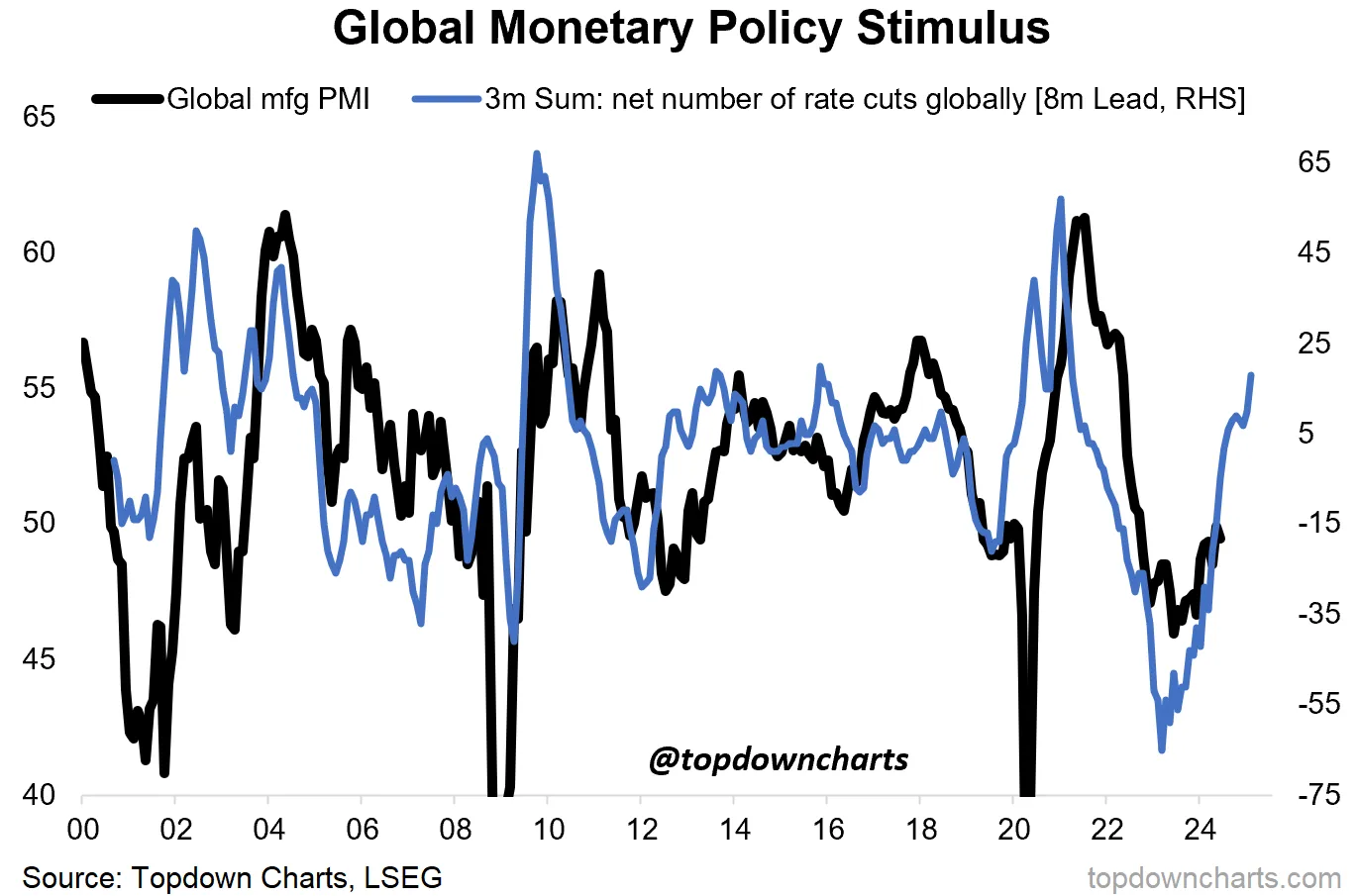

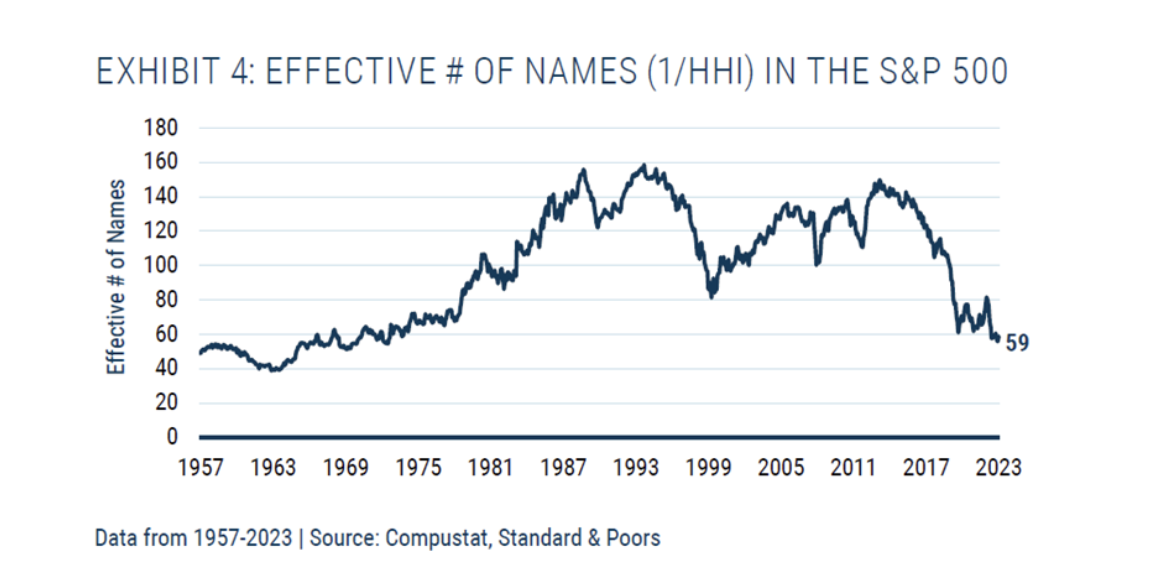

We all know indices are concentrated right now, more than ever. Just how bad is it?

