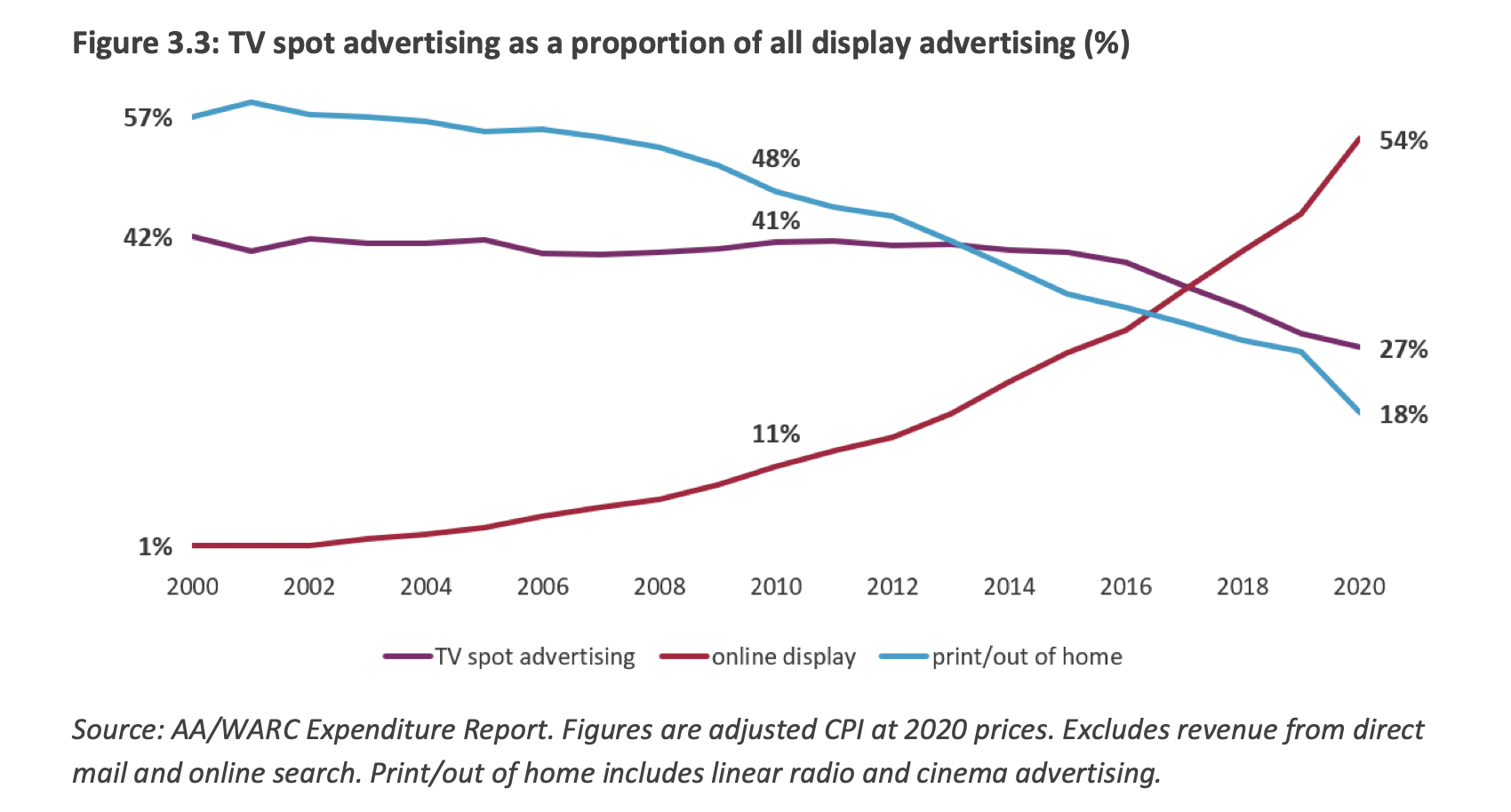

Online display advertising is rapidly displacing TV in the UK.

“However, despite the increase in online, TV advertising remains the medium of choice for big brands wanting to reach an audience quickly and at scale, with advertisers citing TV’s ability to drive both short-term sales and longer-term brand equity as a major advantage.”

George Lucas was forced to sell Pixar to fund his divorce.

Venture capitalists, 35 of them, refused to back the firm as did eight strategic partners, but Steve Jobs agreed.

“If we’d had any other investor than Steve, we would have been dead in the water.“

He forced the firm to succeed “He’d berate those of us in management, then write another check”

Pixar was eventually sold for $7bn to Disney “This is astounding considering they could have had us for free in the 1970s when we approached them on bended knee.”

“Splitting a good black jack hand” is a great way to describe how Michael Dell pulled off perhaps the most daring deal of the last decade.

