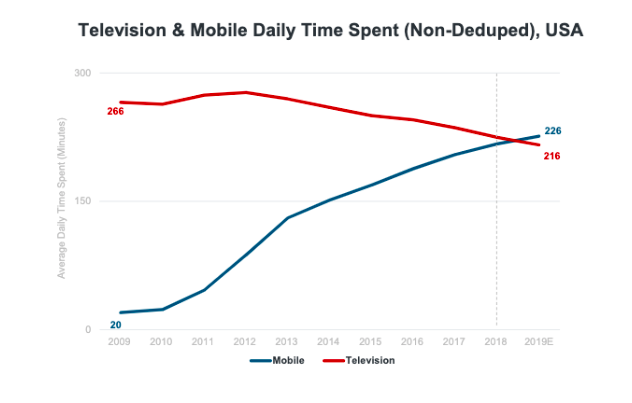

“The rise of AirPods, smart speakers, and other wearable devices may not signal the onset of a true platform shift, but it undoubtedly represents a transformational evolution in the way we will consume media — and this emerging paradigm of distributed, “eyes up” device interaction directly benefits audio more than other content categories.“

An interesting perspective on how to invest in winners.

“There is a lot of advice about how to be a good startup founder. But there isn’t very much about how to be a good startup investor. Before going any further, I should point out that this is a particularly hard time to invest in startups—it’s easier right now to be a capital-taker than a capital-giver.”

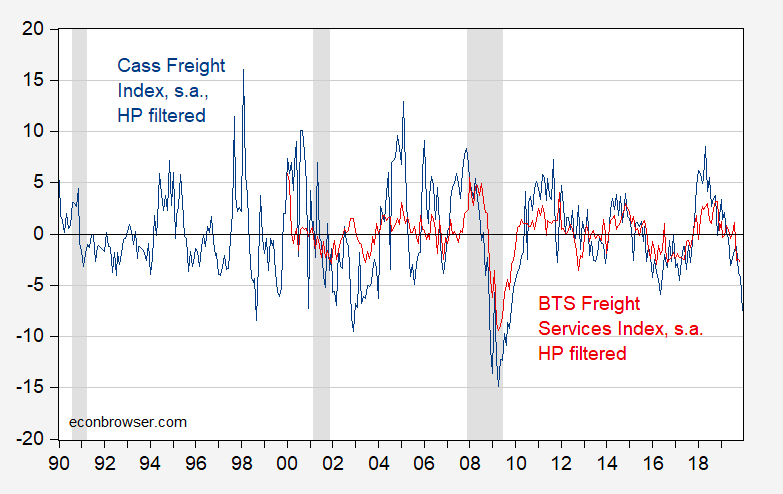

Interestingly freight data in the US continues to be weak.

“Both the shipments and expenditures components of the Cass Freight Index marked their lowest reading of 2019 and took another step backwards in terms of y/y growth. There is lots of hope in the stock market and the freight market for a better 2020, but the trends have yet to turn.”

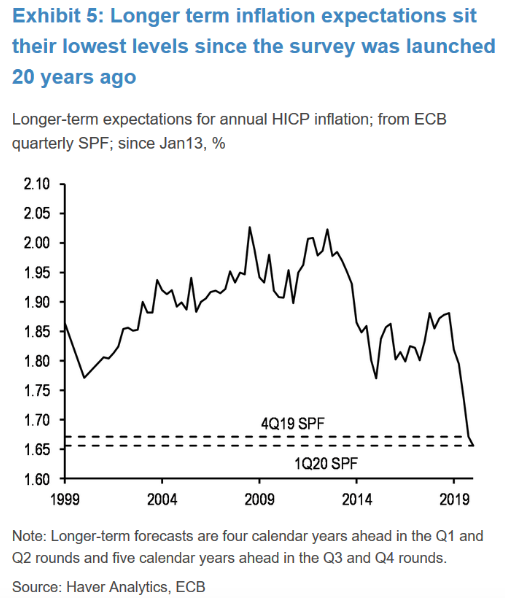

Chart from Haver Analytics supports their arguments on subdued inflation.

These five factors – loss of momentum, monetary restraint, high debt levels, flat profits and excess capacity – will bring about slower growth and continue to subdue core inflation.

Over the past 65 years, yields on long dated risk-free U.S. treasury securities moved in the same direction as core inflation on an annual basis roughly 80% of the time. We believe that there is a high probability that this relationship will hold in 2020 as inflationary pressures continue to subside.