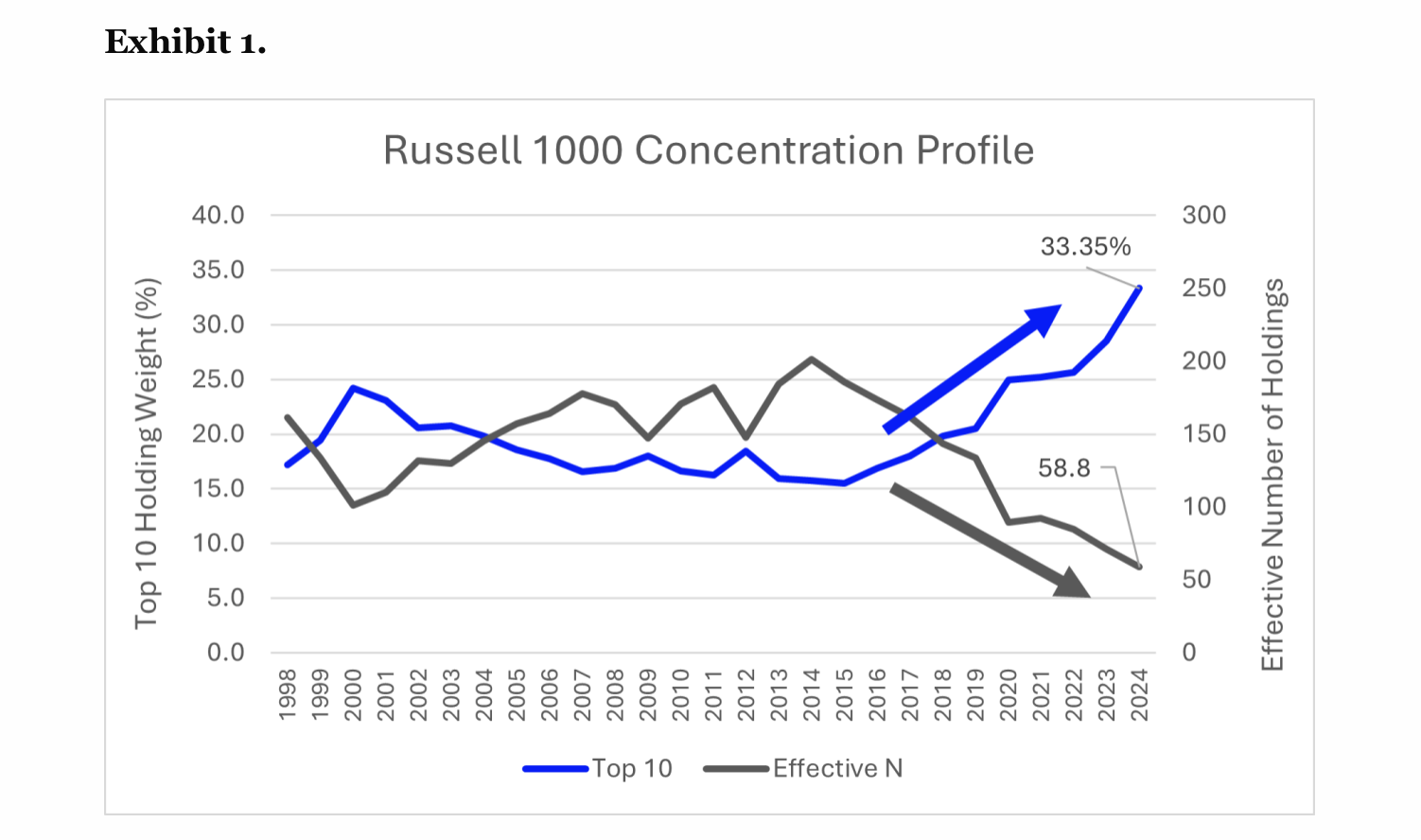

“The startling conclusion is that, despite the Russell 1000 nominally providing exposure to its namesake number of stocks, the index affords an effective diversification of only 59 stocks.“

“Not only does market-cap weighting induce substantial single-stock risk, but the diversification provided by this foundational asset class has evaporated by 70% over the past decade.“

Equal weight, as the article argues, is not the solution here, as it “suffers from significant operational costs, underperformance, questionable assumptions, and skewed risk bets.“