“Before the LBO, he owned 15.6% of his company, shares worth less than $4 billion. Thanks to the miracles of his financial engineering, he will own 52% of Dell and a 42% stake in VMware. The total value of his Dell holdings is $40 billion.“

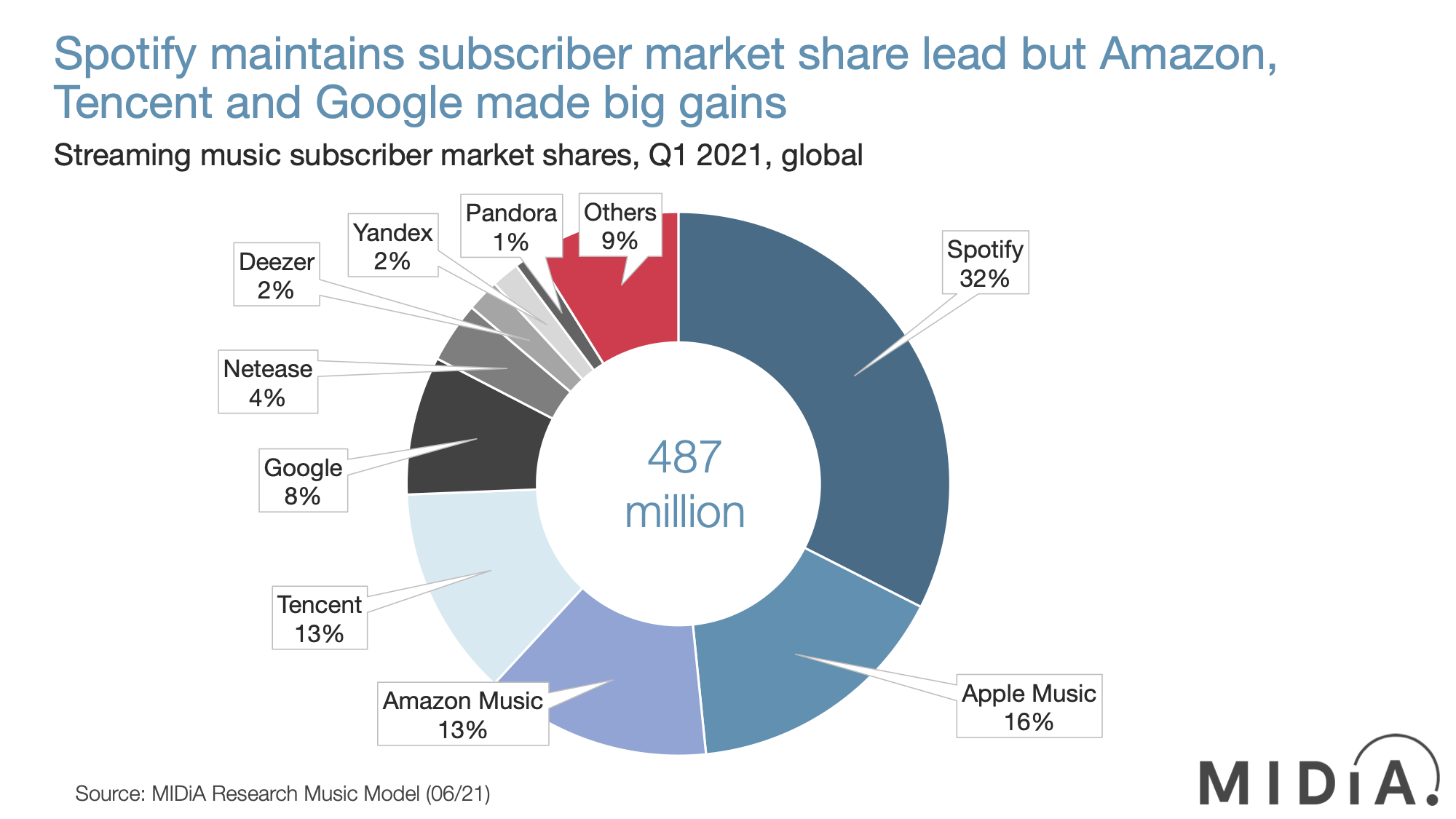

There are 487m music streaming subscribers globally at Q1 2021.

Emerging markets are now central to this market accounting for 60% of all 2020 subscriber growth.

Spotify is still the leader with 32% but has lost two points of market share since Q1 2020.

