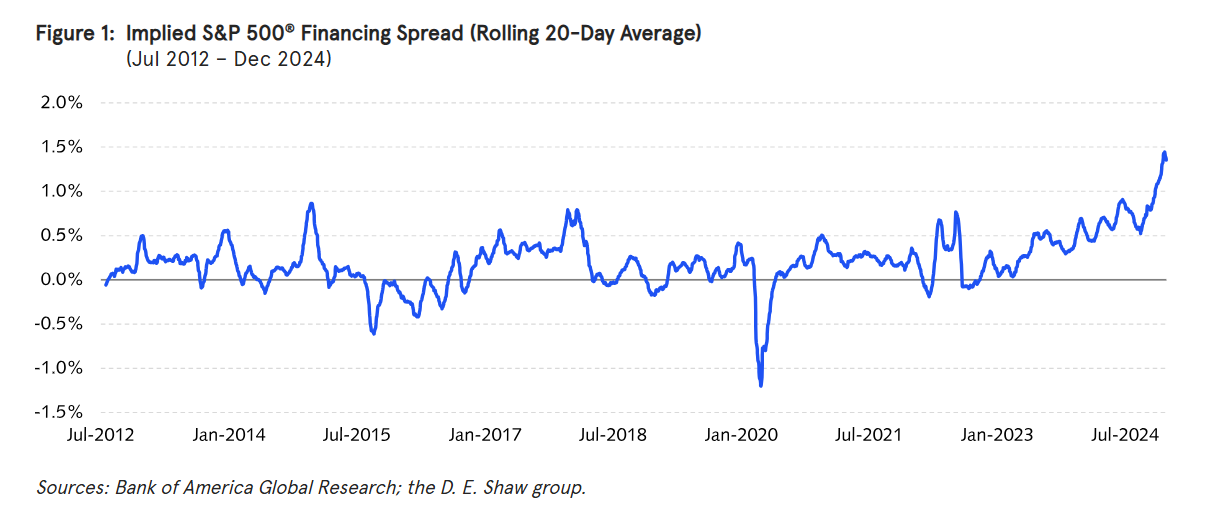

The financing rate for equity exposure via futures has been very high.

The S&P 500® financing spread can’t be directly observed, but it can be estimated by comparing the actual price of futures to the fair value implied by dividend forecasts, interest rates, and spot prices. Figure 1 plots one such estimate since 2012.

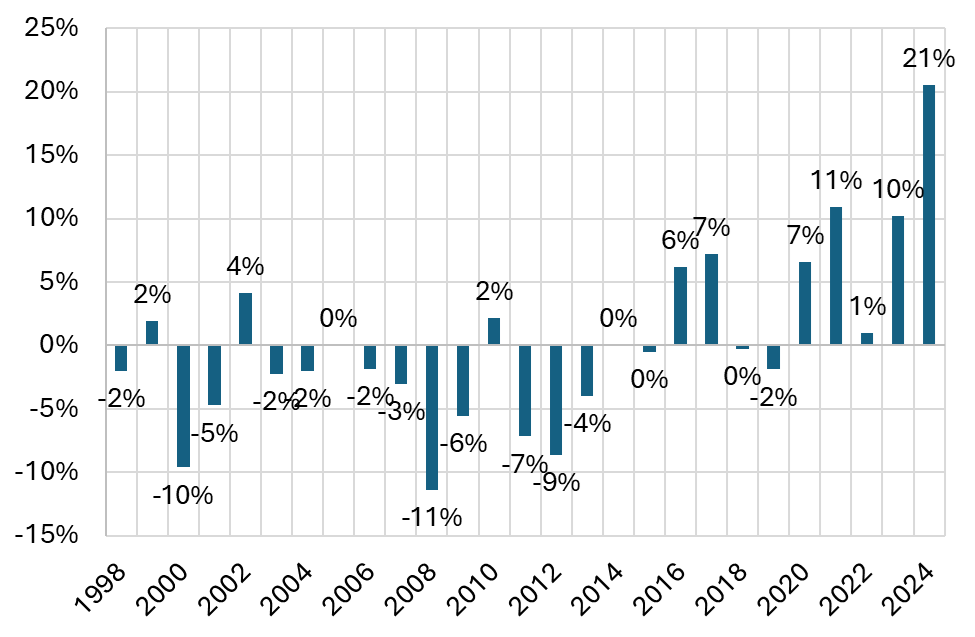

Once S&P 500 return is decomposed into factors 2024 really stands out.