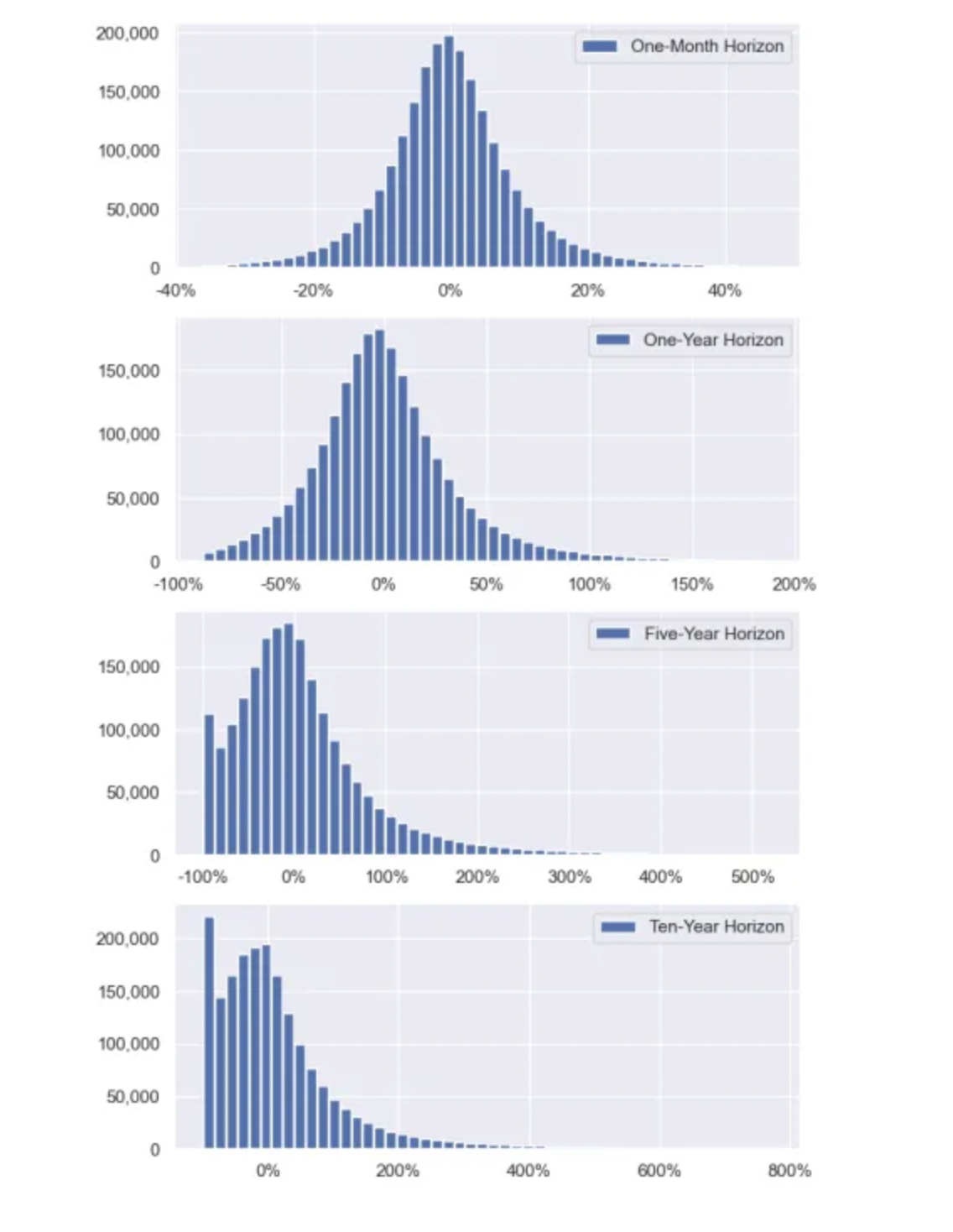

“Antti Petajisto analyzed the return distribution of all US stocks in the CRSP database going back to 1926. Below is the distribution of returns for different investment horizons. Note that the distribution gets more and more skewed to the left as investment horizons