The story of Renaissance Technologies and Jim Simons is worth reading in full.

But this post does a great job pulling out the key extracts.

One consistent feature of their success relates to this – “What you’re really modeling is human behavior. Humans are most predictable in times of high stress — they act instinctively and panic. Our entire premise was that human actors will react the way humans did in the past…we learned to take advantage.”

A really great and rare podcast with the legendary investor.

His points on how to frame buy and sell decisions are particularly good.

As is his view of the UK needing capital to unlock the world-class IP historically generated there and give people ambition to build global platforms instead of solving individual problems.

Finally, his advice to young people about enthusiasm really rings true.

This was a good summary of other points by a former colleague, but the full thing is absolutely worth your time.

He makes an interesting point that since the financial crisis (2009) certain industries have faced very high costs of equity (low valuations), and shareholder demands to return capital and limit or stop fully capacity expansion.

This is still the case, but against high current and pent up demand (savings, though there are mitigating factors here and here), under investment will lead to higher pricing and profits.

He gives examples of housing, air freight, copper, Titanium dioxide, cement, thermal coal/natural gas, and paperboard.

The latter is perhaps the only one that has ESG credentials in this list.

It makes the distinction between a winner’s game (where you win by winning) and a loser’s game (where you win by not losing).

He argues that investing has become the latter but does offer some advice:

(1) play your own game – “Impose upon the enemy the time and place and conditions for fighting preferred by oneself.” Simon Ramo suggests: “Give the other fellow as many opportunities as possible to make mistakes, and he will do so.“

(2) keep it simple – “Play the shot you’ve got the greatest chance of playing well.”

(3) concentrate on defence (selling) vs. offence (buying).

This is a fascinating slightly old interview with Chris Cole of Artemis Capital Management.

He runs a long volatility fund i.e. a crash protection fund.

In the interview he talks about the core principle of the fund – to sacrifice the next linear predictable outcome in order to gain exposure to a truly convex upside outcome.

Around minute seven he goes into a brilliant analogy using George Lucas’ success with Star Wars.

Most interestingly, this idea can also be applied to life as Chris describes in minute 47 of the interview embedded here.

Worth checking out their writing and following him on Twitter.

Interesting latest piece (page 15) from Hosking Partners on why the rotation into value stocks will persist.

(1) They perform well at the end of recessions (2) stimulus favours value (3) Covid recovery will be long and is only getting underway now in some countries (4) fund managers are entrenched (5) Interesting ESG angle.

There is also a full webcast that is worth listening to.

“What are the similarities between a forecaster and a one-eyed javelin thrower? Answer: Neither is likely to be very accurate but they are typically good at keeping the attention of the audience.“

We leverage the Snippet ecosystem to expand our footprint holistically in the space we operate. We have a long runway for our KPIs. After all it is a global and iconic brand.

A fun list of banned corporate “words” from FundSmith.

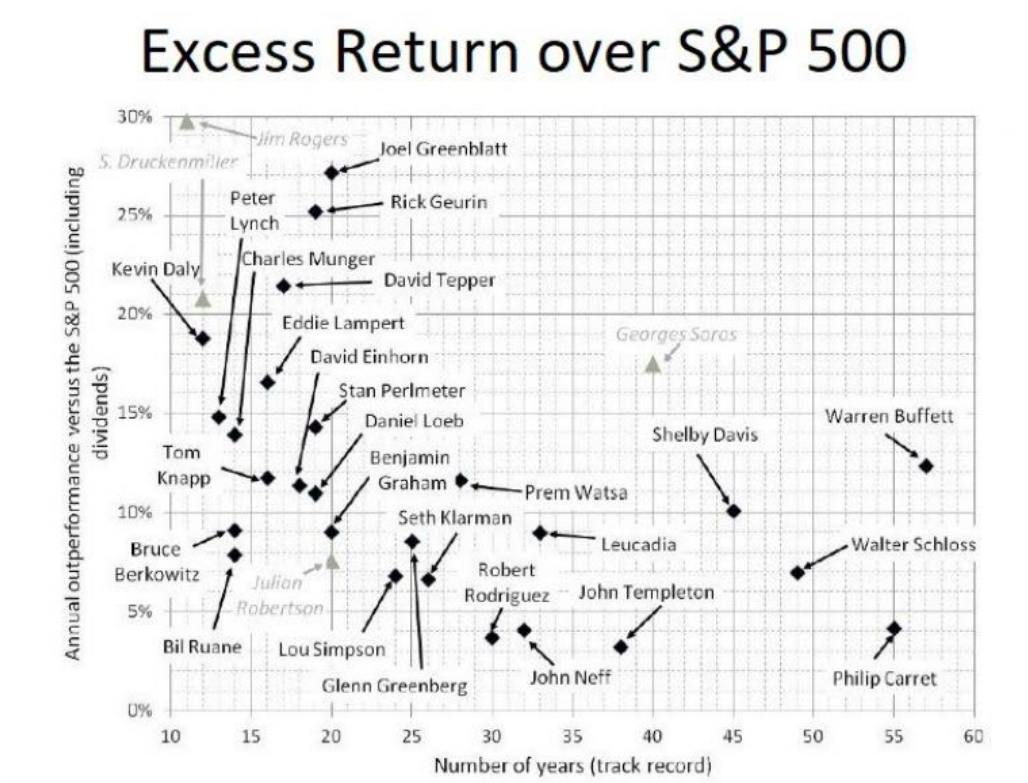

The partnership is an investment success story, outperforming the index by +14.3% per annum for thirteen years (2001 – 2014).

Although all are worth your time, this is nice blog post that pulls out some of the most interesting quotes and ideas. There are many.

“One trick that Zak and I use when sieving the data that passes over our desks is to ask the question: does any of this make a meaningful difference to the relationship our businesses have with their customers? This bond (or not!) between customers and companies is one of the most important factors in determining long-term business success. Recognising this can be very helpful to the long-term investor.”

A thought-provoking piece (first one in the link) arguing against concentrated equity portfolios – the orthodoxy of the day.

Concentrated portfolios are built on the idea of “analytical certainty” which lends itself easily to “overconfidence” and “overweighting hubris”

Institutions that hold several such concentrated portfolios, thereby diversifying, might find instead they suffer from other forms of correlation – in terms of stock size (large cap) and style (quality or growth).

They will also find that the higher fees charged by concentrated active portfolios add up and don’t average down.

Most interestingly concentration “underweights luck” – that term most fund managers have pushed deep into their subconscious.

“The resources are not simply about investing. It is about becoming a better human being. Learning from the success and failure of others is the fastest way to get smarter and wiser without a lot of pain.”

Alta Fox have done a massive analysis of all the best performing stocks over the last five years.

Overall – they find that financially healthy companies with advantageous business positioning tend to do better.

Acquisitions are a feature of these top performing stocks (perhaps because of the five year time frame).

The analysis is a bit too micro cap focussed and only concentrates on Australia, Europe and North America and excludes some sectors (e.g. materials), but is nonetheless useful.