Google’s Youtube Music has been the standout story – “The early signs are that YouTube Music is becoming to Gen Z what Spotify was to Millennials half a decade ago.“

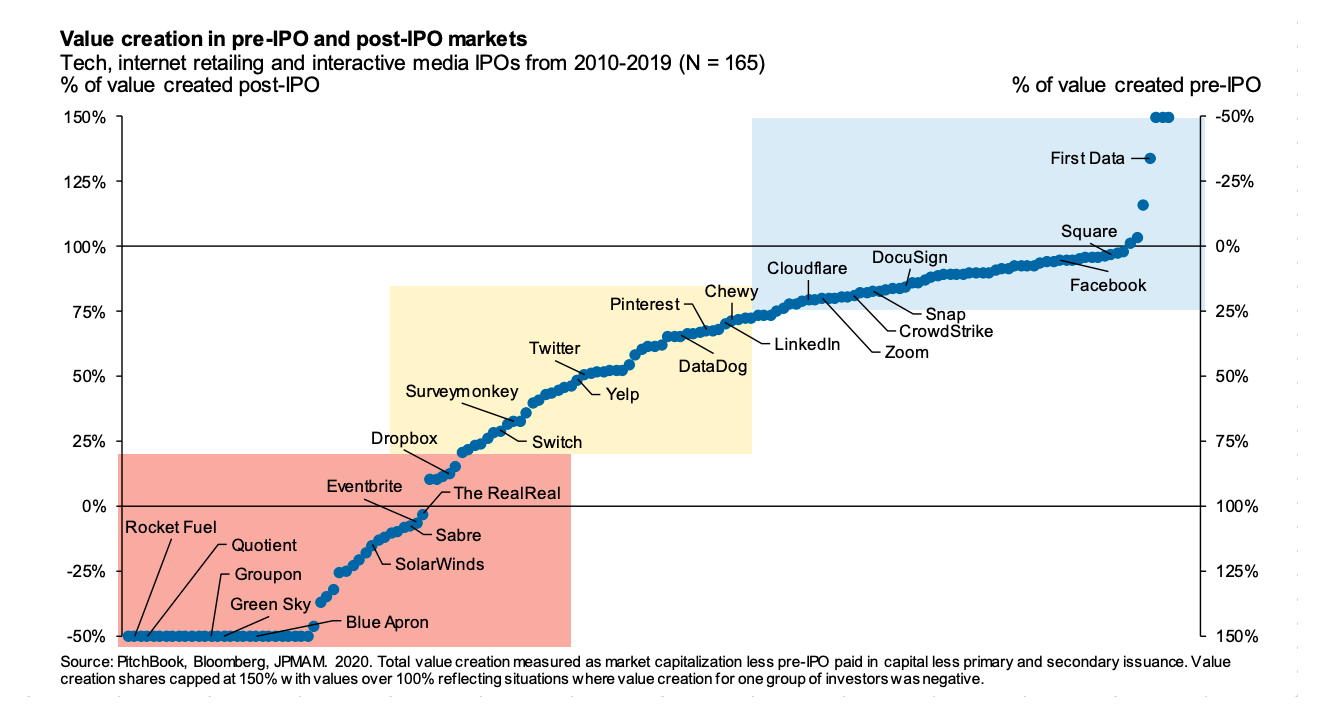

Who reaps the majority of the rewards from venture backed companies – VC or public markets?

“Over the last decade when measured in terms of total dollars of value creation accruing to pre- and post-IPO investors: post-IPO investor gains have often been substantial.“

Of the 165 IPOs analysed – the vast majority had a large share of value accrue to public markets (blue region).

There are some exceptions (red region), and some shared (yellow region).

A lot has been written about this remarkable company and its even more remarkable founders.

This was a really great, long piece covering everything from history to strategy.

“In 2006, using an SAT score from a test he’d taken at the age of 13 (an infuriating anecdote), Patrick matriculated to Lisp’s birthplace: the Massachusetts Institute of Technology. He’d sped through the final two years of his high school curriculum in just twenty days.”

Fascinating article on the ballooning software requirement in cars.

“Even low-end vehicles are quickly approaching 100 ECUs and 100 million of lines of code as more features that were once considered luxury options, such adaptive cruise control and automatic emergency breaking, are becoming standard“.

Interesting essay on the future of the web – Web3.

Web3 allows a new generation of disrupters to create products that actually pay people to use them, and aligns the incentives of creators, consumers, suppliers, and investors.

“Imagine going to Disney World, and getting shares in Disney, the company, every time you took a ride, bought Mickey Merch, or sent your friend a picture. Or that owning shares in Disney let you skip all of the lines as long as you held the shares. That’s what tokens do.“

In the essay he presents Web3 competitors to all the major web platforms.

One neat way to describe the landscape is to think of “crypto as listed versions of traditional VC, with a real-time, 24/7 quoted price.” (Source).

Good analysis of the bill proposed in Congress on regulating Big Tech.

The bill tries to restrict a lot of activity that is seen as anti-competitive behaviour on platforms.

It is also aimed at breaking up the businesses, making data easily portable, and acquisitions harder.

“Taken together, these laws would be a revolution in antitrust law, adapted for an era where Big Tech marketplaces, not railroads, are the dominant businesses of the day. They could also have many serious unintended side effects, so the final form of these laws matters a lot.”