increase and that the left-hand side of the distribution is not zero, but a total loss of investment (-100% return).“

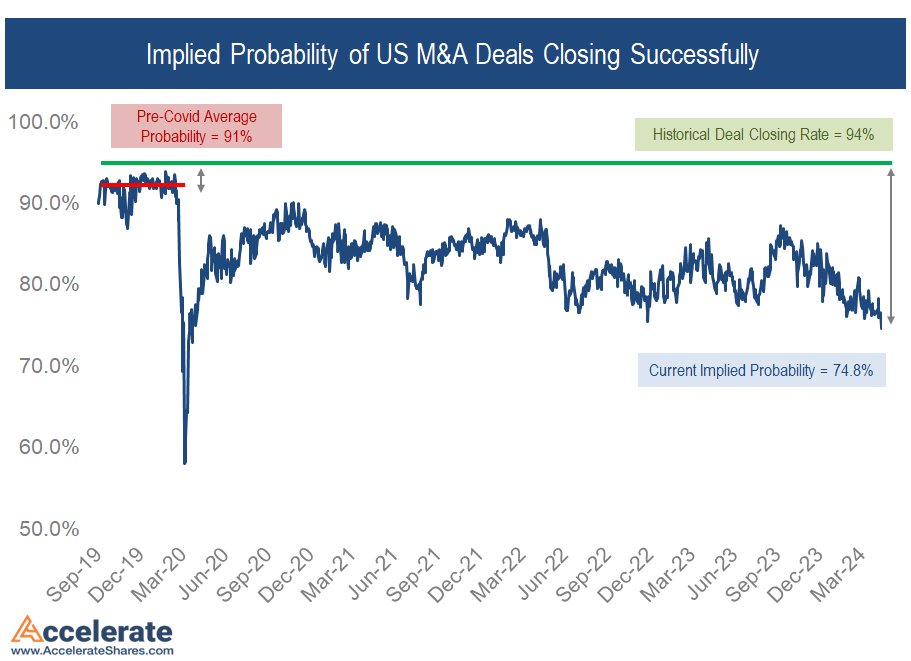

The probability of deal success is currently very low. In a small part, this is due to interest rates but also an aggressive DOJ/FTC (see JetBlue/Spirit).

