the platform.

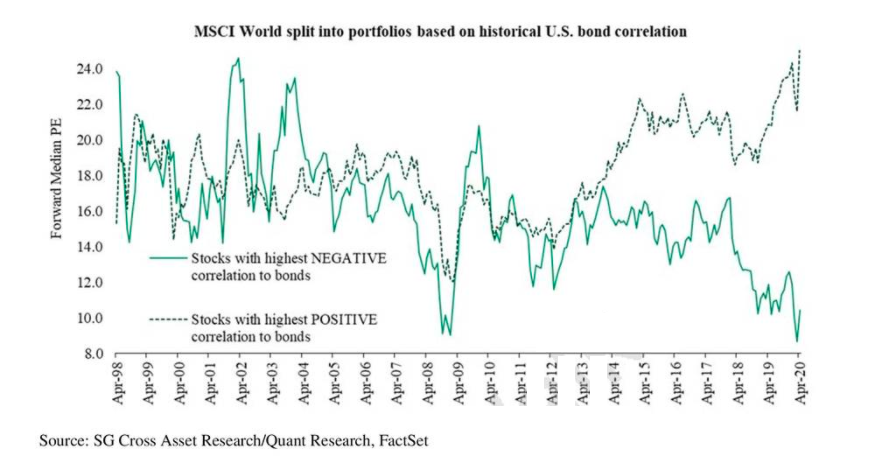

Whereas Einhorn thinks that inflation is coming, Hoisington think this couldn’t be further from the truth (and hence think the yield curve will be anchored at zero).

“Recent articles have suggested that the Federal Reserve and the Department of the Treasury are engaged in Modern Monetary Theory (MMT) or some form of “helicopter money”, the famous Milton Friedman phrase also referred to by Ben Bernanke. The inference is that once the virus is contained, these new efforts will yield different and more powerful economic and inflation results than did the Quantitative Easing periods following the 2008-09 Global Financial Crisis (GFC). Further, the suggestion is that the fiscal policy actions taken this year totaling $2.7 trillion will be far more effective than the $2 trillion stimulus package of 2009. Are these assertions that MMT is in place and monetary and fiscal actions will spur economic and inflation rates higher true? The short answer is no.”

What follows is a rather technical economic theoretic description of what is going on.

It is worth getting one’s head around this. Especially understanding how quantitative easing leads to increased excess deposits by banks at the Fed and not borrowing (a decision that is independent) and hence economic impact.

Overall they are predicting deflation – grim reading indeed.

“One of the most influential things he [Buffet] said to me was if you want to be successful, all you need to do is look around the room and think about the classmate or classmates you most admire and what qualities they have and just decide to adopt those qualities. If you do that, your chances of being successful go up enormously.”

“I actually think that people will be that much more desperate for human connection after this experience than they were before.”

He is probably right on the last point – long human connection?

The fund is -21.5% in Q1 and down a futher -1.1% in April (despite the market rebound).

Interesting discussion of how, despite taking net from 74% to 15%, they still struggled with performance against a falling market.

Eninhorn’s value style is struggling in recent years and these markets. Despite this Greenlight is starting to market the fund again.

Letter includes interesting debate on inflation post-crisis, what to buy in that environment, his current holdings and shorts (incl TSLA), new positions. Always worth a read.