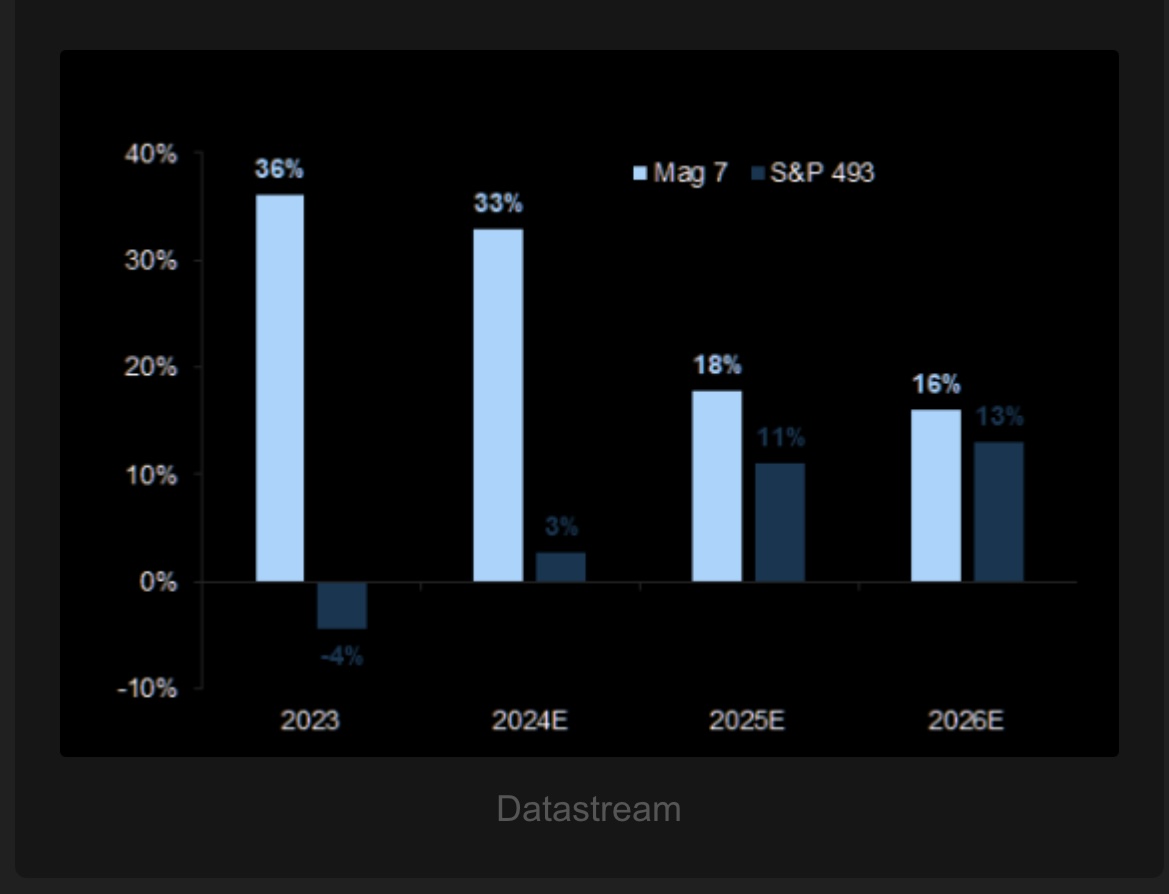

“… What is particularly interesting about 2024 is how much of the S&P 500 return came from non-systematic (i.e., idiosyncratic) returns, driven by the significant appreciation of the “Magnificent Seven” (Mag-7), which now account for 35% of the S&P 500. Idiosyncratic returns are company specific and by definition should be uncorrelated and random.“

“In fact, idiosyncratic return has never contributed as significantly to the overall S&P 500 return as it has recently. Over the trailing 24 month period, idiosyncratic returns have accounted for 21% of the 51% return of the S&P 500.“