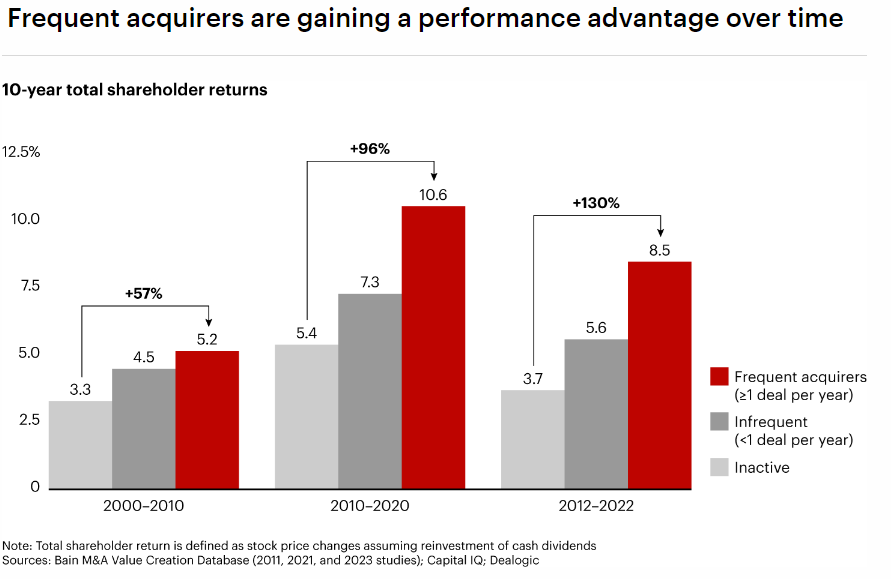

Bain study shows that frequent acquirers outperform.

“To put some data behind this assertion, from 2000 to 2010 companies that were frequent acquirers earned 57% higher shareholder returns vs. those that stayed out of the market. Now that advantage is about 130% (see Figure 1).“

“The S&P 500’s total concentration, which we can measure using a Herfindahl-Hirschman Index (or HHI), is equivalent today to that of an equal-weighted, 59-stock portfolio. Ten years ago, the index was more than twice as diversified. We have never seen – over any 10-year period – a decline (or increase) in diversification of the magnitude we have just witnessed.“

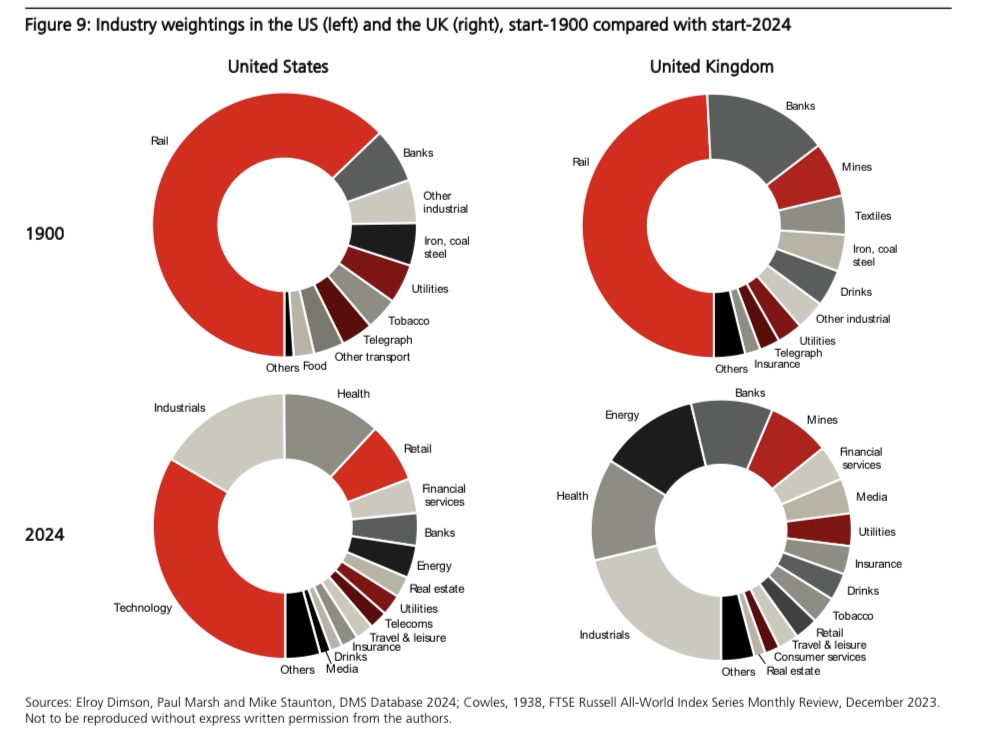

Let this sink in – “Of the US firms listed in 1900, some 80% of their value was in industries that are small or extinct today; the UK figure is 65%“

Many of these industries have simply moved to lower-cost countries.