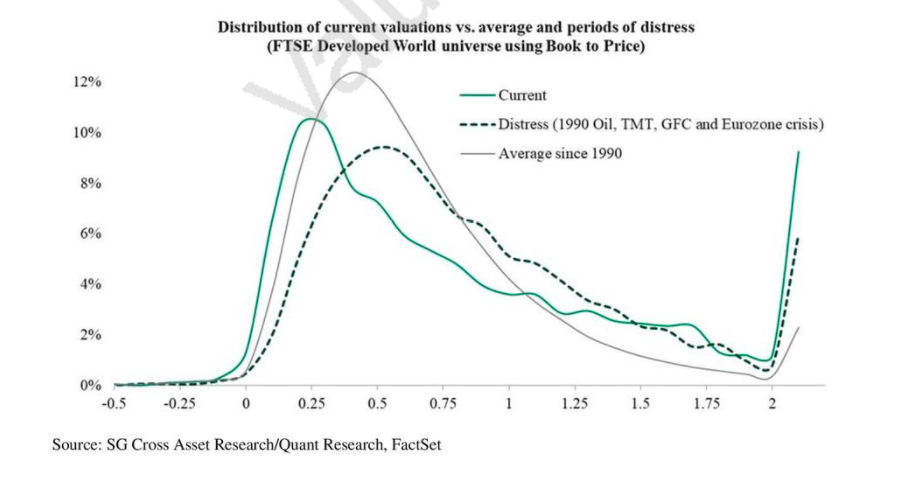

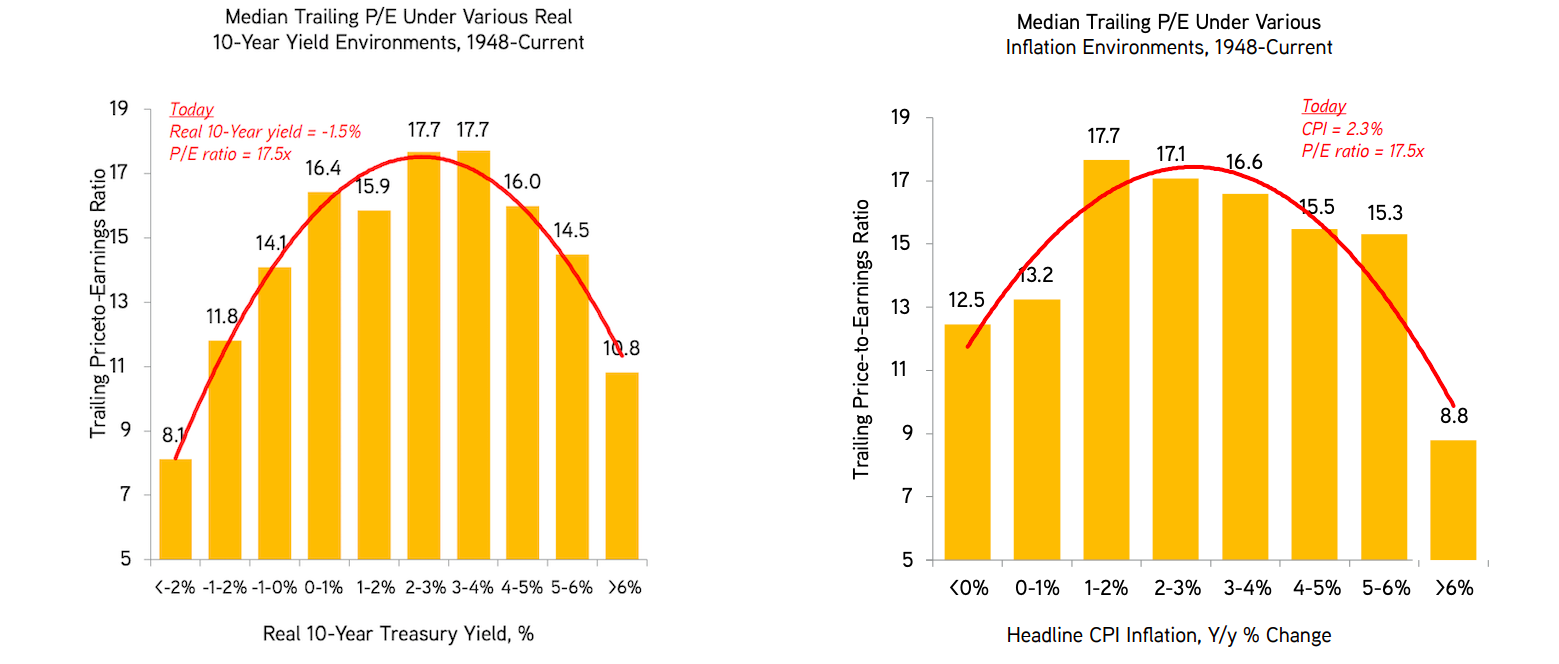

They plot the markets trailing P/E ratio against CPI inflation (right hand side) and the 10-year real treasury yield (left hand side).

The data is from 1948 to today and sourced from BofAML

As real-rates go negative or inflation falls multiples tend to be lower.

KKR analysis suggests there isn’t some funny data skewing results here.

What about today? at the current real 10-year yield of -1.5% and inflation rate of 2.3% (likely to fall) the 17.5x P/E ratio for the market (since increased) stands out as too high.

These types of equity strategy charts are good to hang on to.