“Yet similarities between 1900 and 2024 are also apparent. The banking and insurance industries continue to be important. Similarly, such industries as food, beverages (including alcohol), tobacco, and utilities were present in 1900 and continue to be represented today. In the UK, quoted mining companies were important in 1900 just as they are in London today“

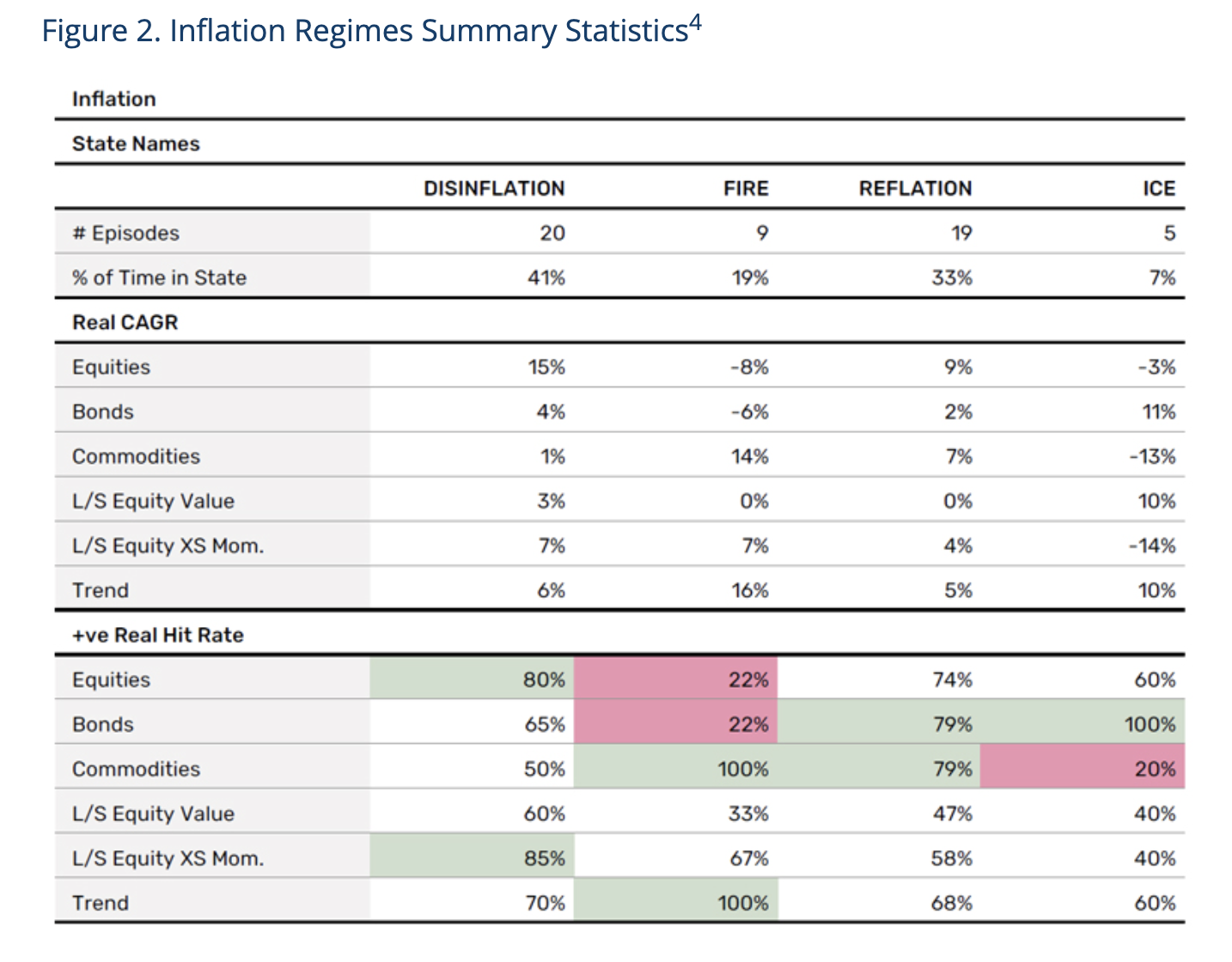

“Inflation is probably the most predictable of the regime frameworks, in terms of the magnitude of returns and the persistence of direction. If you are only allowed to use one economic datapoint to guide your decisions, US headline CPI should be it.“

Equity bull markets are 80% of history. Don’t forget the simple lessons…

Man group’s team tries to study whether investment regimes exist and whether one can profit from them.